Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalKRX Growth Companies With High Insider Ownership October 2024

Over the last 7 days, the South Korean market has remained flat, yet it has experienced a 3.8% increase over the past year with earnings forecasted to grow by 30% annually. In this context of steady growth and positive earnings outlook, companies with high insider ownership can be particularly attractive as they often signal confidence from those closest to the business and may align management's interests with those of shareholders.

Top 10 Growth Companies With High Insider Ownership In South Korea

| Name | Insider Ownership | Earnings Growth |

| People & Technology (KOSDAQ:A137400) | 16.4% | 35.6% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.8% | 49.1% |

| Bioneer (KOSDAQ:A064550) | 15.8% | 97.6% |

| Oscotec (KOSDAQ:A039200) | 26.1% | 122% |

| ALTEOGEN (KOSDAQ:A196170) | 26.6% | 99.5% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 105.8% |

| Vuno (KOSDAQ:A338220) | 19.4% | 110.9% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

| Techwing (KOSDAQ:A089030) | 18.7% | 83.6% |

| INTEKPLUS (KOSDAQ:A064290) | 16.3% | 96.7% |

Here we highlight a subset of our preferred stocks from the screener.

ALTEOGEN (KOSDAQ:A196170)

Simply Wall St Growth Rating: ★★★★★★

Overview: ALTEOGEN Inc. is a biotechnology company specializing in the development of long-acting biobetters, proprietary antibody-drug conjugates, and antibody biosimilars, with a market cap of ₩20.53 trillion.

Operations: The company's revenue is primarily derived from its biotechnology segment, totaling ₩90.79 billion.

Insider Ownership: 26.6%

Earnings Growth Forecast: 99.5% p.a.

ALTEOGEN is positioned for significant growth, with revenue projected to increase by 64.2% annually, outpacing the South Korean market's average. Despite past shareholder dilution, the company is expected to achieve profitability within three years and boasts a very high forecasted return on equity of 66.3%. Trading at 70.4% below its estimated fair value, ALTEOGEN presents potential upside as insider ownership remains stable without recent substantial insider trading activity.

- Get an in-depth perspective on ALTEOGEN's performance by reading our analyst estimates report here.

- Upon reviewing our latest valuation report, ALTEOGEN's share price might be too optimistic.

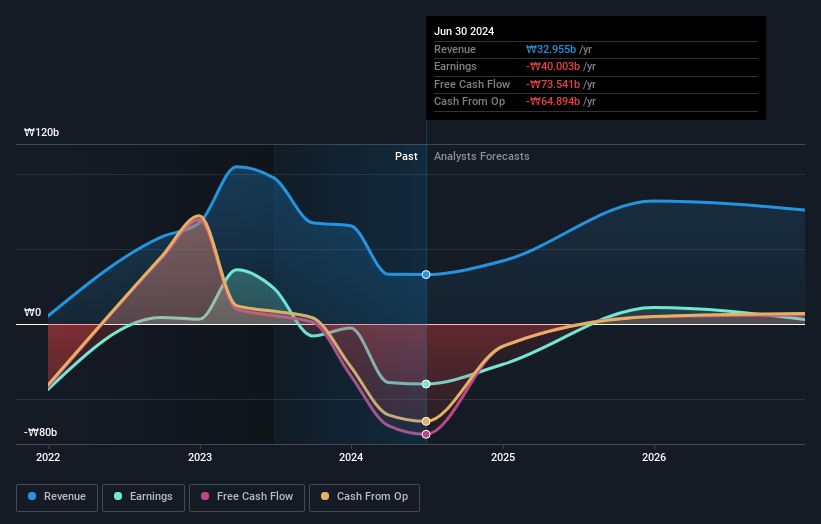

ABL Bio (KOSDAQ:A298380)

Simply Wall St Growth Rating: ★★★★★☆

Overview: ABL Bio Inc. is a biotech research company specializing in therapeutic drugs for immuno-oncology and neurodegenerative diseases, with a market cap of ₩1.96 trillion.

Operations: The company's revenue is primarily derived from its biotechnology startups segment, amounting to ₩32.95 billion.

Insider Ownership: 30.5%

Earnings Growth Forecast: 48.2% p.a.

ABL Bio is projected to grow revenue by 24.7% annually, surpassing the South Korean market average of 10.4%. The company is expected to achieve profitability within three years, reflecting above-average market growth. Despite a highly volatile share price recently and a forecasted low return on equity of 13%, ABL Bio's substantial insider ownership remains stable, with no significant insider trading activity reported in the past three months.

- Click here and access our complete growth analysis report to understand the dynamics of ABL Bio.

- Insights from our recent valuation report point to the potential overvaluation of ABL Bio shares in the market.

Doosan (KOSE:A000150)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Doosan Corporation operates in heavy industry, machinery manufacturing, and apartment construction across South Korea, the United States, Asia, the Middle East, Europe, and internationally with a market cap of ₩2.93 trillion.

Operations: The company's revenue is primarily derived from Doosan Bobcat at ₩9.31 billion, Doosan Energy at ₩8.25 billion, Electronic BG at ₩855.42 million, Doosan Fuel Cell at ₩279.99 million, and Digital Innovation BU at ₩286.29 million.

Insider Ownership: 38.9%

Earnings Growth Forecast: 65.5% p.a.

Doosan's earnings are forecast to grow significantly at 65.51% annually, with expectations of becoming profitable in the next three years, indicating above-average market growth. Despite trading at 62% below estimated fair value and having a volatile share price recently, its inclusion in the S&P Global BMI Index highlights its market relevance. Revenue growth is slower than both the industry and market averages, but high insider ownership suggests confidence in long-term potential.

- Dive into the specifics of Doosan here with our thorough growth forecast report.

- Our valuation report here indicates Doosan may be undervalued.

Taking Advantage

- Click through to start exploring the rest of the 83 Fast Growing KRX Companies With High Insider Ownership now.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com