Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street Journal3 Japanese Exchange Stocks That May Be Trading Below Intrinsic Value Estimates

Japan's stock markets have experienced a rise recently, with the Nikkei 225 Index gaining 2.45% and the TOPIX Index up by 0.45%, supported in part by yen weakness which has improved the profit outlook for exporters. In this context of market growth, identifying stocks that may be trading below their intrinsic value estimates can present potential opportunities for investors seeking to capitalize on undervalued assets within Japan's exchange landscape.

Top 10 Undervalued Stocks Based On Cash Flows In Japan

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Hagiwara Electric Holdings (TSE:7467) | ¥3475.00 | ¥6712.11 | 48.2% |

| Akatsuki (TSE:3932) | ¥2049.00 | ¥3746.87 | 45.3% |

| Management SolutionsLtd (TSE:7033) | ¥1885.00 | ¥3765.37 | 49.9% |

| Pilot (TSE:7846) | ¥4684.00 | ¥8892.46 | 47.3% |

| Eternal Hospitality GroupLtd (TSE:3193) | ¥4110.00 | ¥7799.68 | 47.3% |

| Appier Group (TSE:4180) | ¥1743.00 | ¥3466.52 | 49.7% |

| Hibino (TSE:2469) | ¥3565.00 | ¥6935.44 | 48.6% |

| Medley (TSE:4480) | ¥3955.00 | ¥7909.34 | 50% |

| freee K.K (TSE:4478) | ¥3255.00 | ¥6057.65 | 46.3% |

| Money Forward (TSE:3994) | ¥6283.00 | ¥11797.87 | 46.7% |

Let's take a closer look at a couple of our picks from the screened companies.

