Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalExploring Koshidaka Holdings And 2 Other Promising Small Caps with Robust Financials

Japan's stock markets have been on the rise recently, with the Nikkei 225 Index gaining 2.45% and the broader TOPIX Index up 0.45%, buoyed by yen weakness that has bolstered the profit outlook for exporters. In this favorable market environment, small-cap stocks with robust financials, such as Koshidaka Holdings and two other promising companies, present intriguing opportunities for investors seeking to explore lesser-known yet financially sound options in Japan's dynamic economy.

Top 10 Undiscovered Gems With Strong Fundamentals In Japan

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Intelligent Wave | NA | 6.92% | 15.18% | ★★★★★★ |

| Nitto Fuji Flour MillingLtd | 0.80% | 6.26% | 4.41% | ★★★★★★ |

| Central Forest Group | NA | 7.05% | 14.29% | ★★★★★★ |

| Otec | 9.81% | 2.32% | -1.39% | ★★★★★★ |

| HeadwatersLtd | NA | 19.26% | 23.89% | ★★★★★★ |

| Innotech | 38.96% | 7.08% | 6.36% | ★★★★★☆ |

| Imuraya Group | 26.21% | 2.37% | 32.09% | ★★★★★☆ |

| GENOVA | 0.93% | 33.82% | 30.22% | ★★★★☆☆ |

| Ogaki Kyoritsu Bank | 139.93% | 2.20% | -0.27% | ★★★★☆☆ |

| Nippon Sharyo | 61.34% | -1.68% | -17.07% | ★★★★☆☆ |

We'll examine a selection from our screener results.

