Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalMicrosoft [0 NasdaqGS:MSFT Name: unique_symbol, dtype: object] Boosts Healthcare with AI Innovations and Strategic Alliances

Microsoft (NasdaqGS:MSFT) is currently experiencing a mix of growth and challenges, driven by its strategic focus on AI and Cloud innovation, which has significantly boosted its financial performance. However, the company faces pressures from operating margin declines and competitive threats in these key sectors. In the discussion that follows, we will explore Microsoft's financial health, market opportunities, operational hurdles, and regulatory concerns to provide a comprehensive understanding of its current business dynamics.

Unlock comprehensive insights into our analysis of Microsoft stock here.

Innovative Factors Supporting Microsoft

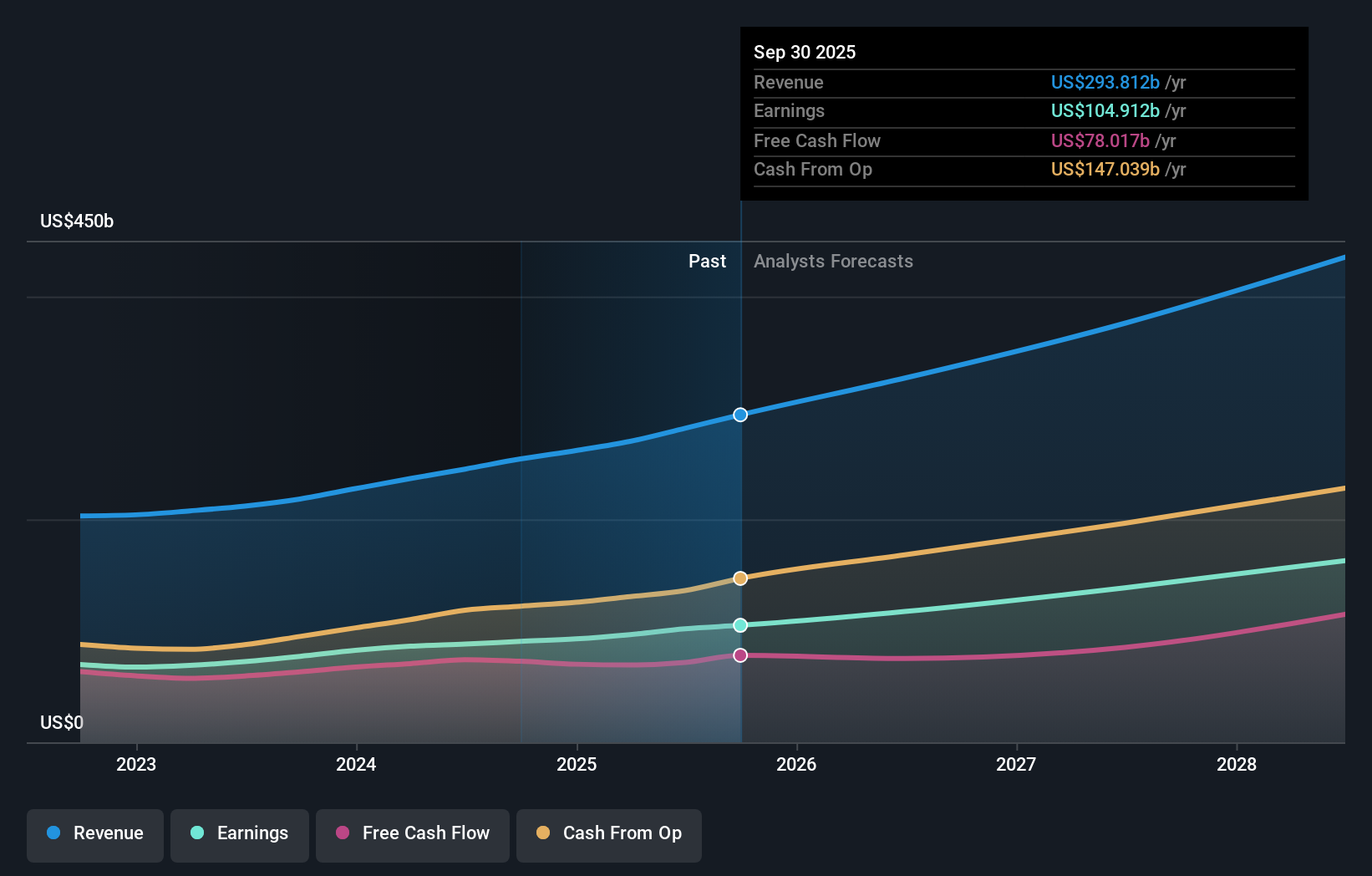

Microsoft's financial performance is evident with its annual revenue surpassing $245 billion, marking a 15% year-over-year increase, as noted by CEO Satya Nadella. The company's strategic focus on AI and Cloud innovation has driven significant growth, with Microsoft Cloud revenue exceeding $135 billion, up 23%. This growth is supported by a strong customer base expansion, including a 90% increase in Arc customers. Microsoft's commitment to security, with 1.2 million security customers, and substantial cash flow from operations reaching $119 billion, further underscore its financial health. Despite being considered expensive compared to peers with a Price-To-Earnings Ratio of 35.3x, Microsoft is undervalued relative to its estimated fair value of $573.39, highlighting its strong market positioning.

Vulnerabilities Impacting Microsoft

Challenges are present, particularly with operating margin pressures, as the Microsoft Cloud gross margin percentage decreased by 2 points year-over-year to 69%, according to CFO Amy Hood. The Activision acquisition, while contributing to revenue growth, exerted a 2-point drag on operating income growth. Additionally, device revenue saw an 11% decrease, reflecting performance issues in this segment. Microsoft's Price-To-Earnings Ratio, while lower than the US Software industry average, is higher than the peer average, indicating a potential overvaluation relative to peers. Furthermore, the moderated growth in certain segments, such as Office 365 Commercial seats, which grew only 7% year-over-year, suggests areas needing improvement.

