Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalZhengzhou Suda Industry Machinery Service And 2 Other Undiscovered Gems In China

As Chinese equities experience a downturn amid fading optimism about Beijing's stimulus measures, the market environment presents unique opportunities for discerning investors. In this context, identifying promising small-cap stocks like Zhengzhou Suda Industry Machinery Service can be crucial, as these companies often offer growth potential through innovative solutions and strategic positioning in niche markets.

Top 10 Undiscovered Gems With Strong Fundamentals In China

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Hangzhou Xili Intelligent TechnologyLtd | NA | 14.50% | 3.31% | ★★★★★★ |

| Shenzhen TVT Digital Technology | 1.02% | 12.79% | 32.81% | ★★★★★★ |

| Shenzhen Tongye TechnologyLtd | 4.87% | 9.24% | -21.23% | ★★★★★★ |

| Shanghai Haixin Group | 0.87% | 3.75% | 7.37% | ★★★★★★ |

| Sinotherapeutics | NA | 76.64% | 0.81% | ★★★★★★ |

| Kangping Technology (Suzhou) | 26.12% | -7.88% | -2.37% | ★★★★★☆ |

| Shanghai YongLi Belting | 12.97% | -12.15% | 18.03% | ★★★★★☆ |

| Silvery Dragon Prestressed MaterialsLTD Tianjin | 22.46% | 0.77% | -3.26% | ★★★★☆☆ |

| Sichuan Dowell Science and Technology | 33.70% | 13.47% | -12.57% | ★★★★☆☆ |

| Shenzhen Tongyi Industry | 72.24% | 13.41% | -16.34% | ★★★★☆☆ |

We'll examine a selection from our screener results.

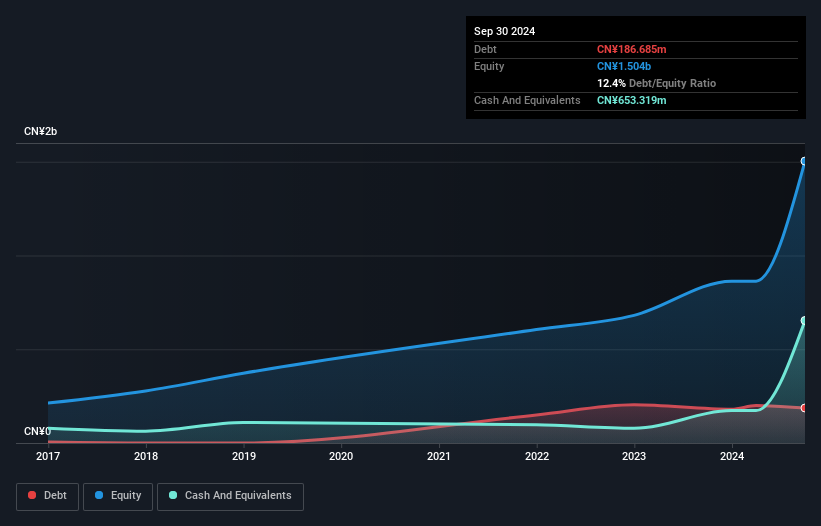

Zhengzhou Suda Industry Machinery Service (SZSE:001277)

Simply Wall St Value Rating: ★★★★★☆

Overview: Zhengzhou Suda Industry Machinery Service Co., Ltd. operates in the machinery service industry with a market capitalization of CN¥2.77 billion.

Operations: Zhengzhou Suda Industry Machinery Service generates revenue primarily through its machinery service operations. The company's financial performance is characterized by a focus on optimizing its cost structure to enhance profitability.

Zhengzhou Suda Industry Machinery Service, a small player in the industry, recently completed an IPO raising ¥608 million. The company reported half-year sales of ¥569.83 million, slightly down from last year's ¥593.75 million, but net income rose to ¥78.91 million from ¥67.69 million previously. Its earnings growth of 30% outpaced the commercial services sector's -1.8%. With a price-to-earnings ratio of 15.6x below the Chinese market average and satisfactory debt metrics, it shows promising potential despite its illiquid shares and increasing debt-to-equity ratio over five years from 3.8% to 23%.

