Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalSEHK Growth Companies With High Insider Ownership October 2024

As global markets experience varied economic shifts, the Hong Kong market has been navigating its own challenges, with the Hang Seng Index recently seeing significant declines amid concerns over China's economic stimulus measures. In this environment, growth companies with high insider ownership can offer unique insights into potential resilience and alignment of interests between company leaders and shareholders.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

| Name | Insider Ownership | Earnings Growth |

| Laopu Gold (SEHK:6181) | 36.4% | 33.2% |

| Akeso (SEHK:9926) | 20.5% | 53% |

| Fenbi (SEHK:2469) | 33.1% | 22.4% |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.8% | 69.8% |

| Pacific Textiles Holdings (SEHK:1382) | 11.2% | 37.7% |

| DPC Dash (SEHK:1405) | 38.1% | 104.2% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 13.9% | 109.2% |

| Beijing Airdoc Technology (SEHK:2251) | 29.4% | 93.4% |

| Zhejiang Leapmotor Technology (SEHK:9863) | 15% | 69.7% |

| MicroTech Medical (Hangzhou) (SEHK:2235) | 25.8% | 105% |

Let's dive into some prime choices out of the screener.

Shanghai INT Medical Instruments (SEHK:1501)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shanghai INT Medical Instruments Co., Ltd. operates in the medical instruments sector and has a market cap of HK$5.51 billion.

Operations: The company generates revenue from its Cardiovascular Interventional Business, totaling CN¥718.71 million.

