Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street Journal3 Euronext Amsterdam Growth Stocks With Insider Ownership And Up To 108% Earnings Growth

As European markets show signs of optimism with the pan-European STOXX Europe 600 Index ending higher, investors are keenly observing the potential for interest rate cuts by the European Central Bank and increased economic stimulus from China. In this context, growth companies in the Netherlands with significant insider ownership present intriguing opportunities, as they often reflect strong confidence from those closest to the business. Identifying stocks that combine robust earnings growth with high insider ownership can be a strategic approach in navigating today's market dynamics.

Top 5 Growth Companies With High Insider Ownership In The Netherlands

| Name | Insider Ownership | Earnings Growth |

| Envipco Holding (ENXTAM:ENVI) | 36.7% | 84.4% |

| Ebusco Holding (ENXTAM:EBUS) | 31% | 107.8% |

| MotorK (ENXTAM:MTRK) | 35.7% | 108.4% |

| Basic-Fit (ENXTAM:BFIT) | 12% | 77.7% |

| CVC Capital Partners (ENXTAM:CVC) | 20.2% | 33.5% |

| PostNL (ENXTAM:PNL) | 35.6% | 36.4% |

Let's dive into some prime choices out of the screener.

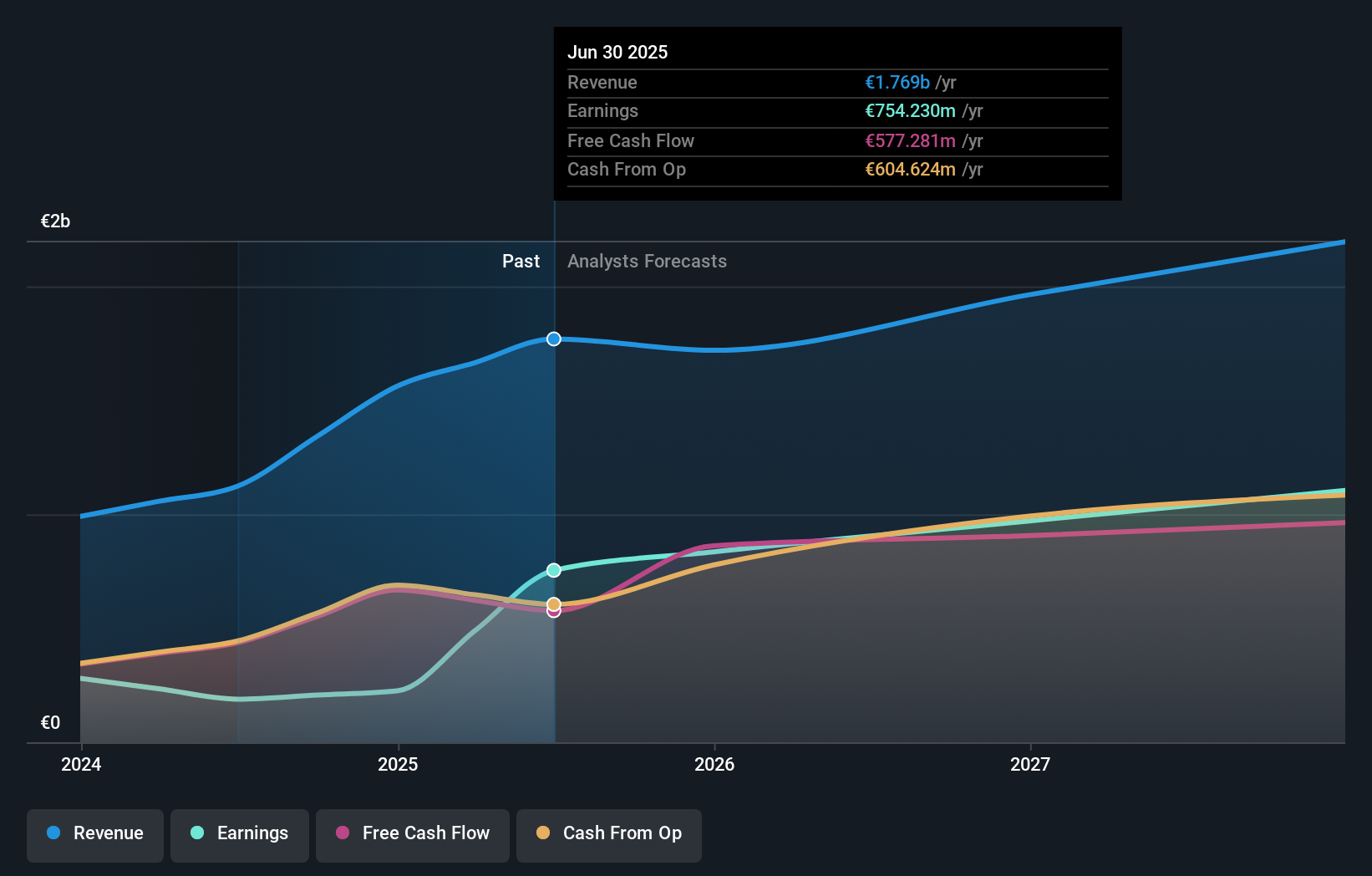

CVC Capital Partners (ENXTAM:CVC)

Simply Wall St Growth Rating: ★★★★★☆

Overview: CVC Capital Partners plc is a private equity and venture capital firm that specializes in middle market secondaries, infrastructure and credit, management buyouts, leveraged buyouts, growth equity, mature investments, recapitalizations, strip sales, and spinouts with a market cap of €21.26 billion.

Operations: Revenue segments for the firm include middle market secondaries, infrastructure and credit, management buyouts, leveraged buyouts, growth equity, mature investments, recapitalizations, strip sales, and spinouts.

