Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

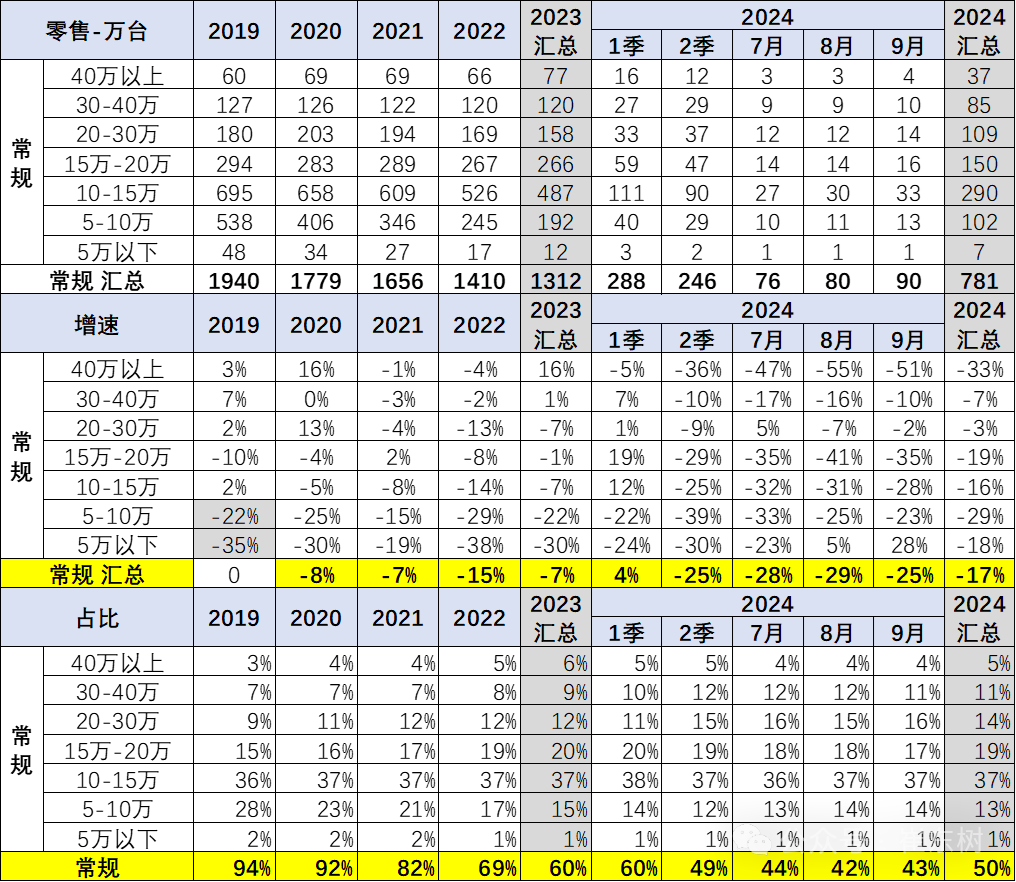

Wall Street JournalCui Dongshu: The new energy market under 100,000 yuan strengthened in the third quarter, and the trend of 50,000 yuan pure electric vehicles improved

The Zhitong Finance App learned that on October 15, Cui Dongshu released an analysis of the passenger car price segment market structure. According to data from the Passenger Federation, the price segment sales structure trend in the national passenger car market has continued to rise in recent years. The share of sales of high-end models has increased markedly, and the share of sales of medium- and low-price models has decreased. This is driving consumption upgrading, and it is also driven by the consumption upgrade of purchasers. With the implementation of the national scrap renewal subsidy policy, the new energy market of less than 100,000 yuan strengthened in the 3rd quarter of 2024, the trend of 50,000 yuan pure electric vehicles improved, and the 100,000 yuan hybrid grew rapidly, further dividing the fuel vehicle market share.

1. The lower the price of passenger cars, the more expensive

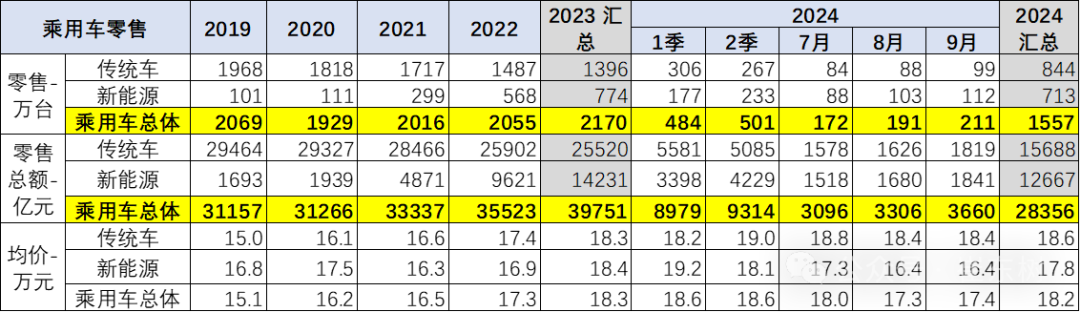

Price changes are mainly affected by structural changes. Car market prices have continued to rise in recent years. In 2019 it was 151,000 yuan, 2020 was 162,000 yuan, the cumulative average this year was 182,000 yuan, and in September it was 174,000 yuan.

The share of entry-level electric vehicles and plug-in hybrid sales increased in September, leading to a drop in average prices. The structural reason for the decline in average prices in September was that the price of hybrids and extenders was higher, but the share declined, causing structural impetus. At the same time, the average sales price of original fuel vehicles also declined, and the higher end of fuel vehicles led to a significant increase in prices.

2. Passenger car market price segment sales structure

According to the retail data of the Passenger Federation, the price segment structure trend in the national urban market continues to rise. Sales of high-end new energy models have increased significantly, and sales of medium- and low-price models have declined.