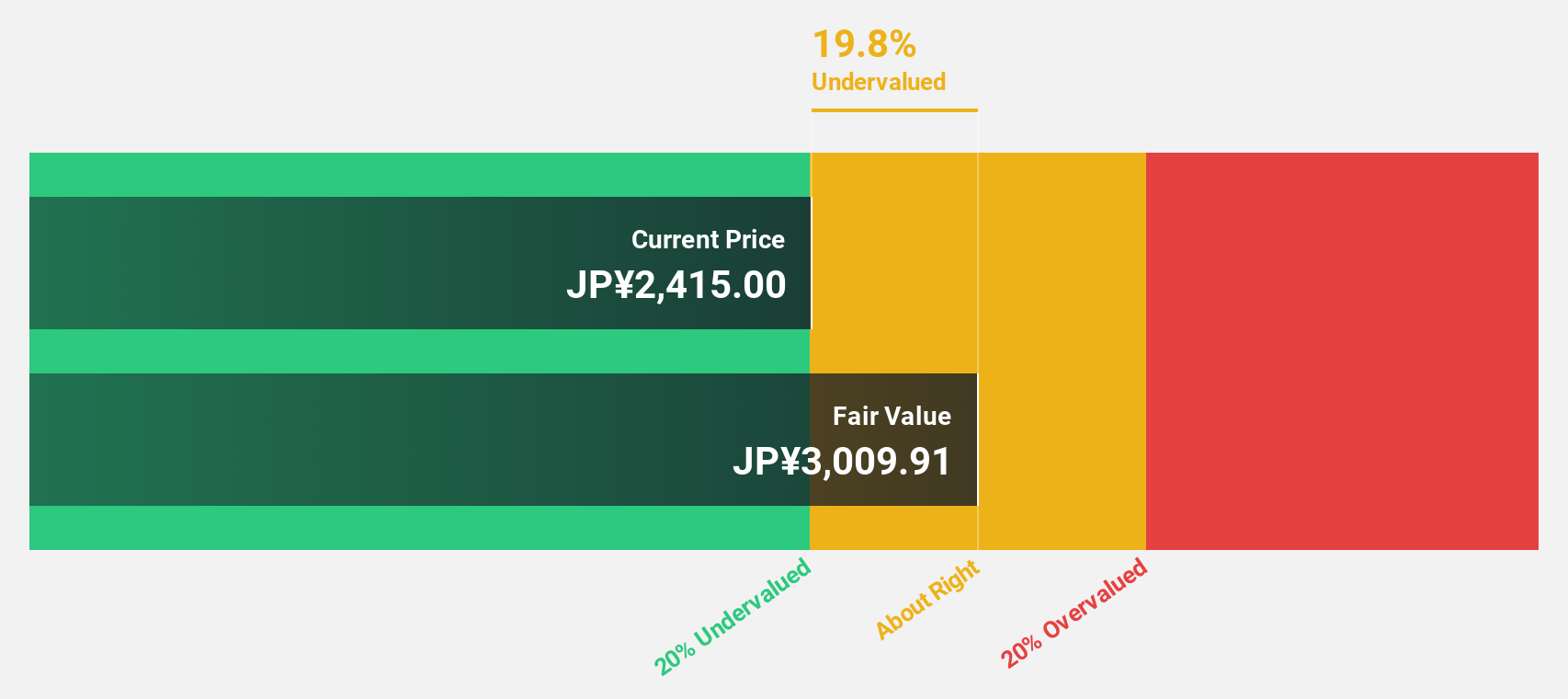

Shiseido Company (TSE:4911)

Overview: Shiseido Company, Limited is involved in the production and sale of cosmetics both in Japan and internationally, with a market cap of ¥1.47 trillion.

Operations: The company's revenue segments include the Japan Business at ¥279.41 billion, China Business at ¥253.08 billion, Travel Retail Business at ¥122.20 billion, Americas Business at ¥120.34 billion, EMEA Business at ¥134.42 million, and Asia-Pacific Business at ¥76.29 million.

Estimated Discount To Fair Value: 12%

Shiseido Company is trading at ¥3,686, slightly below its estimated fair value of ¥4,190.23, suggesting potential undervaluation based on cash flows. Despite low profit margins and a forecasted return on equity of 10.4%, earnings are expected to grow significantly at 35.8% annually over the next three years—outpacing the Japanese market's growth rate. Recent executive changes and share buybacks may influence future performance, with leadership transitions effective January 2025.

- Our expertly prepared growth report on Shiseido Company implies its future financial outlook may be stronger than recent results.

- Take a closer look at Shiseido Company's balance sheet health here in our report.

