Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street Journal3 ASX Stocks Estimated To Be Undervalued By Up To 48.8% Offering Investment Opportunities

The Australian stock market has remained flat over the past week but has experienced a notable 17% increase over the last year, with earnings projected to grow by 12% annually. In this context, identifying undervalued stocks can present compelling opportunities for investors seeking to capitalize on potential growth and value in a thriving market environment.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Accent Group (ASX:AX1) | A$2.44 | A$4.81 | 49.3% |

| Mader Group (ASX:MAD) | A$5.74 | A$10.42 | 44.9% |

| MLG Oz (ASX:MLG) | A$0.62 | A$1.15 | 46.1% |

| Charter Hall Group (ASX:CHC) | A$16.10 | A$31.43 | 48.8% |

| Ingenia Communities Group (ASX:INA) | A$5.00 | A$9.40 | 46.8% |

| Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

| Little Green Pharma (ASX:LGP) | A$0.092 | A$0.17 | 45.7% |

| Ai-Media Technologies (ASX:AIM) | A$0.78 | A$1.42 | 44.9% |

| Superloop (ASX:SLC) | A$1.83 | A$3.31 | 44.7% |

| Mineral Resources (ASX:MIN) | A$50.24 | A$95.42 | 47.4% |

Let's take a closer look at a couple of our picks from the screened companies.