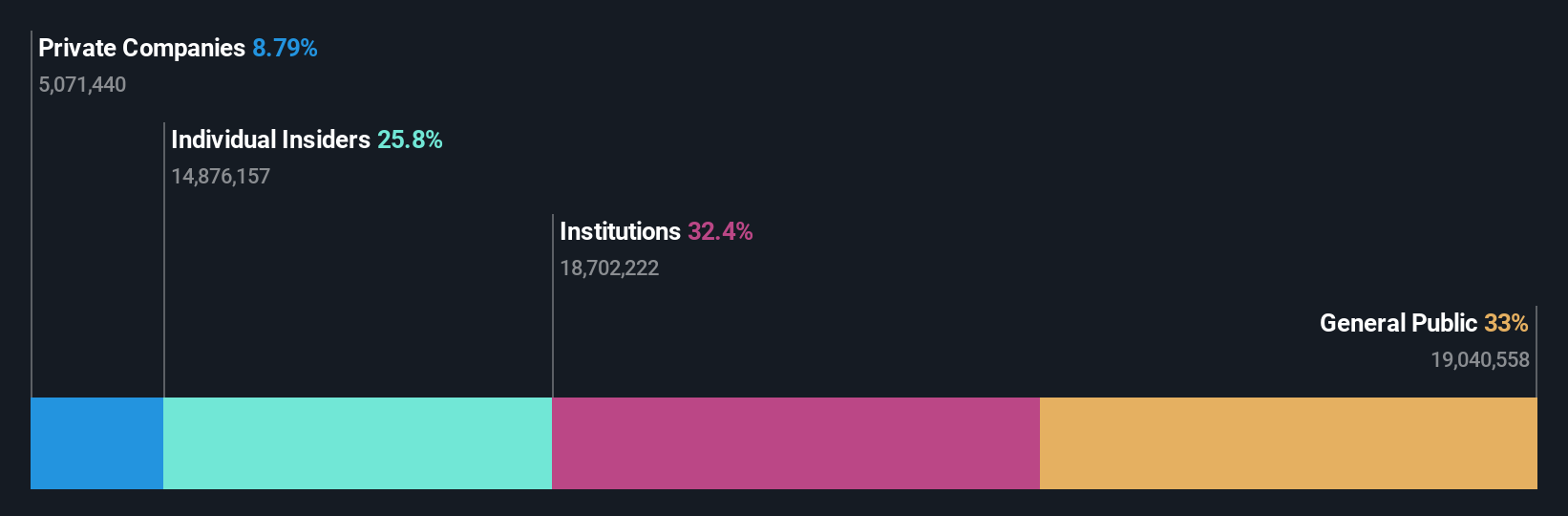

Insider Ownership: 20.2%

Earnings Growth Forecast: 33.5% p.a.

CVC Capital Partners, a private equity firm in the Netherlands, is experiencing significant growth with earnings expected to increase by 33.52% annually, outpacing the Dutch market. Despite trading at 22.3% below its estimated fair value, CVC's revenue growth forecast of 13.6% per year surpasses the local market average of 9.5%. Recent M&A activities highlight CVC's strategic ambitions and adaptability in competitive environments, although the company maintains a high debt level which investors should consider carefully.

- Unlock comprehensive insights into our analysis of CVC Capital Partners stock in this growth report.

- Our comprehensive valuation report raises the possibility that CVC Capital Partners is priced higher than what may be justified by its financials.

Envipco Holding (ENXTAM:ENVI)

Simply Wall St Growth Rating: ★★★★★★

Overview: Envipco Holding N.V. designs, manufactures, and services reverse vending machines for used beverage container collection in the Netherlands, North America, and Europe, with a market cap of €297.11 million.

Operations: Envipco Holding N.V. generates revenue by designing, developing, and servicing reverse vending machines that facilitate the collection and processing of used beverage containers across the Netherlands, North America, and Europe.

Insider Ownership: 36.7%

Earnings Growth Forecast: 84.4% p.a.

Envipco Holding, a Dutch company with substantial insider ownership, is poised for strong growth. Its revenue is forecast to grow at 34.6% annually, significantly outpacing the Dutch market average of 9.5%. The company's earnings are expected to increase by 84.4% per year, driven by recent orders from a major Romanian retail group for its Optima RVMs. Despite past share dilution and volatility in share price, Envipco's profitability has improved this year with reduced net losses reported.

- Delve into the full analysis future growth report here for a deeper understanding of Envipco Holding.

- Upon reviewing our latest valuation report, Envipco Holding's share price might be too optimistic.

MotorK (ENXTAM:MTRK)

Simply Wall St Growth Rating: ★★★★★☆

Overview: MotorK plc offers software-as-a-service solutions for the automotive retail industry across Italy, Spain, France, Germany, and the Benelux Union with a market cap of €253.82 million.

Operations: The company's revenue primarily comes from its Software & Programming segment, which generated €42.50 million.

Insider Ownership: 35.7%

Earnings Growth Forecast: 108.4% p.a.

MotorK, with significant insider ownership, is on a path to profitability within three years, boasting an expected annual profit growth above the market average. Revenue is projected to grow at 22.1% annually, outpacing the Dutch market. Despite recent share price volatility and past dilution, its financial position remains challenging with less than a year of cash runway. Recent executive changes include Zoltan Gelencser as CFO, potentially strengthening its financial leadership team.

- Click here to discover the nuances of MotorK with our detailed analytical future growth report.

- Our valuation report here indicates MotorK may be overvalued.

Turning Ideas Into Actions

- Navigate through the entire inventory of 6 Fast Growing Euronext Amsterdam Companies With High Insider Ownership here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com