Emerging Markets Or Trends for Microsoft

Opportunities abound in the AI and Cloud sectors, with Microsoft investing in long-term innovation and people, as emphasized by Satya Nadella. The introduction of new product categories, like Copilot+ PCs, and the growing engagement on LinkedIn, which continues to see record growth, are promising developments. The market demand for AI is expected to drive Azure's growth, with capital investments enhancing AI capacity. Strategic alliances, such as the recent partnership with Infosys to accelerate AI adoption, further position Microsoft to capitalize on emerging opportunities and expand its market presence.

Regulatory Challenges Facing Microsoft

However, competitive pressures in AI and Cloud from other tech giants pose significant threats, as these sectors are crucial to Microsoft's growth strategy. Economic challenges in Europe, with slightly lower-than-expected growth in certain regions, add to the complexities. Capacity constraints in AI, as highlighted by Amy Hood, could hinder Microsoft's ability to meet growing demand. Additionally, regulatory risks remain a concern, with the company's VP of Investor Relations, Brett Iversen, noting the potential for unforeseen legal challenges. These factors could impact Microsoft's long-term growth and market share if not addressed strategically.

To dive deeper into how Microsoft's valuation metrics are shaping its market position, check out our detailed analysis of Microsoft's Valuation.Conclusion

Microsoft's strong financial performance, driven by its strategic focus on AI and Cloud innovation, positions it well for future growth despite current challenges. While the company's Price-To-Earnings Ratio of 35.3x suggests a higher cost compared to peers, its estimated fair value of $573.39 indicates significant potential for appreciation. This discrepancy highlights Microsoft's strong market positioning and potential for long-term value creation. However, to sustain its growth trajectory, Microsoft must address margin pressures, regulatory risks, and competitive threats, particularly in AI and Cloud sectors, while capitalizing on emerging opportunities such as AI-driven Azure growth and strategic partnerships.

Turning Ideas Into Actions

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.