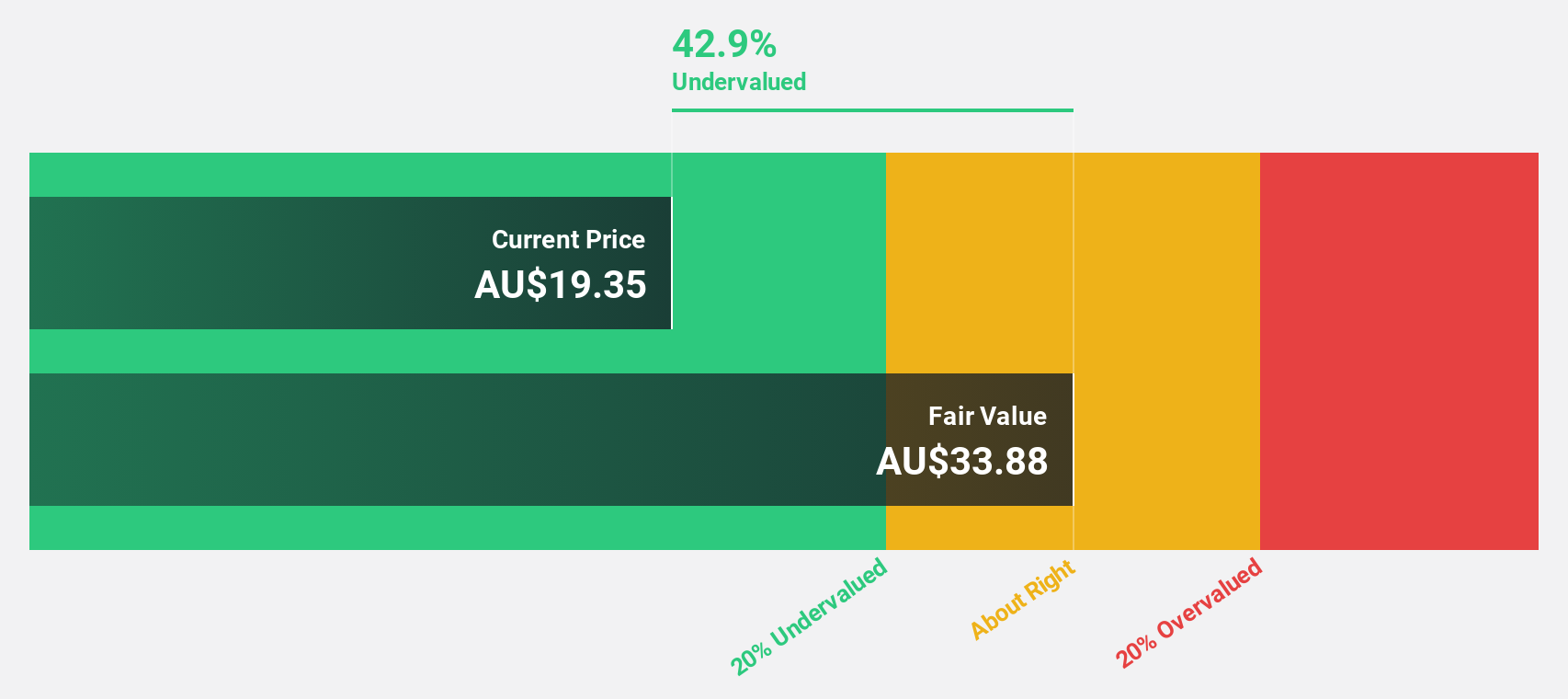

Charter Hall Group (ASX:CHC)

Overview: Charter Hall Group (ASX:CHC) is a prominent Australian fully integrated property investment and funds management company with a market cap of A$7.62 billion.

Operations: The company's revenue is derived from three main segments: Funds Management at A$448.60 million, Property Investments at A$322.80 million, and Development Investments at A$73.30 million.

Estimated Discount To Fair Value: 48.8%

Charter Hall Group is trading significantly below its estimated fair value, with a current price of A$16.1 compared to a fair value estimate of A$31.43, suggesting potential undervaluation based on cash flows. Despite recent financial setbacks, including a net loss of A$222.1 million for FY24 and decreased revenues, the company forecasts earnings growth and aims for 6% distribution growth in FY25. Its revenue is expected to grow at 8.5% annually, outpacing the broader Australian market's growth rate.

- Our expertly prepared growth report on Charter Hall Group implies its future financial outlook may be stronger than recent results.

- Click to explore a detailed breakdown of our findings in Charter Hall Group's balance sheet health report.

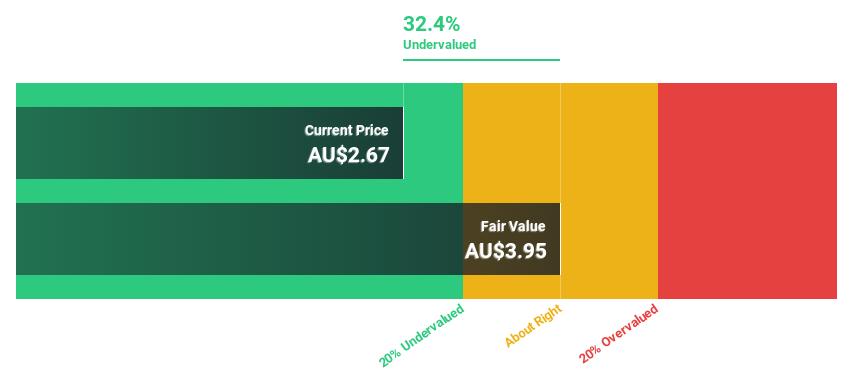

Megaport (ASX:MP1)

Overview: Megaport Limited offers on-demand interconnection and internet exchange services to enterprises and service providers across regions including Australia, New Zealand, Hong Kong, Singapore, Japan, North America, Italy, and Europe with a market cap of A$1.19 billion.

Operations: The company's revenue segments consist of A$31.88 million from Europe, A$52.58 million from Asia-Pacific, and A$110.81 million from North America.

Estimated Discount To Fair Value: 42.7%

Megaport is trading at A$7.71, significantly below its estimated fair value of A$13.47, indicating potential undervaluation based on cash flows. The company recently turned profitable with a net income of A$9.61 million for FY24 and expects earnings to grow 32.1% annually over the next three years, outpacing the Australian market's growth rate. Its strategic expansion into Italy enhances its global presence and could drive future revenue growth beyond the forecasted 13.4% per year increase.

- The analysis detailed in our Megaport growth report hints at robust future financial performance.

- Get an in-depth perspective on Megaport's balance sheet by reading our health report here.

