Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalTibet Tianlu Co., Ltd. (SHSE:600326) Looks Just Right With A 33% Price Jump

Tibet Tianlu Co., Ltd. (SHSE:600326) shares have continued their recent momentum with a 33% gain in the last month alone. Taking a wider view, although not as strong as the last month, the full year gain of 24% is also fairly reasonable.

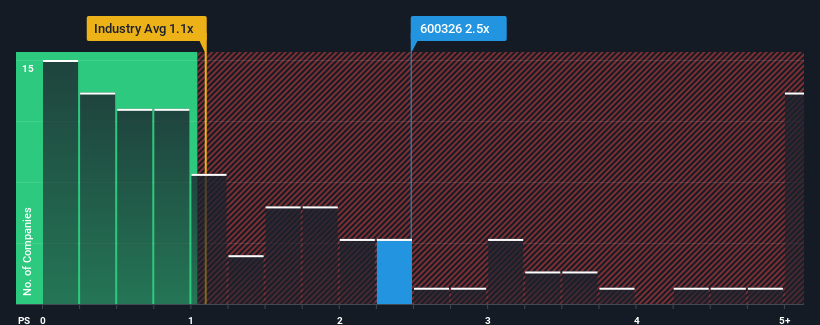

After such a large jump in price, when almost half of the companies in China's Construction industry have price-to-sales ratios (or "P/S") below 1.1x, you may consider Tibet Tianlu as a stock probably not worth researching with its 2.5x P/S ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the elevated P/S.

See our latest analysis for Tibet Tianlu

How Has Tibet Tianlu Performed Recently?

While the industry has experienced revenue growth lately, Tibet Tianlu's revenue has gone into reverse gear, which is not great. One possibility is that the P/S ratio is high because investors think this poor revenue performance will turn the corner. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Tibet Tianlu.Do Revenue Forecasts Match The High P/S Ratio?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Tibet Tianlu's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 4.1% decrease to the company's top line. This means it has also seen a slide in revenue over the longer-term as revenue is down 52% in total over the last three years. Accordingly, shareholders would have felt downbeat about the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 44% during the coming year according to the sole analyst following the company. That's shaping up to be materially higher than the 14% growth forecast for the broader industry.

In light of this, it's understandable that Tibet Tianlu's P/S sits above the majority of other companies. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Tibet Tianlu's P/S

Tibet Tianlu's P/S is on the rise since its shares have risen strongly. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our look into Tibet Tianlu shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless the analysts have really missed the mark, these strong revenue forecasts should keep the share price buoyant.

Before you take the next step, you should know about the 2 warning signs for Tibet Tianlu that we have uncovered.

If you're unsure about the strength of Tibet Tianlu's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.