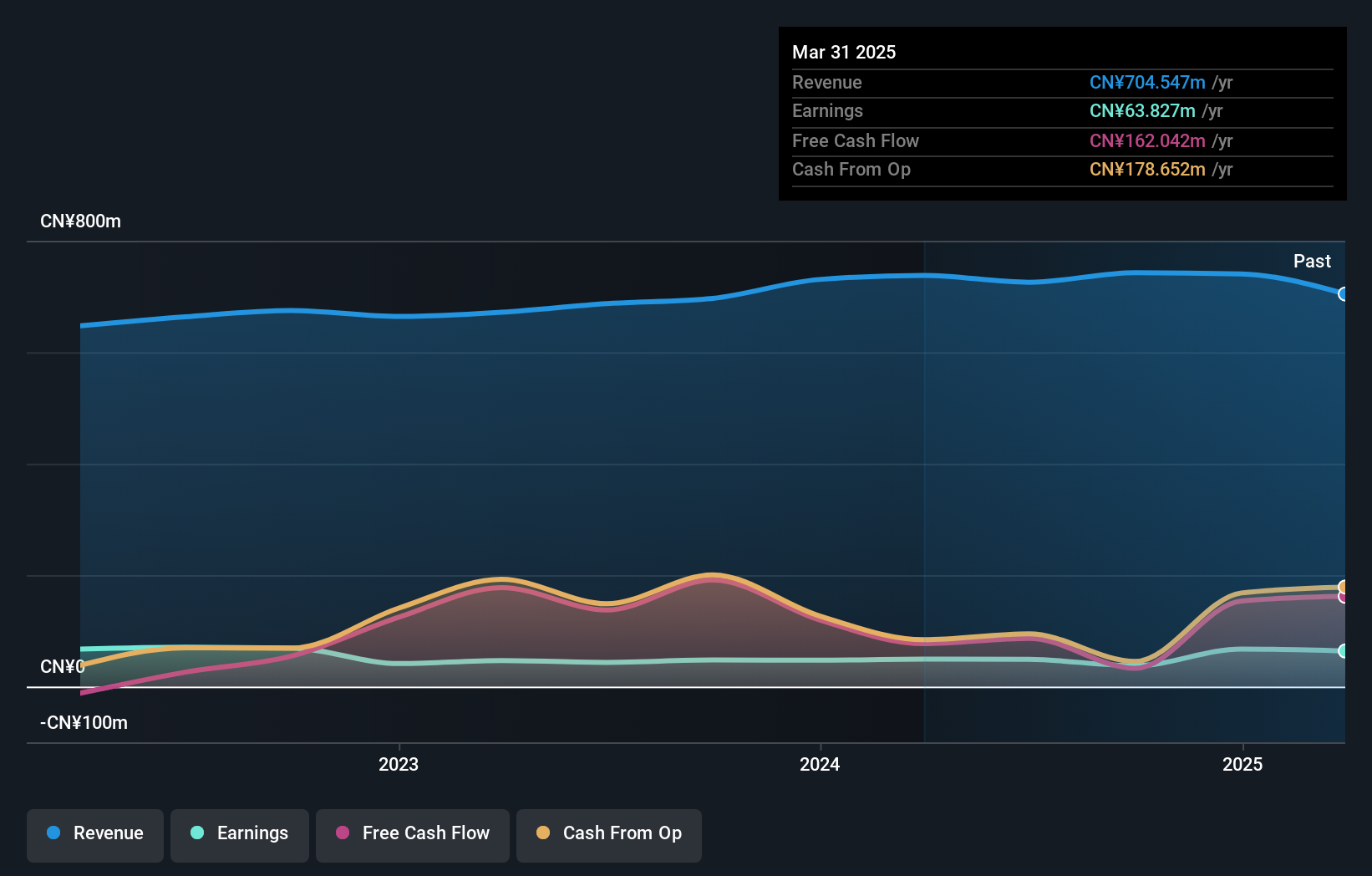

Shenzhen Forms Syntron InformationLtd (SZSE:300468)

Simply Wall St Value Rating: ★★★★★★

Overview: Shenzhen Forms Syntron Information Co., Ltd. (SZSE:300468) operates in the software and information services industry with a market capitalization of CN¥11.84 billion.

Operations: Forms Syntron generates revenue primarily from its software and information services segment, amounting to CN¥725.52 million.

With a track record of high-quality earnings, Shenzhen Forms Syntron Information Ltd. stands out in the IT sector by surpassing industry growth rates, with its earnings rising 12% last year compared to the sector's -11%. Despite a net income increase to CNY 36.8 million for H1 2024 from CNY 35.44 million, revenue slightly dipped to CNY 342.63 million from CNY 347.54 million year-on-year. The company remains debt-free over five years and enjoys positive free cash flow, though its share price has been volatile recently.