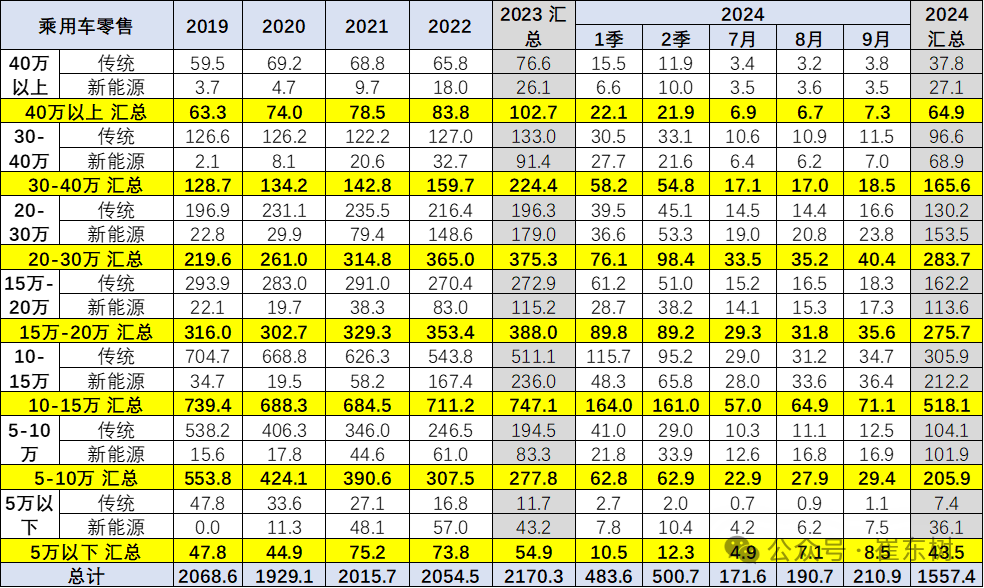

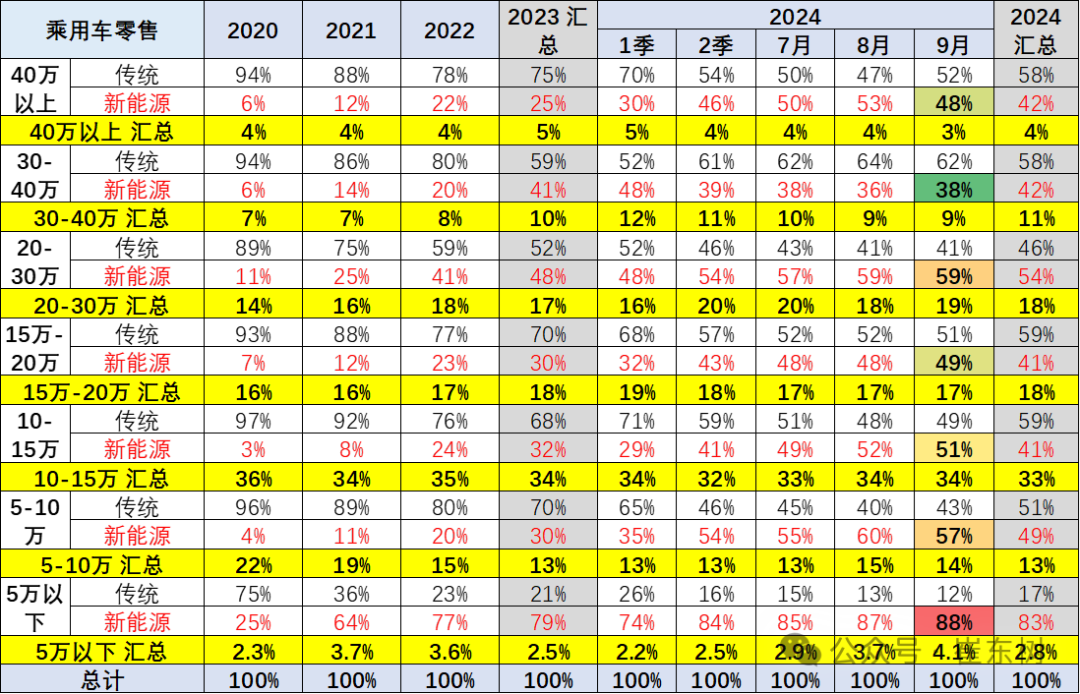

The share of models under 50,000 yuan continued to rise in 2021-2022 compared to 2020, mainly contributing to the sales volume of mini electric vehicles. However, it has continued to decline since 2023, and rebounded after the 3rd quarter of 2024. The sales volume of models under 50,000 yuan in September 2024 accounted for 4.1%, up 1.6 percentage points from 2023. After the decline in sales of 50-150,000 traditional models was offset by the growth of new energy vehicles, the overall downward trend still exists.

The market share of more than 150,000 models continues to rise, growing rapidly. Domestic retail sales of 200,000-300,000 yuan models accounted for 17% in 2023, compared to 19% in September this year. In recent years, the share of all segments of models over 300,000 yuan has continued to rise. The share of retail sales of 300,000-400,000 models was 10% in 2023, and 9% in September. More than 400,000 models accounted for 5% of domestic retail sales in 2023, compared to 3% in September this year. Independent high-end breakthroughs reflect a clear trend in high-end development brought about by the growth of new energy sources for passenger cars, but the downward trend in traditional luxury cars is severe.