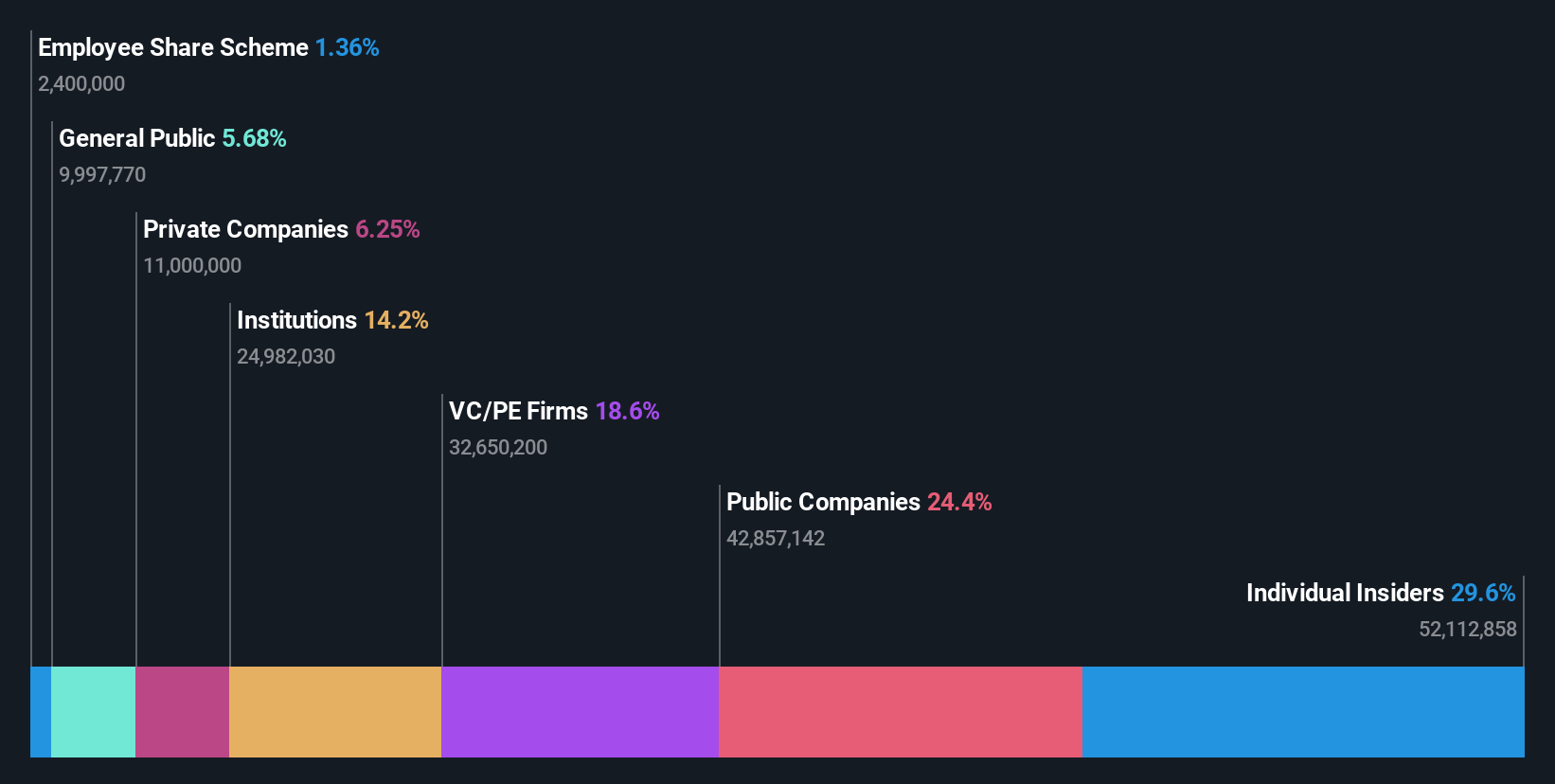

Insider Ownership: 29.6%

Earnings Growth Forecast: 27.2% p.a.

Shanghai INT Medical Instruments is trading at 44.2% below its estimated fair value, indicating potential undervaluation. The company's earnings and revenue are forecast to grow significantly at 27.2% and 28.7% per year respectively, outpacing the Hong Kong market averages of 12.1% and 7.3%. Despite recent shareholder dilution, net income increased from CNY 80.5 million to CNY 100.54 million in the latest half-year results, showcasing robust financial performance amidst market challenges.

- Click to explore a detailed breakdown of our findings in Shanghai INT Medical Instruments' earnings growth report.

- Upon reviewing our latest valuation report, Shanghai INT Medical Instruments' share price might be too optimistic.

Beauty Farm Medical and Health Industry (SEHK:2373)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Beauty Farm Medical and Health Industry Inc. operates in the health and beauty sector, focusing on medical and wellness services, with a market cap of HK$4.05 billion.

Operations: The company's revenue is derived from Aesthetic Medical Services (CN¥851.81 million), Subhealth Medical Services (CN¥125.69 million), Beauty and Wellness Services through Direct Stores (CN¥1.14 billion), and Franchisee and Others (CN¥131.48 million).