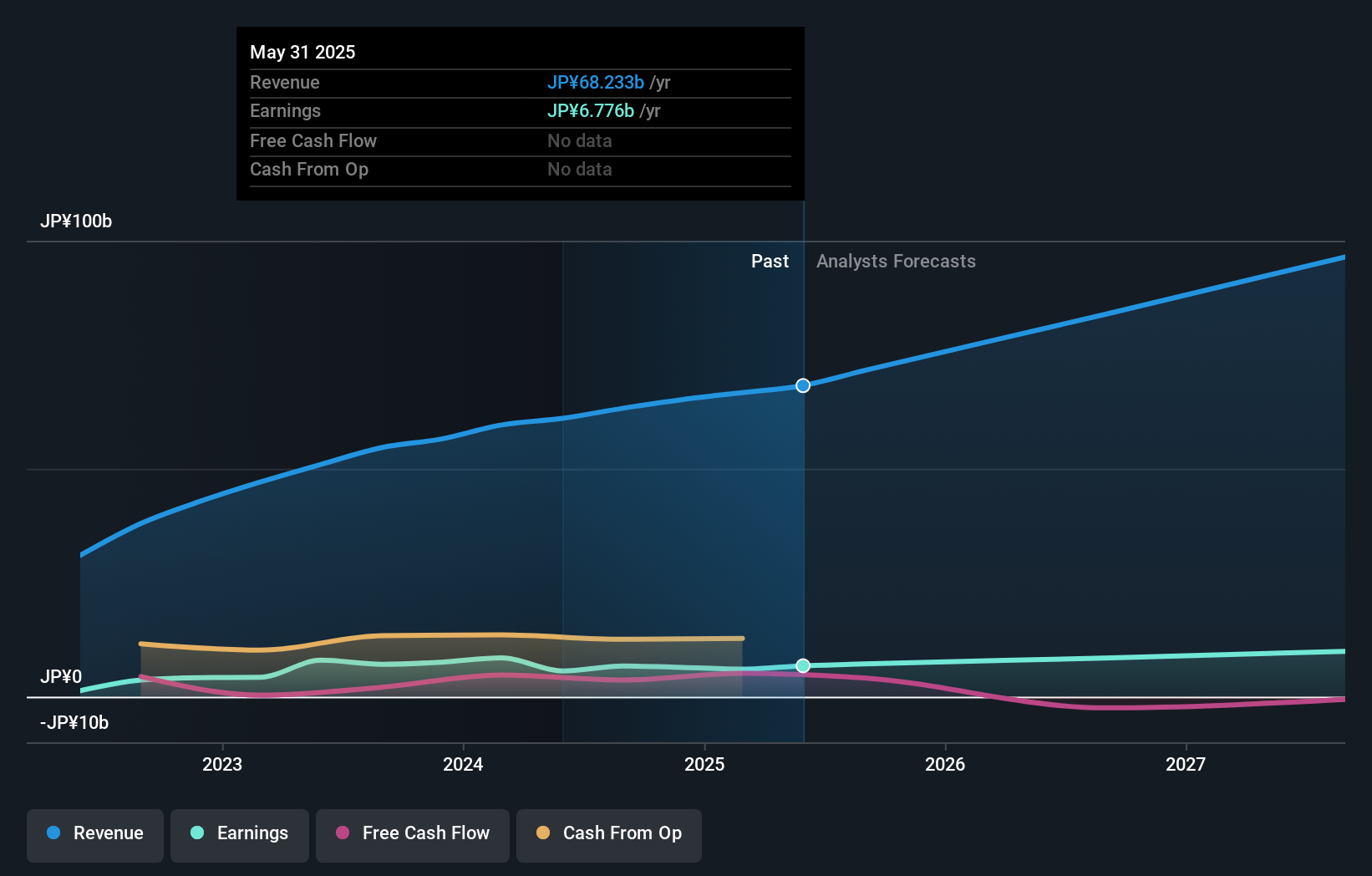

Koshidaka Holdings (TSE:2157)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Koshidaka Holdings Co., Ltd. is engaged in the operation of karaoke and bath house businesses both in Japan and internationally, with a market capitalization of approximately ¥95.03 billion.

Operations: Koshidaka Holdings generates revenue primarily from its karaoke business, which accounts for ¥61.25 billion, and also has a smaller segment in real estate management contributing ¥1.59 billion.

Koshidaka Holdings, a notable player in the hospitality sector, offers a compelling investment narrative. Despite facing negative earnings growth of 5.2% last year, it trades at an attractive price-to-earnings ratio of 14.1x, below the industry average of 21.9x. The company's debt management is commendable with its net debt to equity ratio reduced from 69.9% to 37.7% over five years and interest payments well-covered by EBIT at an impressive multiple of 1626x. Recent forecasts indicate expected net sales of ¥71 billion for fiscal year ending August 2025, alongside increased dividends from ¥11 to ¥12 per share reflecting confidence in future performance and shareholder value enhancement.

- Navigate through the intricacies of Koshidaka Holdings with our comprehensive health report here.

Gain insights into Koshidaka Holdings' past trends and performance with our Past report.