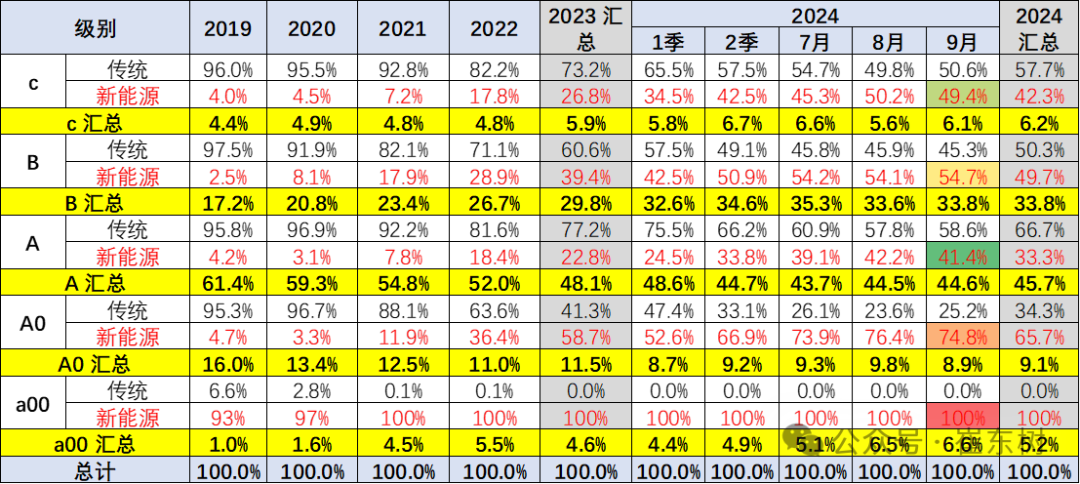

3. Passenger car grade market sales structure

Recently, the highest penetration rate of new energy vehicles was small cars. In September, the penetration rate of mini cars was 100%, A0 class cars surpassed 75%, and A-class new energy increased rapidly.

The new energy penetration rate of B-class cars and C-class cars has increased dramatically, reflecting the obvious advantages of high-end electrification.

The increase in the new energy penetration rate of high-end vehicles mainly reflects the trend of autonomous improvement.