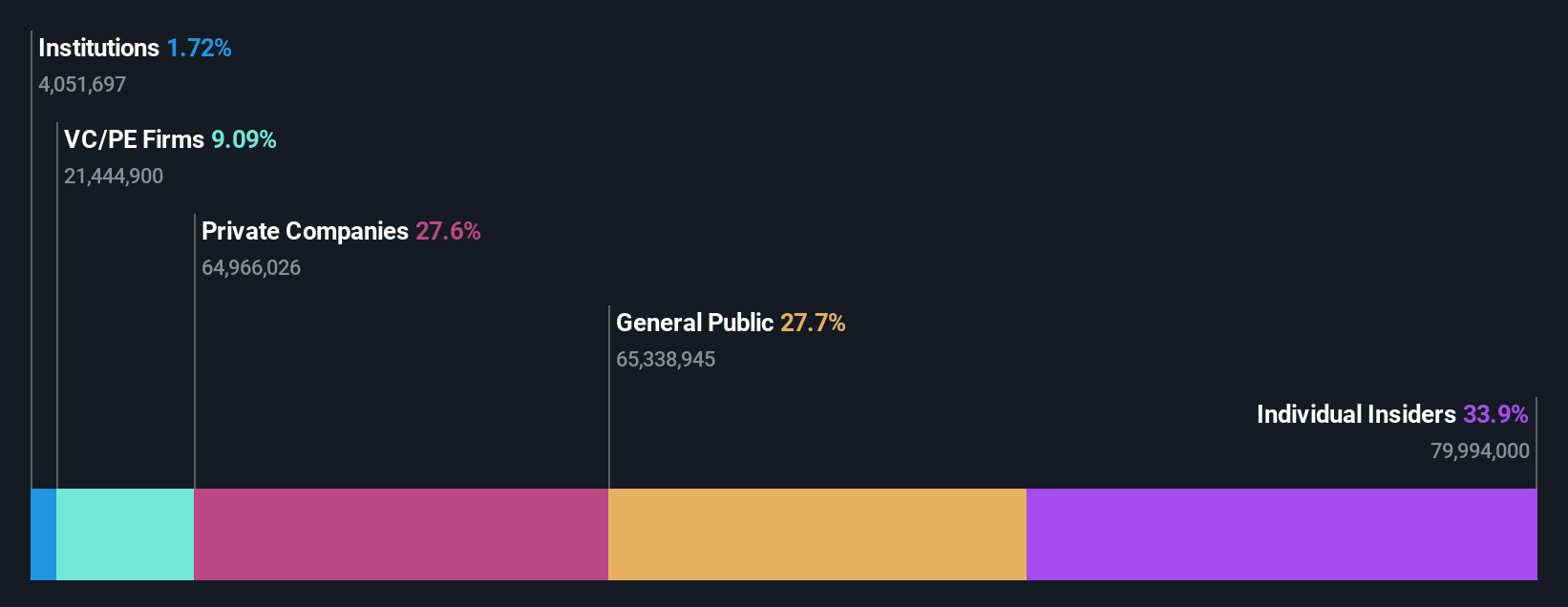

Insider Ownership: 33.9%

Earnings Growth Forecast: 20.2% p.a.

Beauty Farm Medical and Health Industry is trading at 64.1% below its estimated fair value, suggesting potential undervaluation. Its earnings are forecast to grow significantly at 20.2% annually, surpassing the Hong Kong market average of 12.1%. Recent half-year results show sales increased to CNY 1.14 billion, with net income rising slightly to CNY 115.42 million. A recent board change introduced Mr. Hu Tenghe as a non-executive director, bringing extensive capital markets experience.

- Delve into the full analysis future growth report here for a deeper understanding of Beauty Farm Medical and Health Industry.

- Our valuation report here indicates Beauty Farm Medical and Health Industry may be overvalued.