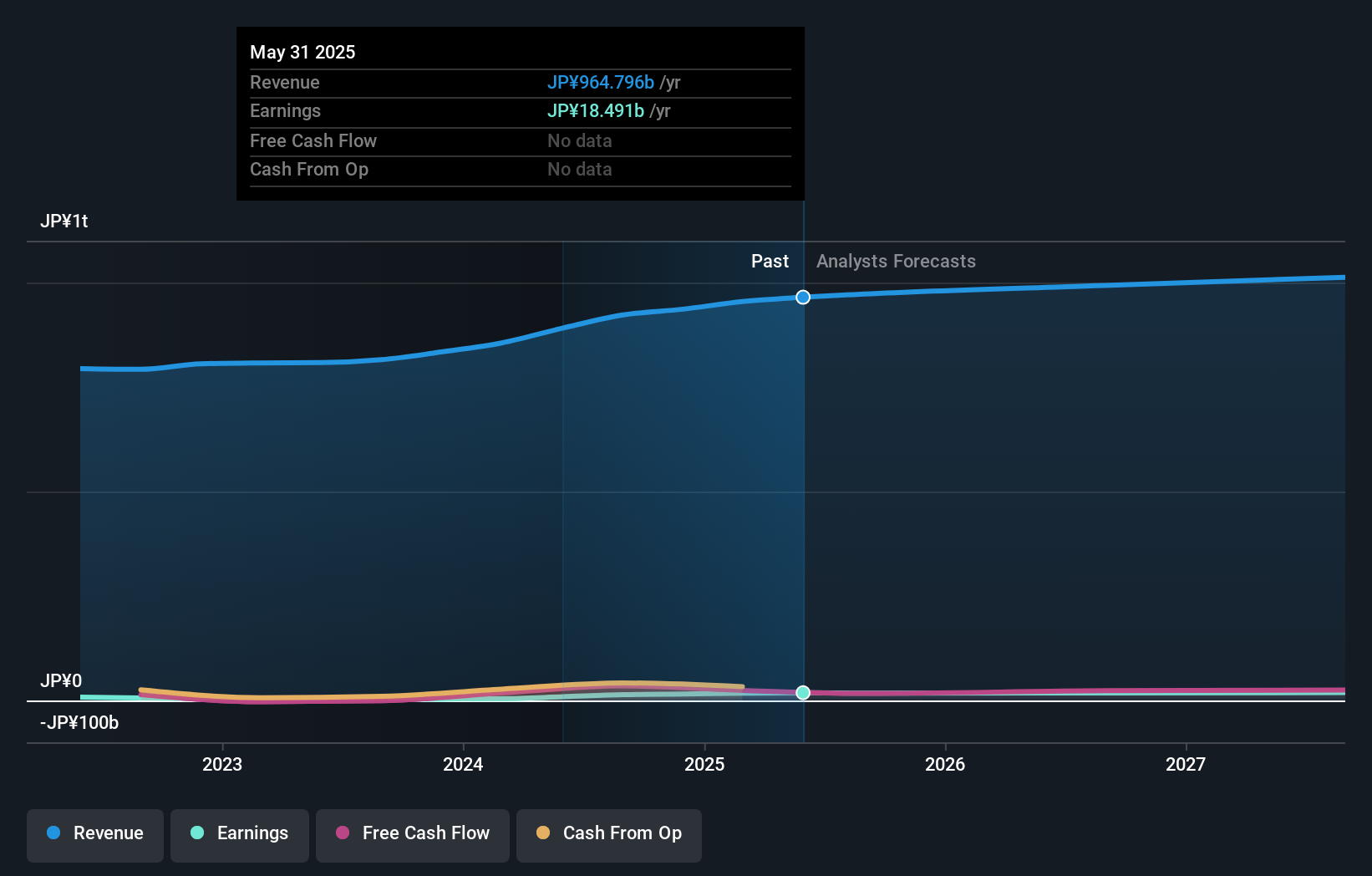

Bic Camera (TSE:3048)

Simply Wall St Value Rating: ★★★★★☆

Overview: Bic Camera Inc., along with its subsidiaries, operates in Japan as a manufacturer and retailer of audiovisual products, with a market capitalization of ¥294.78 billion.

Operations: Bic Camera generates revenue primarily through the sale of audiovisual products.

Bic Camera, a notable player in Japan's retail sector, has seen its earnings soar by 299% over the past year, outpacing the industry growth of 5%. Despite a significant one-off loss of ¥5.4 billion impacting recent financials, it maintains a satisfactory net debt to equity ratio at 26.7%. The company is trading slightly below its estimated fair value and forecasts suggest earnings could grow annually by nearly 14%, indicating potential for future expansion.

- Click here and access our complete health analysis report to understand the dynamics of Bic Camera.

Examine Bic Camera's past performance report to understand how it has performed in the past.