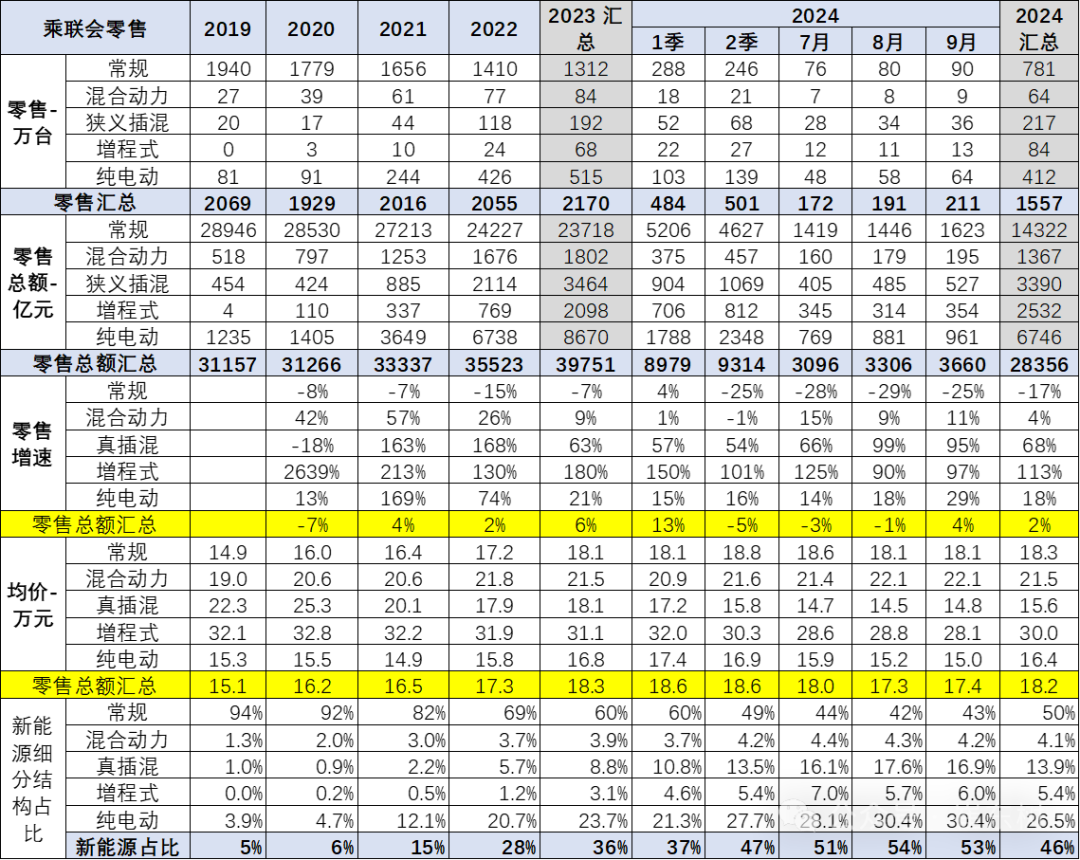

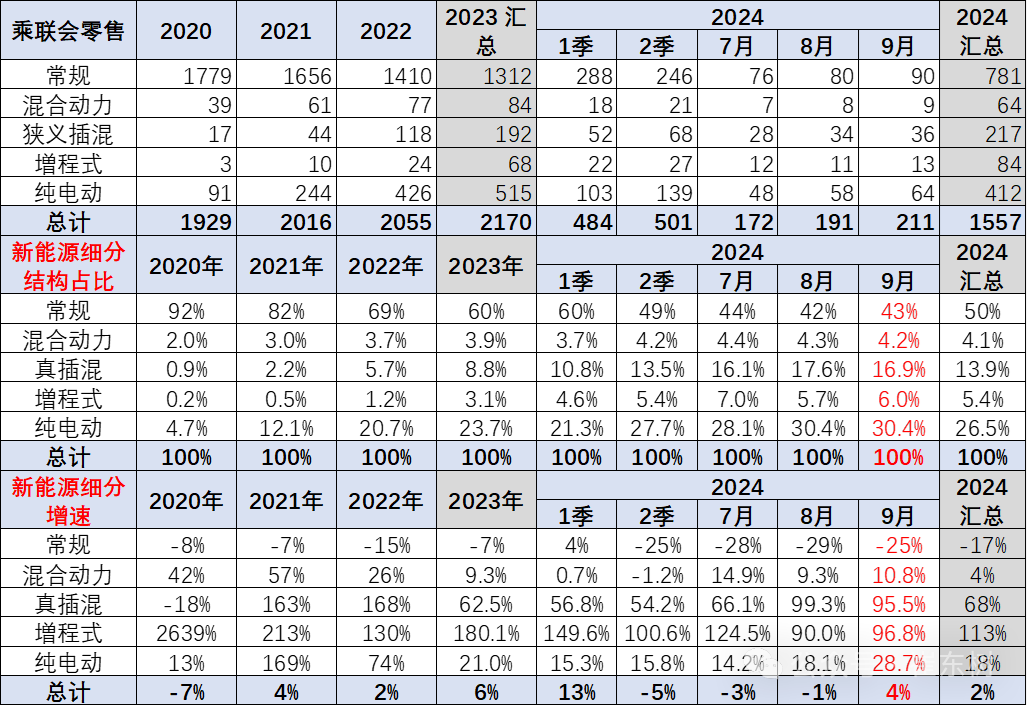

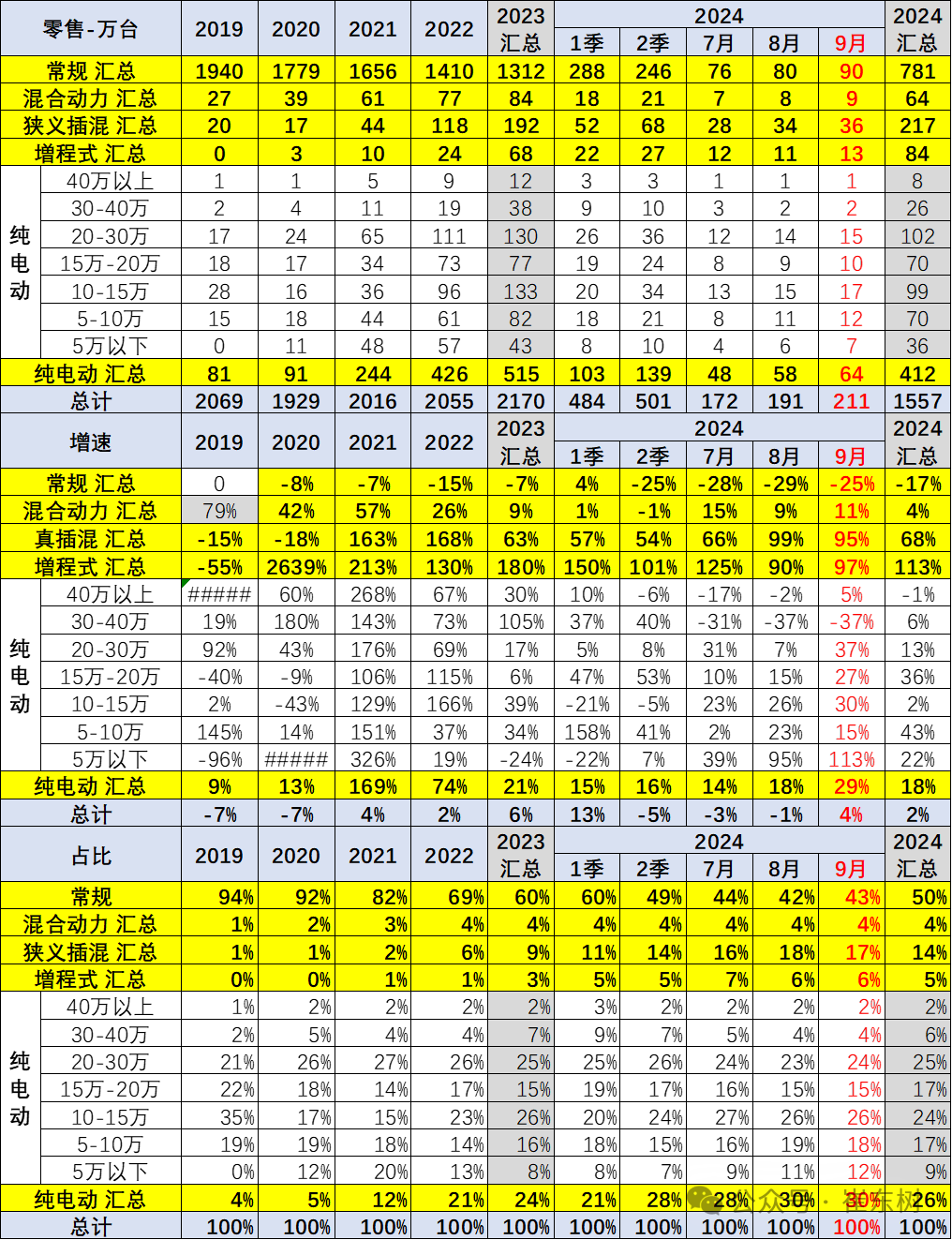

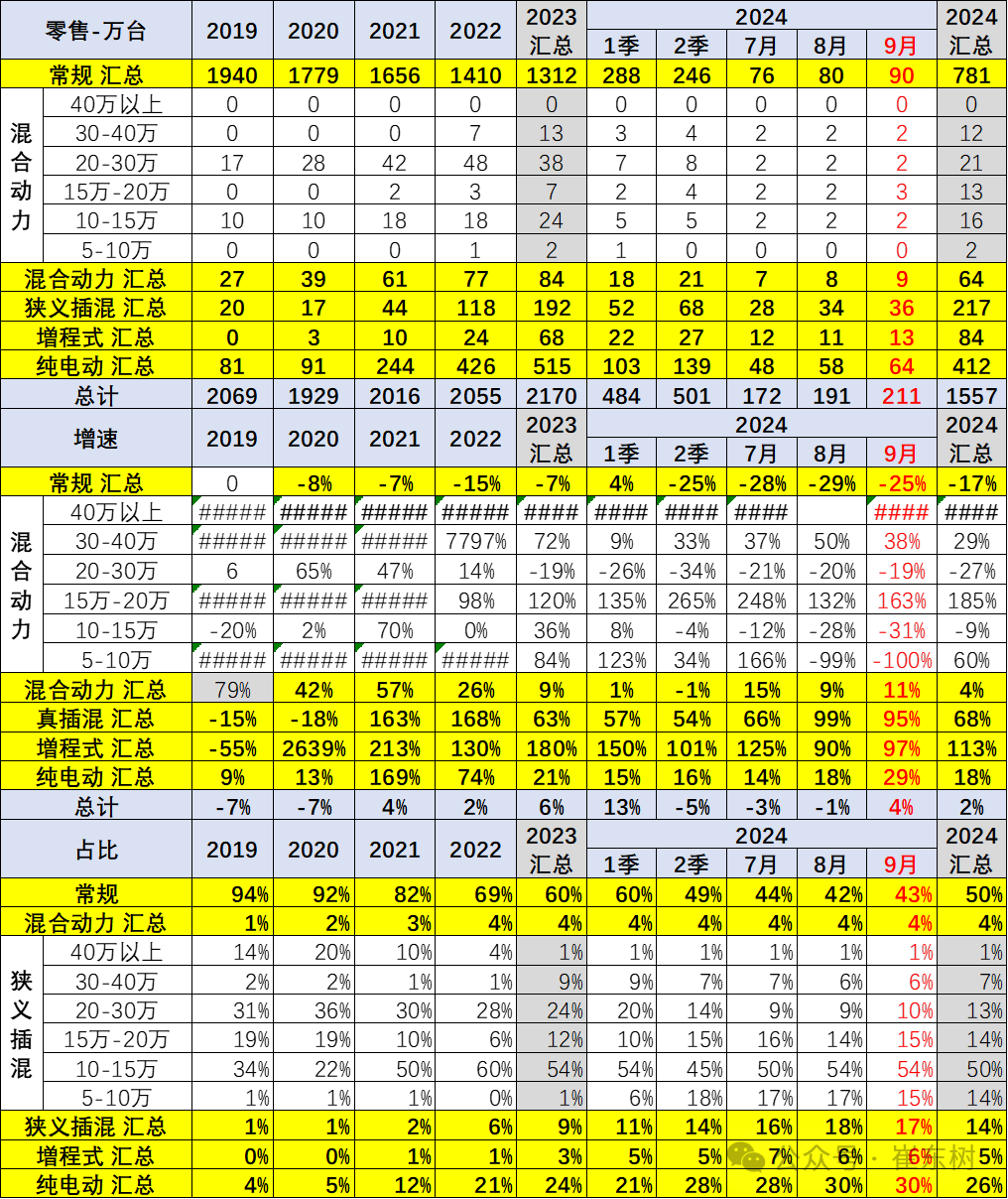

4. New energy vehicle structure for passenger cars

Domestic retail sales of pure electric new energy vehicles have continued to grow at a high rate. The performance of plug-in hybrid has been outstanding in the past three years, and the growth rate has continued to grow slightly. Sales of traditional passenger cars are under continuous downward pressure.

In 2023, the share of new energy vehicles reached a strong proportion of 36%. In September 2024, the penetration rate of new energy vehicles reached 53%, and the contribution of new energy vehicles will continue to rise slightly in the future.