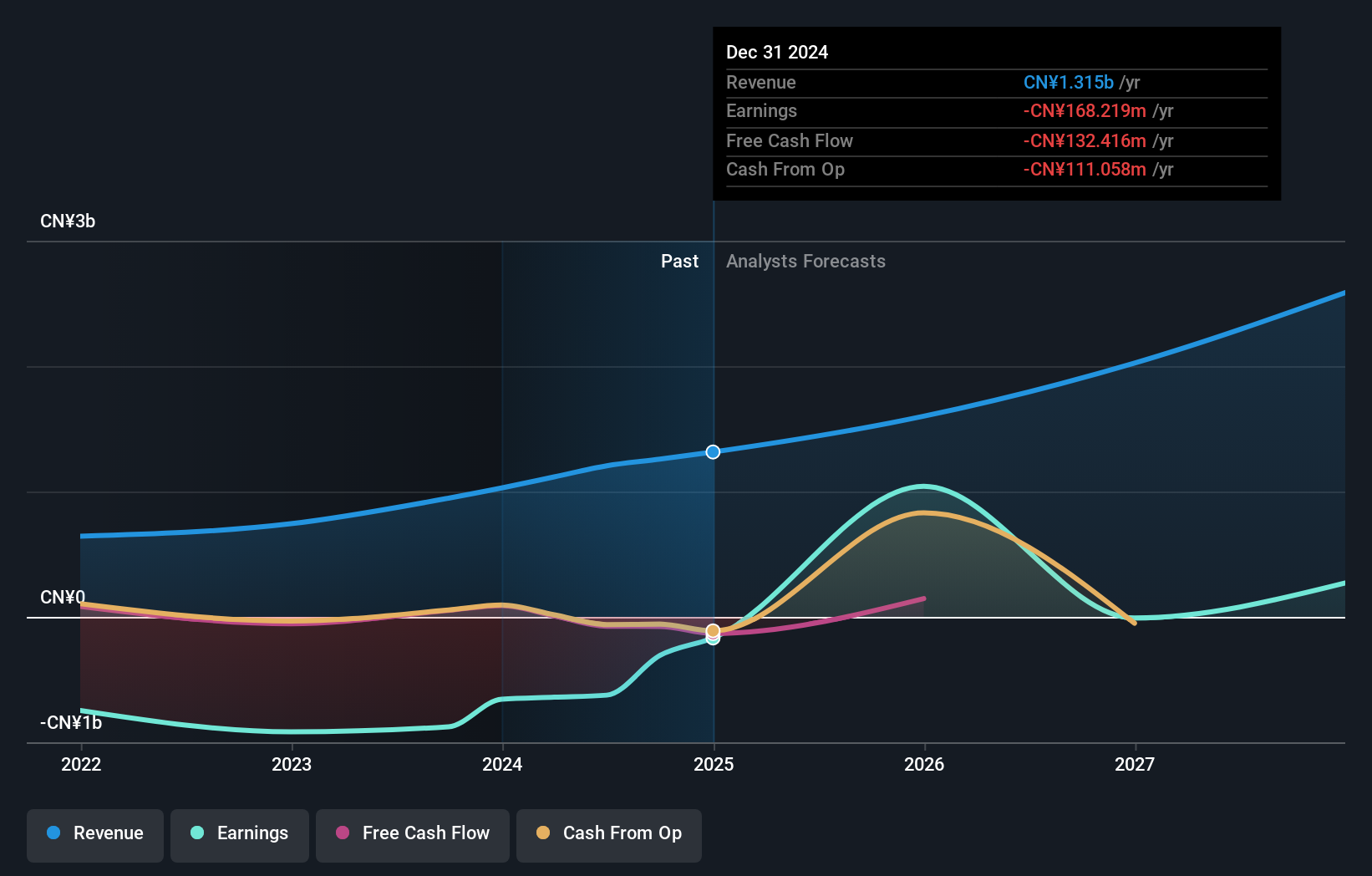

Lianlian DigiTech (SEHK:2598)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Lianlian DigiTech Co., Ltd. offers digital payment and value-added services to small and midsized merchants and enterprises in China, with a market cap of approximately HK$10.59 billion.

Operations: The company's revenue is derived from three main segments: Global Payment (CN¥722.95 million), Domestic Payment (CN¥309.92 million), and Value-Added Services (CN¥153.01 million).

Insider Ownership: 19.7%

Earnings Growth Forecast: 95.7% p.a.

Lianlian DigiTech's revenue is forecast to grow at 22.3% annually, outpacing the Hong Kong market's 7.3%. Earnings are expected to rise significantly by 95.65% per year, with profitability anticipated in three years. Recent results showed a sales increase to CNY 617.39 million, though net loss narrowed slightly to CNY 351.29 million compared to last year. The company's Return on Equity is projected at a modest 14.3% in three years' time, indicating potential challenges ahead despite growth prospects.

- Dive into the specifics of Lianlian DigiTech here with our thorough growth forecast report.

- Our expertly prepared valuation report Lianlian DigiTech implies its share price may be too high.

Seize The Opportunity

- Dive into all 47 of the Fast Growing SEHK Companies With High Insider Ownership we have identified here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com