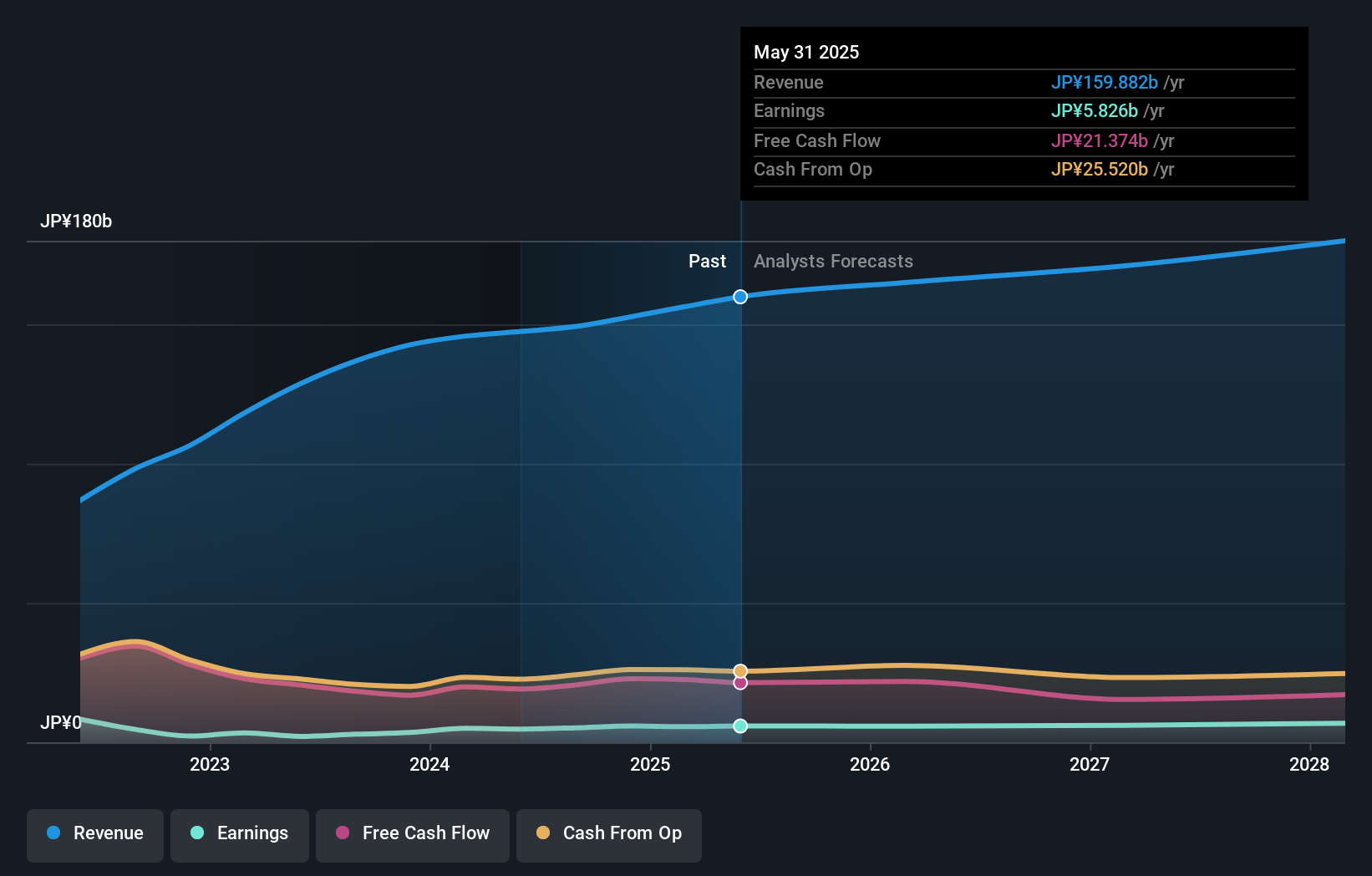

create restaurants holdings (TSE:3387)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Create Restaurants Holdings Inc. is engaged in planning, developing, and managing food courts, izakaya bars, dinner-time restaurants, and bakeries across Japan with a market capitalization of approximately ¥237.31 billion.

Operations: The company generates revenue primarily from its diverse portfolio of dining establishments, including food courts, izakaya bars, and bakeries. A significant portion of costs is attributed to operational expenses across these venues. The company's financial performance includes a notable net profit margin trend that warrants attention for potential investors.

With a net debt to equity ratio of 15.9%, Create Restaurants Holdings is on solid financial ground, having reduced this from 141.3% over five years. The company trades at 53.7% below its estimated fair value, suggesting potential upside. Its earnings have grown by an impressive 78.5% in the past year, outpacing the hospitality industry's average growth of 26.2%. Recent acquisitions are likely to boost revenue beyond previous forecasts, despite unchanged profit expectations due to integration costs.

- Get an in-depth perspective on create restaurants holdings' performance by reading our health report here.

Understand create restaurants holdings' track record by examining our Past report.

Turning Ideas Into Actions

- Gain an insight into the universe of 730 Japanese Undiscovered Gems With Strong Fundamentals by clicking here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com