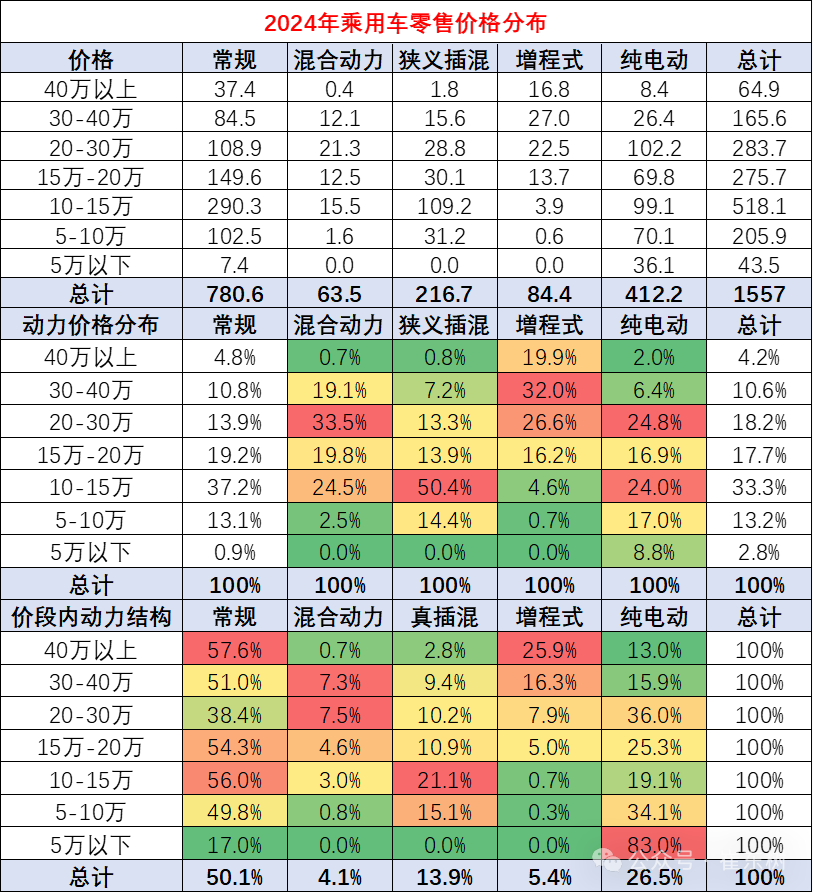

5. Price and sales structure of various types of power in 2024

Currently, the national passenger car market of 50,000 to 150,000 yuan is a characteristic of the core main model market. This is mainly due to the fact that traditional fuel vehicles account for a relatively high share. There is a big difference between traditional cars and new energy vehicles, while the structure in plug-in hybrids is relatively concentrated in the mid-range.

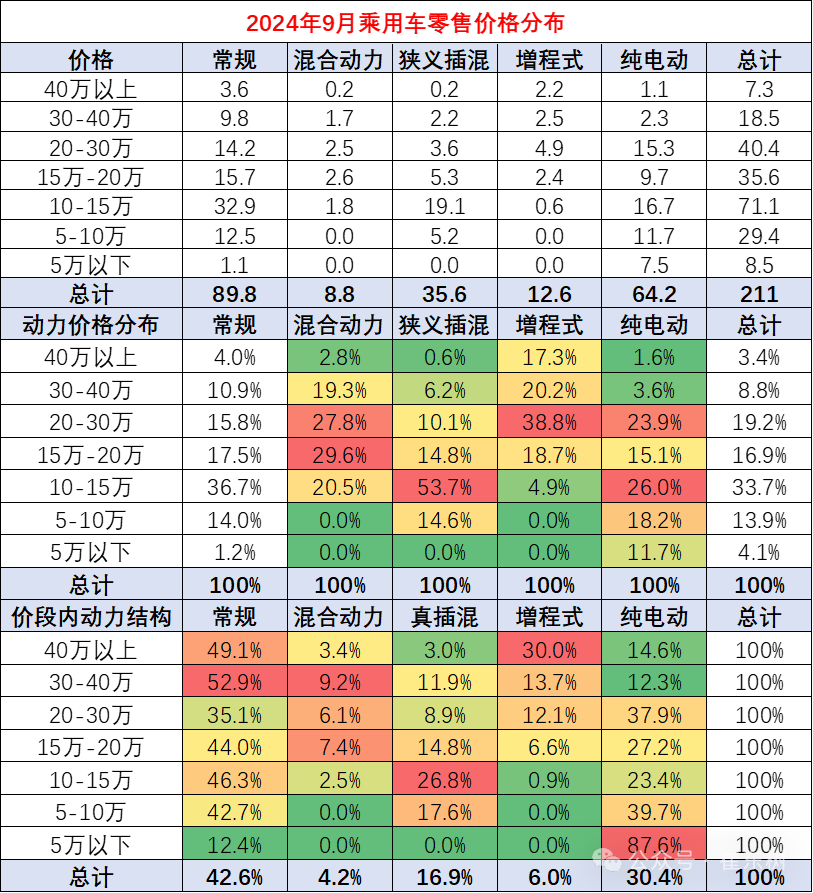

6. Sales structure of internal dynamics in each price segment in September 2024

Within the price segment market, the distribution of power is relatively uneven. Among them, pure electric performance is the strongest in the market below 50,000 yuan, while extended-range electric vehicles have the strongest performance distribution in the high-end market, while hybrids are relatively strong at 200,000 to 300,000 yuan.

Traditional fuel vehicles have a relatively strong performance of 100,000 to 150,000 yuan, forming the characteristics of differentiated distribution. In particular, the distribution of hybrid power is relatively narrow. Products belonging to the middle to high price range are mainly, while plug-in hybrids are the main mainstream models. The low-end market contracted more severely at the beginning of the year. This is also because the impact of weak consumption had a greater impact on the low-end.

7. Conventional fuel passenger vehicle structure

The high-end product structure of traditional fuel vehicles is obvious, mainly due to the high growth of models over 150,000 yuan. This is a direct reflection of consumption upgrades. Recently, the rate of decline in fuel vehicles below 100,000 yuan has slowed down. Under the high growth of pure electric vehicles, fuel vehicles are characterized by a sharp decline.

8. Changes in the product structure of pure electric vehicles - high-end growth is greater

As the cost of pure electric vehicles falls and products increase, electric vehicles under 50,000 are falling faster, and electric vehicles of 150,000 to 300,000 yuan have strong performance. Among these, Tesla (TSLA.US) is still ranked above 200,000, preventing structural fluctuations too much.

With the promotion of the end-of-life renewal policy, new energy sources below 100,000 have increased significantly recently. The share of electric vehicles worth 100,000 to 150,000 yuan has declined. Some of these electric vehicles are the main players in online rental contracts, etc., and the A-class electric vehicle market trend has not been strong in the past two years. As lithium carbonate prices fell, the micro electric vehicle market recovered.