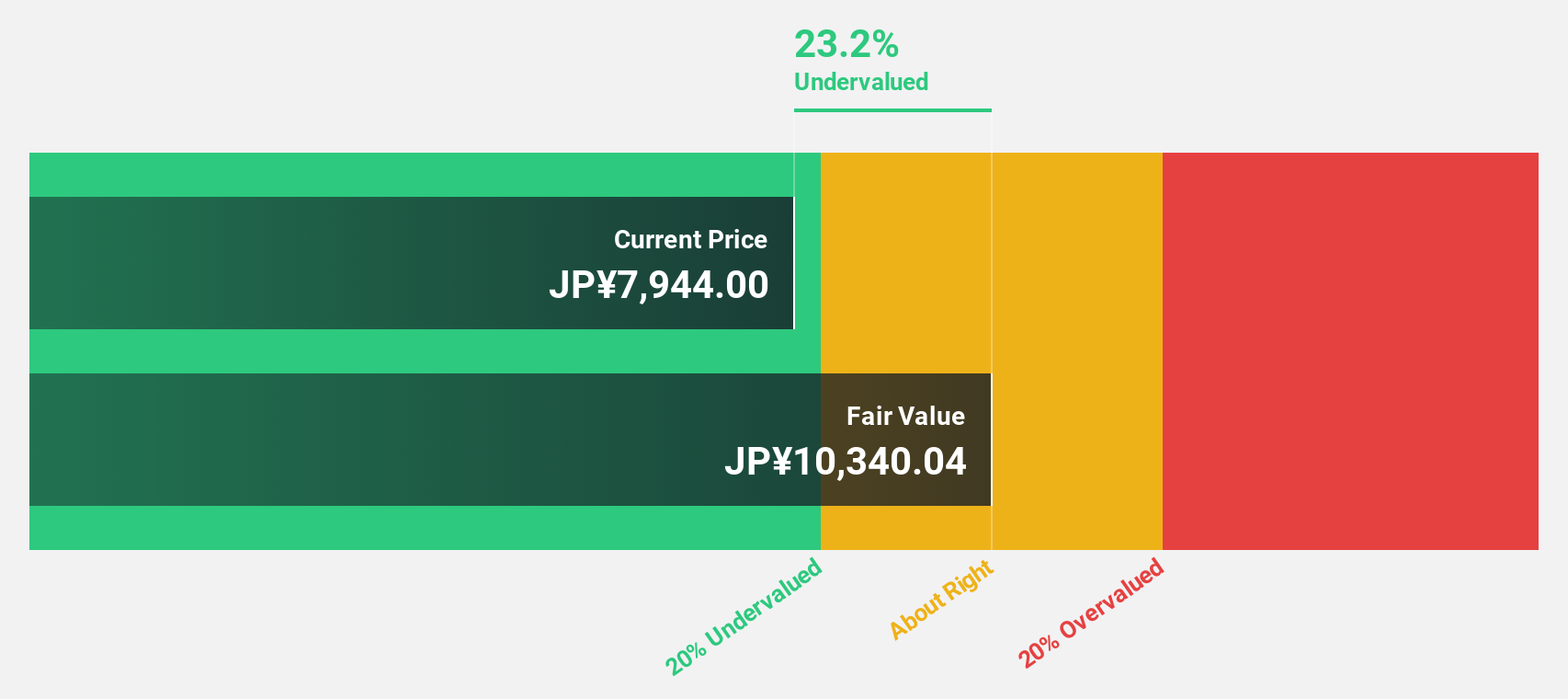

BayCurrent Consulting (TSE:6532)

Overview: BayCurrent Consulting, Inc. offers consulting services in Japan and has a market cap of ¥843.72 billion.

Operations: The company's revenue segments are not specified in the provided text.

Estimated Discount To Fair Value: 34.4%

BayCurrent Consulting, trading at ¥5,561, is significantly undervalued compared to its estimated fair value of ¥8,473.71. Forecasts indicate earnings and revenue growth rates of 18.4% and 17.8% annually, respectively—surpassing the Japanese market averages. With a projected return on equity of 35.4% in three years, the company shows strong financial health despite not achieving significant annual profit growth above 20%. Upcoming Q2 results may provide further insights into performance trends.

- The growth report we've compiled suggests that BayCurrent Consulting's future prospects could be on the up.

- Click to explore a detailed breakdown of our findings in BayCurrent Consulting's balance sheet health report.

