Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

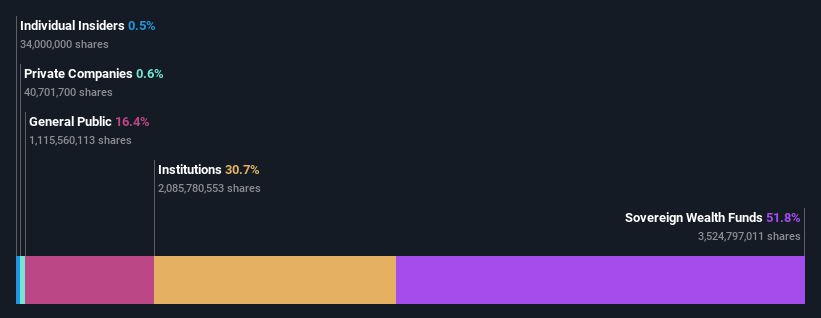

Wall Street Journalsovereign wealth funds who own 52% along with institutions invested in Sime Darby Property Berhad (KLSE:SIMEPROP) saw increase in their holdings value last week

Key Insights

- Sime Darby Property Berhad's significant sovereign wealth funds ownership suggests that the key decisions are influenced by shareholders from the larger public

- The largest shareholder of the company is Permodalan Nasional Berhad with a 52% stake

- Institutions own 31% of Sime Darby Property Berhad

Every investor in Sime Darby Property Berhad (KLSE:SIMEPROP) should be aware of the most powerful shareholder groups. We can see that sovereign wealth funds own the lion's share in the company with 52% ownership. Put another way, the group faces the maximum upside potential (or downside risk).

Following a 4.0% increase in the stock price last week, sovereign wealth funds profited the most, but institutions who own 31% stock also stood to gain from the increase.

Let's delve deeper into each type of owner of Sime Darby Property Berhad, beginning with the chart below.

View our latest analysis for Sime Darby Property Berhad

What Does The Institutional Ownership Tell Us About Sime Darby Property Berhad?

Institutions typically measure themselves against a benchmark when reporting to their own investors, so they often become more enthusiastic about a stock once it's included in a major index. We would expect most companies to have some institutions on the register, especially if they are growing.

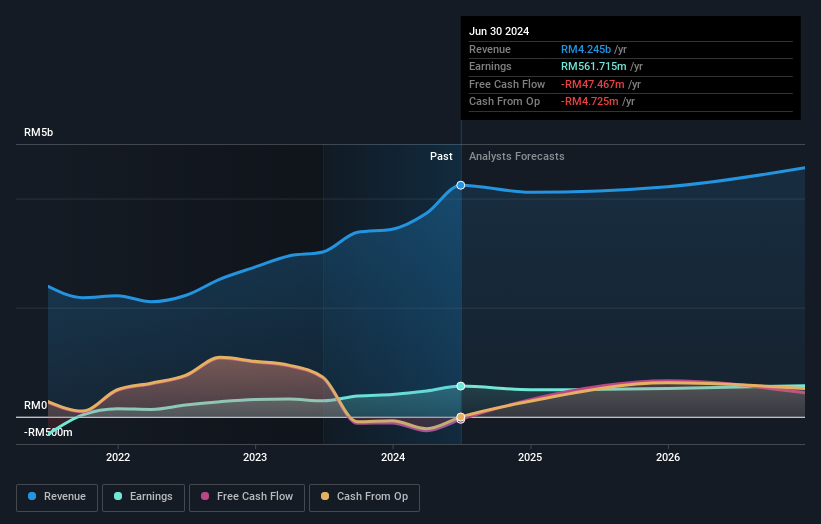

We can see that Sime Darby Property Berhad does have institutional investors; and they hold a good portion of the company's stock. This suggests some credibility amongst professional investors. But we can't rely on that fact alone since institutions make bad investments sometimes, just like everyone does. When multiple institutions own a stock, there's always a risk that they are in a 'crowded trade'. When such a trade goes wrong, multiple parties may compete to sell stock fast. This risk is higher in a company without a history of growth. You can see Sime Darby Property Berhad's historic earnings and revenue below, but keep in mind there's always more to the story.

We note that hedge funds don't have a meaningful investment in Sime Darby Property Berhad. Looking at our data, we can see that the largest shareholder is Permodalan Nasional Berhad with 52% of shares outstanding. This implies that they have majority interest control of the future of the company. With 9.3% and 6.3% of the shares outstanding respectively, Employees Provident Fund of Malaysia and Kumpulan Wang Persaraan are the second and third largest shareholders.

Researching institutional ownership is a good way to gauge and filter a stock's expected performance. The same can be achieved by studying analyst sentiments. Quite a few analysts cover the stock, so you could look into forecast growth quite easily.

Insider Ownership Of Sime Darby Property Berhad

The definition of an insider can differ slightly between different countries, but members of the board of directors always count. The company management answer to the board and the latter should represent the interests of shareholders. Notably, sometimes top-level managers are on the board themselves.

I generally consider insider ownership to be a good thing. However, on some occasions it makes it more difficult for other shareholders to hold the board accountable for decisions.

Our information suggests that Sime Darby Property Berhad insiders own under 1% of the company. It's a big company, so even a small proportional interest can create alignment between the board and shareholders. In this case insiders own RM53m worth of shares. Arguably, recent buying and selling is just as important to consider. You can click here to see if insiders have been buying or selling.

General Public Ownership

The general public-- including retail investors -- own 16% stake in the company, and hence can't easily be ignored. While this size of ownership may not be enough to sway a policy decision in their favour, they can still make a collective impact on company policies.

Next Steps:

It's always worth thinking about the different groups who own shares in a company. But to understand Sime Darby Property Berhad better, we need to consider many other factors. Consider risks, for instance. Every company has them, and we've spotted 2 warning signs for Sime Darby Property Berhad you should know about.

Ultimately the future is most important. You can access this free report on analyst forecasts for the company.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.