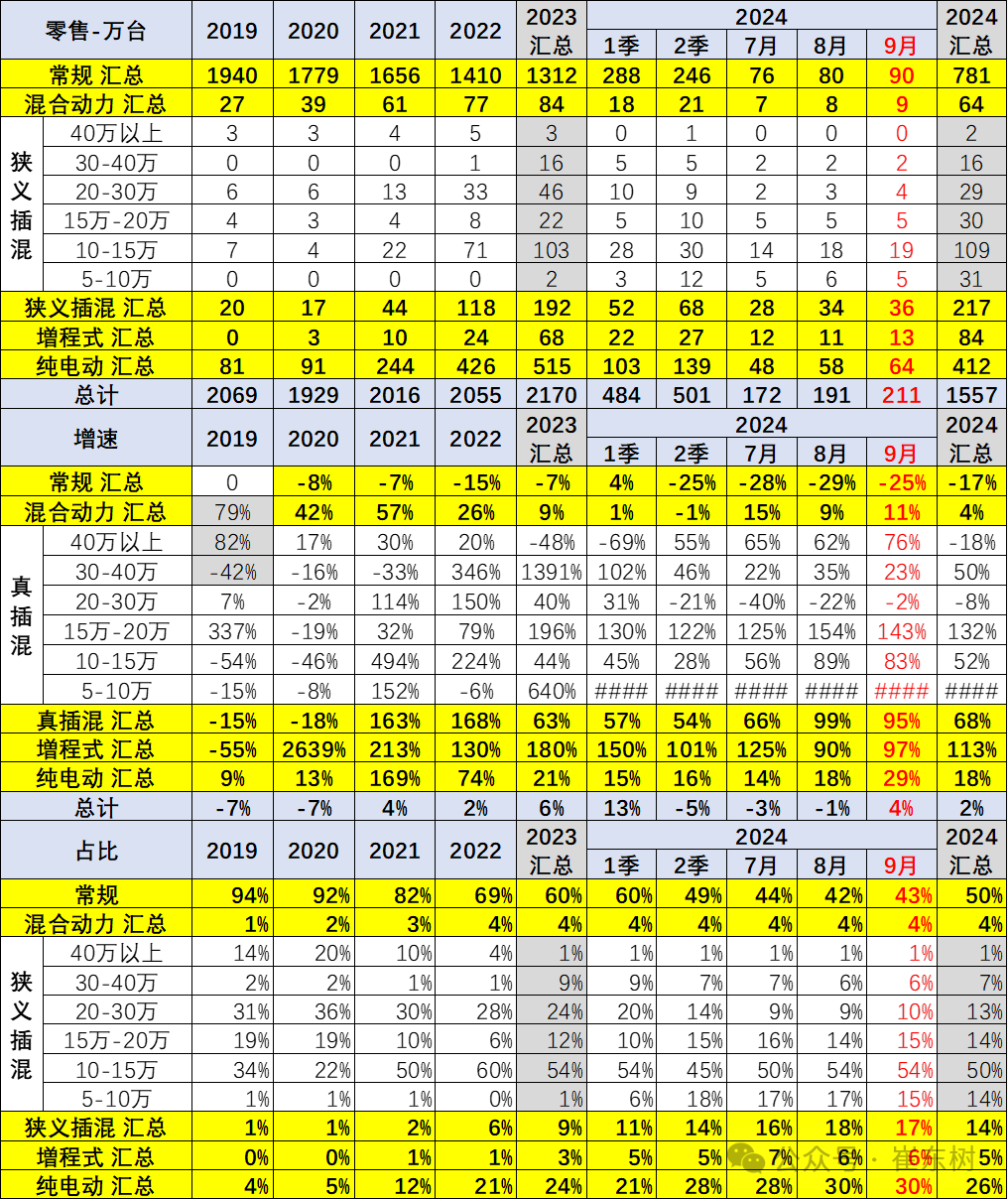

9. Changes in plug-in hybrid product structure - - significant increase in mid-range and high-end

The increase in plug-in hybrid models is mainly in the low price range. After autonomous plug-in hybrid technology matures, they have gained a large share in the medium to low price market. In 2024, the 100,000 yuan hybrid exploded growth, driving the strength of the plug-in mix.