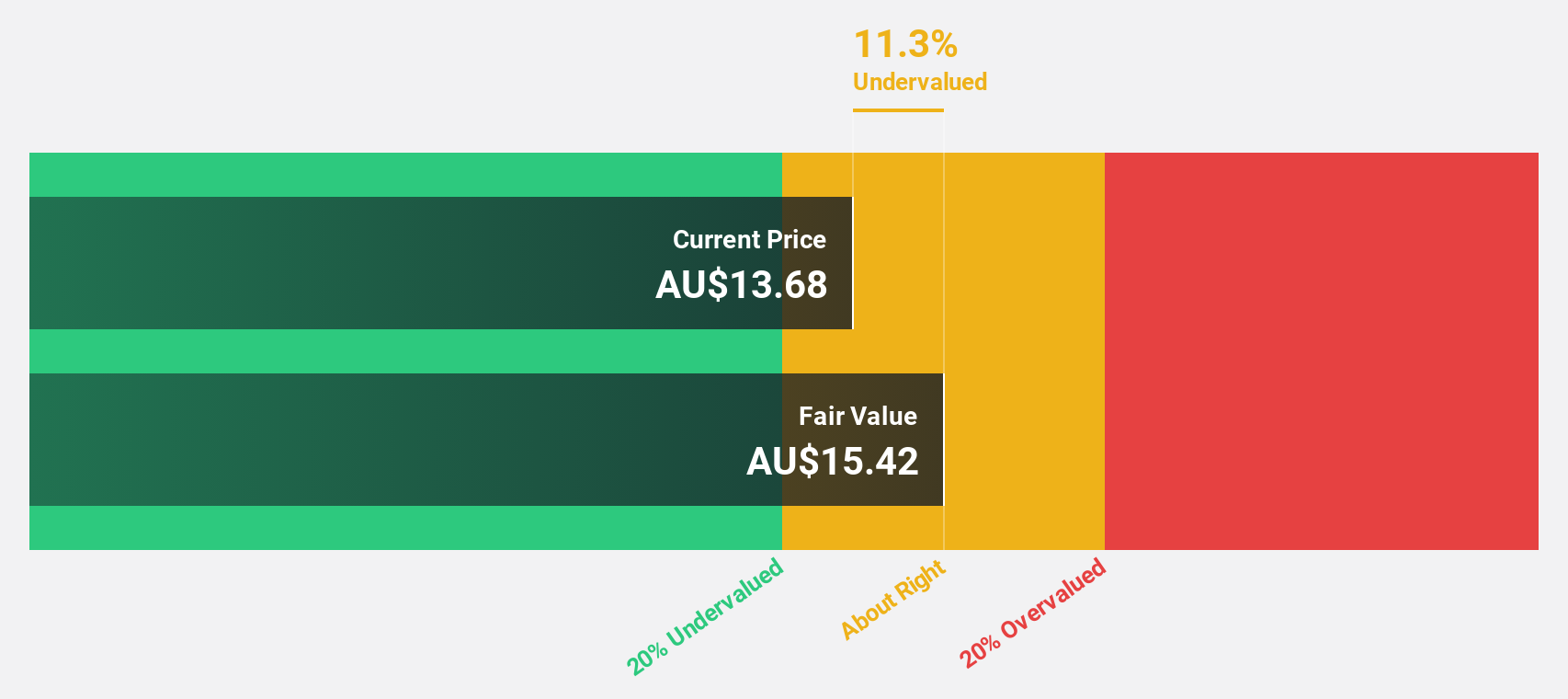

Westgold Resources (ASX:WGX)

Overview: Westgold Resources Limited is involved in the exploration, operation, development, mining, and treatment of gold and other assets mainly in Western Australia with a market cap of A$2.45 billion.

Operations: The company's revenue segments consist of A$183.25 million from Bryah and A$533.23 million from Murchison.

Estimated Discount To Fair Value: 30.6%

Westgold Resources is trading at A$2.60, below its estimated fair value of A$3.75, suggesting potential undervaluation based on cash flows. Earnings are projected to grow 26.1% annually over the next three years, surpassing the Australian market's growth rate. Recent executive changes and record gold production of 77,369 ounces in Q1 FY25 highlight operational advancements post-merger with Karora Resources, potentially bolstering future cash flow and financial performance.

- The growth report we've compiled suggests that Westgold Resources' future prospects could be on the up.

- Take a closer look at Westgold Resources' balance sheet health here in our report.

Next Steps

- Get an in-depth perspective on all 45 Undervalued ASX Stocks Based On Cash Flows by using our screener here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com