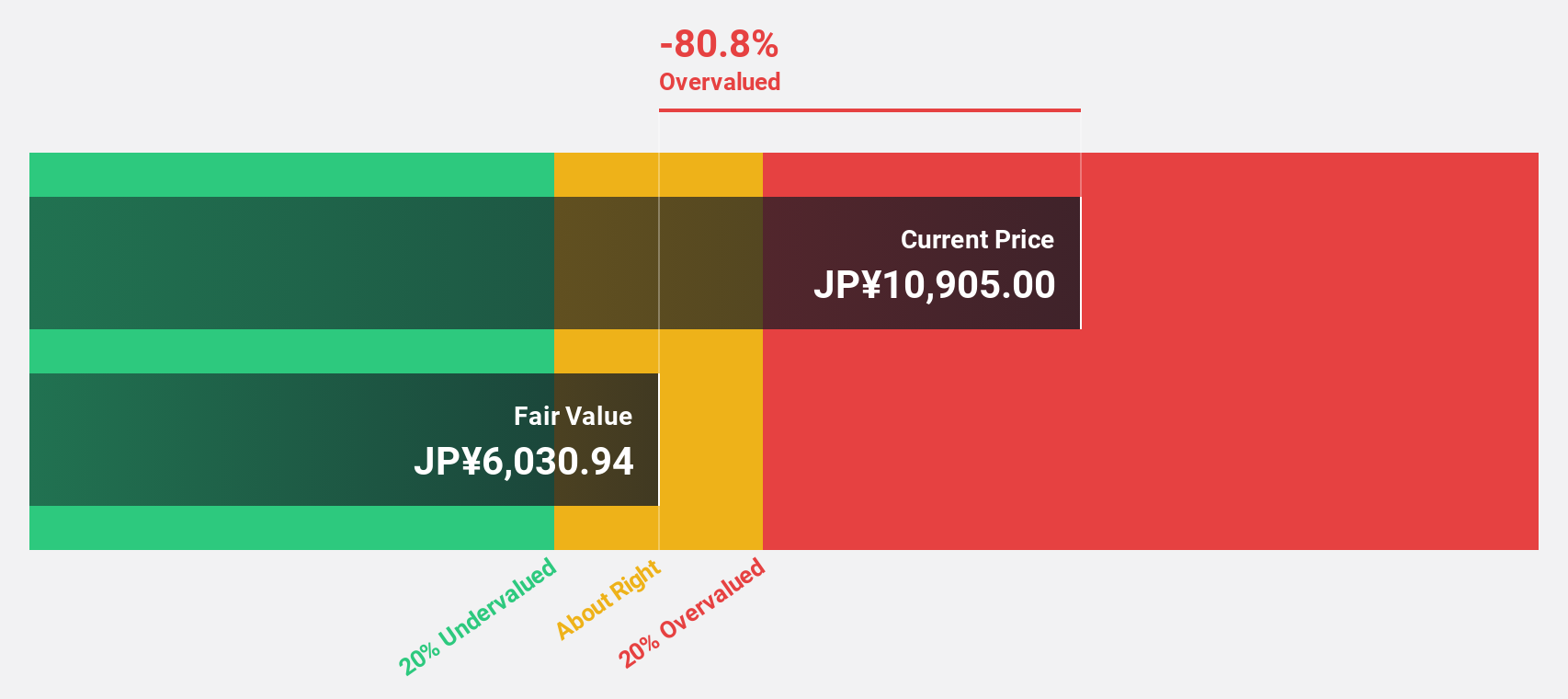

Kawasaki Heavy Industries (TSE:7012)

Overview: Kawasaki Heavy Industries, Ltd. operates in aerospace systems, energy solutions and marine engineering, precision machinery and robotics, rolling stock, and motorcycle and engine sectors both in Japan and internationally with a market cap of ¥1.10 trillion.

Operations: The company's revenue segments include Aerospace Business at ¥435.40 billion, Power Sports & Engine at ¥594.38 billion, Energy Solutions & Marine at ¥388.09 billion, Precision Machinery / Robot at ¥249.35 billion, and Vehicle at ¥196.26 billion.

Estimated Discount To Fair Value: 14.8%

Kawasaki Heavy Industries, trading at ¥6,563, is undervalued compared to its estimated fair value of ¥7,702.15. While earnings are projected to grow significantly at 22.1% annually—surpassing the Japanese market's growth rate—the company's debt is not well covered by operating cash flow, and profit margins have decreased from last year. Despite a volatile share price and low future return on equity forecasts (13%), revenue growth outpaces the market average.

- Our growth report here indicates Kawasaki Heavy Industries may be poised for an improving outlook.

- Navigate through the intricacies of Kawasaki Heavy Industries with our comprehensive financial health report here.

Turning Ideas Into Actions

- Delve into our full catalog of 82 Undervalued Japanese Stocks Based On Cash Flows here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com