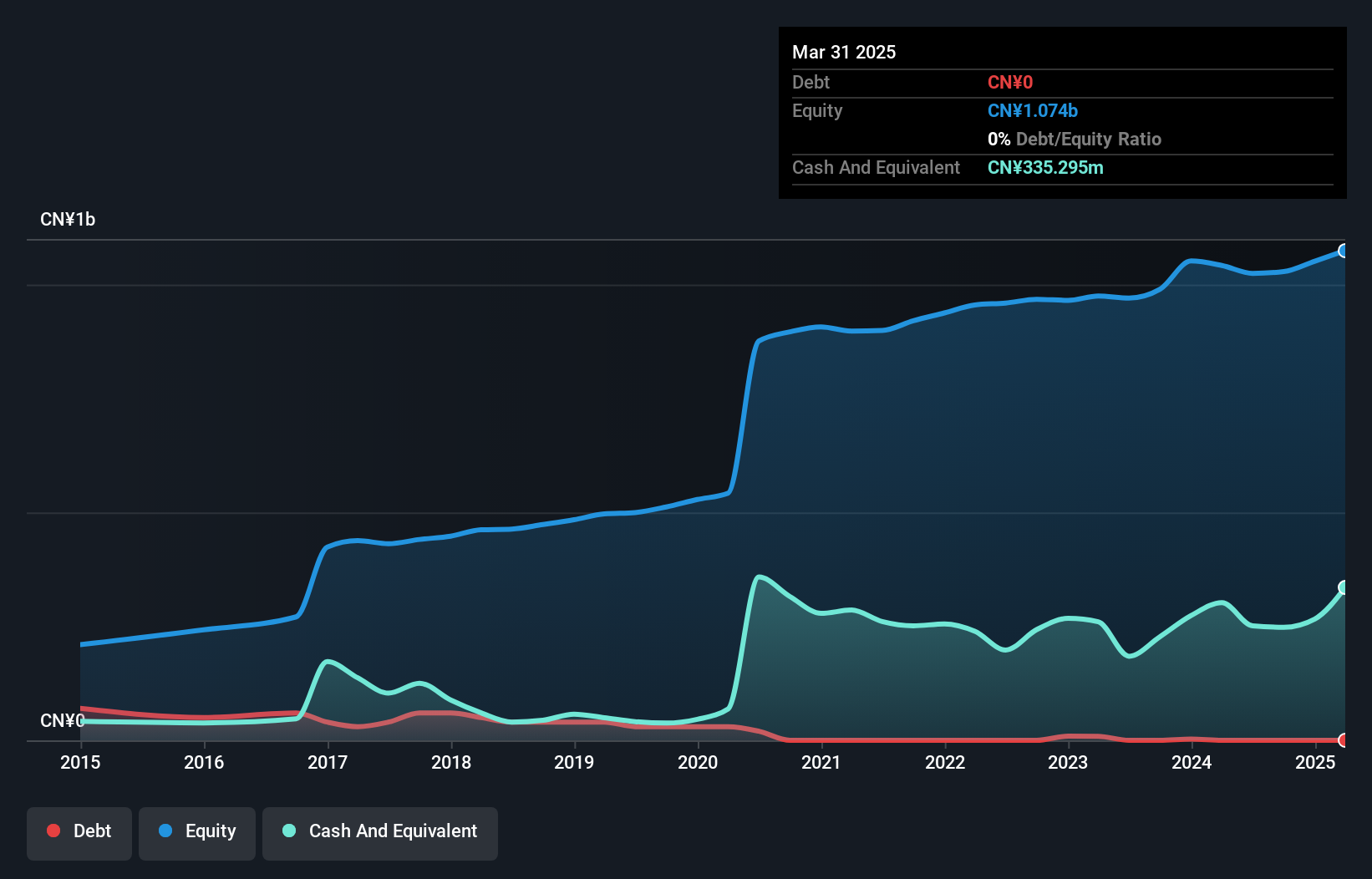

Shenyu Communication Technology (SZSE:300563)

Simply Wall St Value Rating: ★★★★★★

Overview: Shenyu Communication Technology Inc. focuses on the research, development, production, and sale of radio frequency coaxial cables in China with a market capitalization of CN¥9.89 billion.

Operations: Shenyu generates revenue primarily from the production and sales of coaxial cable products, amounting to CN¥816.30 million.

Shenyu Communication Technology, a small player in the communications sector, has shown impressive earnings growth of 226.8% over the past year, significantly outpacing its industry. The company reported net income of CNY 57.21 million for the first half of 2024, up from CNY 20.79 million a year prior. With no debt on its books and a history of high-quality earnings, Shenyu seems well-positioned despite recent share price volatility and declared dividends totaling CNY 0.07 per share recently confirmed this stability.

- Navigate through the intricacies of Shenyu Communication Technology with our comprehensive health report here.

Understand Shenyu Communication Technology's track record by examining our Past report.

Seize The Opportunity

- Unlock our comprehensive list of 903 Chinese Undiscovered Gems With Strong Fundamentals by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com