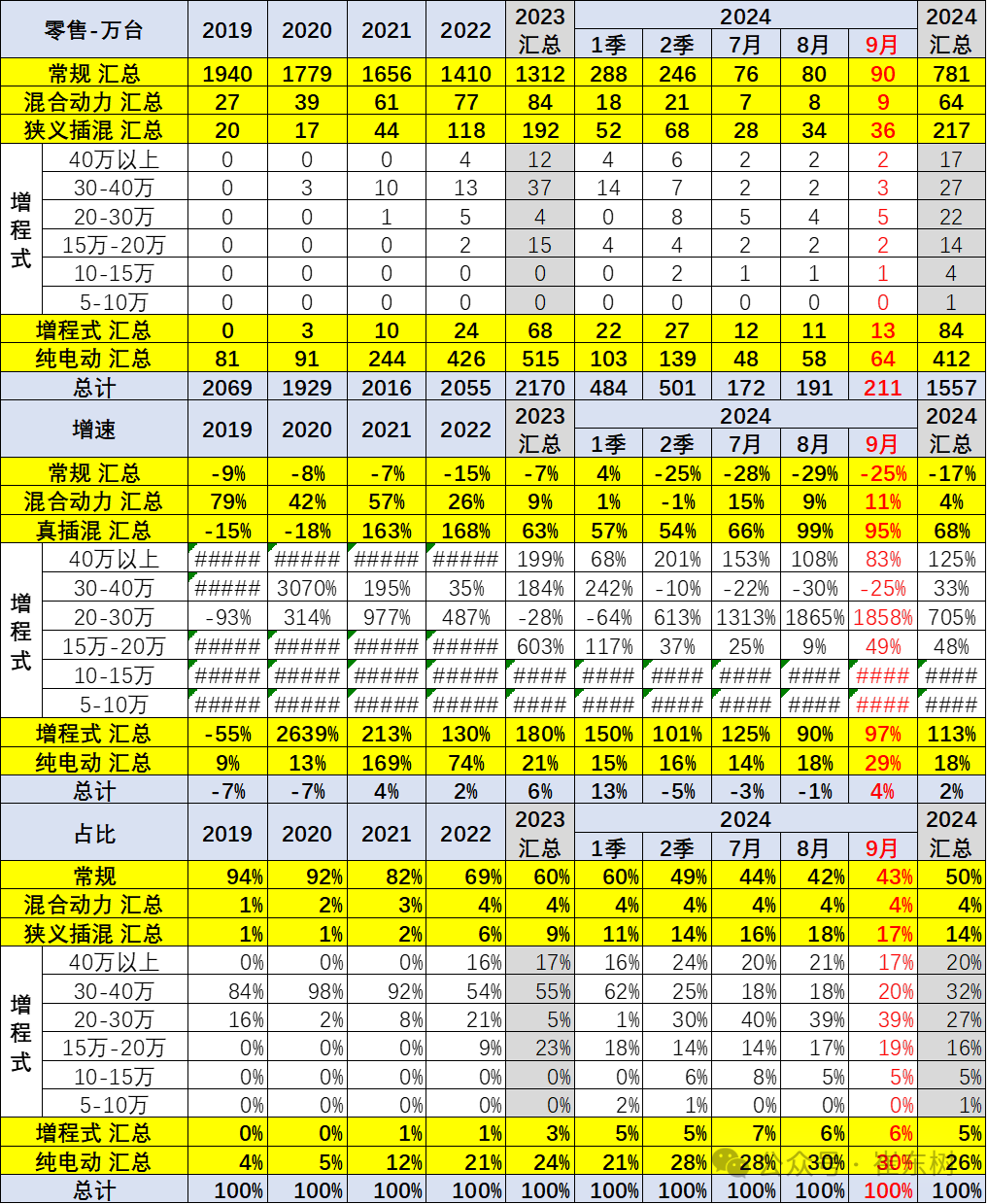

10. Extended range product structure changes - high-end performance is very strong

As a branch of pure electric power, the extended range was put into the hybrid. The performance continued to strengthen in previous years, and both high-end and 150,000 yuan products were strong.

Recently, growth in expansion programs has clearly slowed, and the share of high-end ones has declined sharply.

11. Ordinary hybrid products - changes in high-end share

The share of the hybrid car market also continues to rise. The supply improvement in 2024 led to a gradual increase in share. Policy-driven market demand is shifting to mixed markets. Joint venture hybrid market performance is average.

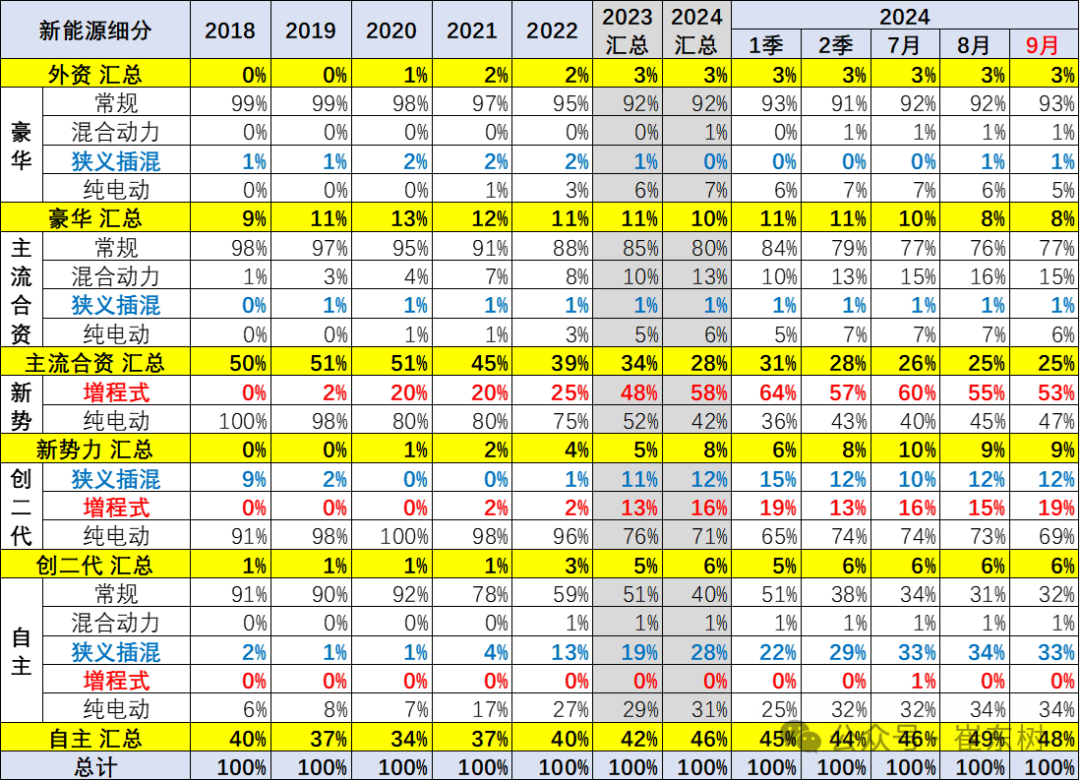

12. Changes in product shares of various car companies

Independent brands performed very well in 2024. New energy sources were fully effective, and pure electric and hybrid performance in the narrow sense were all very good. Overall, the dominant areas of new energy are prominent in high-end oil and electricity hybrids brought about by independent innovative technology. The structure of the new forces fluctuates greatly, and the growth performance is relatively good. The pure electric market gradually strengthened, and jointly diverted the fuel vehicle market. In September, autonomous fuel vehicles accounted for only 32% of the autonomous fuel vehicles.