Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalASX Stocks Estimated To Be Below Intrinsic Value In October 2024

The Australian market has experienced a flat performance over the last week, yet it boasts an impressive 17% increase over the past year, with earnings projected to grow by 12% annually. In such an environment, identifying stocks that are estimated to be trading below their intrinsic value can offer potential opportunities for investors looking to capitalize on future growth prospects.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Mader Group (ASX:MAD) | A$5.60 | A$10.42 | 46.3% |

| MLG Oz (ASX:MLG) | A$0.63 | A$1.15 | 45.3% |

| Charter Hall Group (ASX:CHC) | A$15.79 | A$31.43 | 49.8% |

| Ingenia Communities Group (ASX:INA) | A$4.93 | A$9.41 | 47.6% |

| Treasury Wine Estates (ASX:TWE) | A$12.29 | A$24.19 | 49.2% |

| Millennium Services Group (ASX:MIL) | A$1.145 | A$2.24 | 48.9% |

| IDP Education (ASX:IEL) | A$14.79 | A$27.65 | 46.5% |

| Ai-Media Technologies (ASX:AIM) | A$0.76 | A$1.42 | 46.3% |

| Superloop (ASX:SLC) | A$1.715 | A$3.31 | 48.2% |

| Mineral Resources (ASX:MIN) | A$50.67 | A$95.49 | 46.9% |

We're going to check out a few of the best picks from our screener tool.

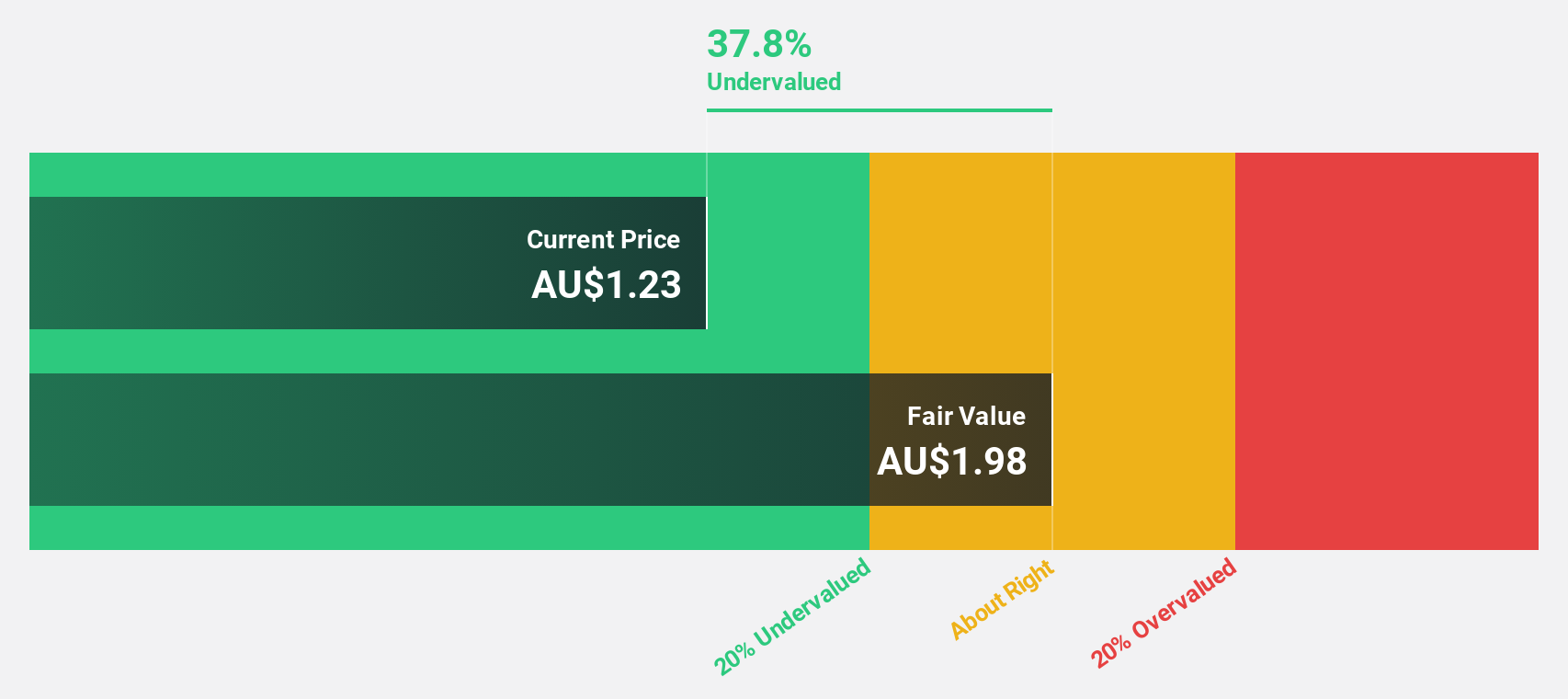

Infomedia (ASX:IFM)

Overview: Infomedia Ltd is a technology company that develops and supplies electronic parts catalogues, service quoting software, and e-commerce solutions for the automotive industry worldwide, with a market cap of A$579.00 million.

Operations: The company's revenue segment includes Publishing - Periodicals, generating A$140.83 million.

Estimated Discount To Fair Value: 35.9%

Infomedia is trading at A$1.55, significantly below its estimated fair value of A$2.41, indicating it may be undervalued based on cash flows. Despite large one-off items impacting financial results, earnings grew by 32.4% last year and are expected to grow significantly over the next three years at 22% annually, outpacing the Australian market's growth rate of 12.2%. However, its dividend yield of 2.72% is not well covered by earnings.

- In light of our recent growth report, it seems possible that Infomedia's financial performance will exceed current levels.

- Unlock comprehensive insights into our analysis of Infomedia stock in this financial health report.

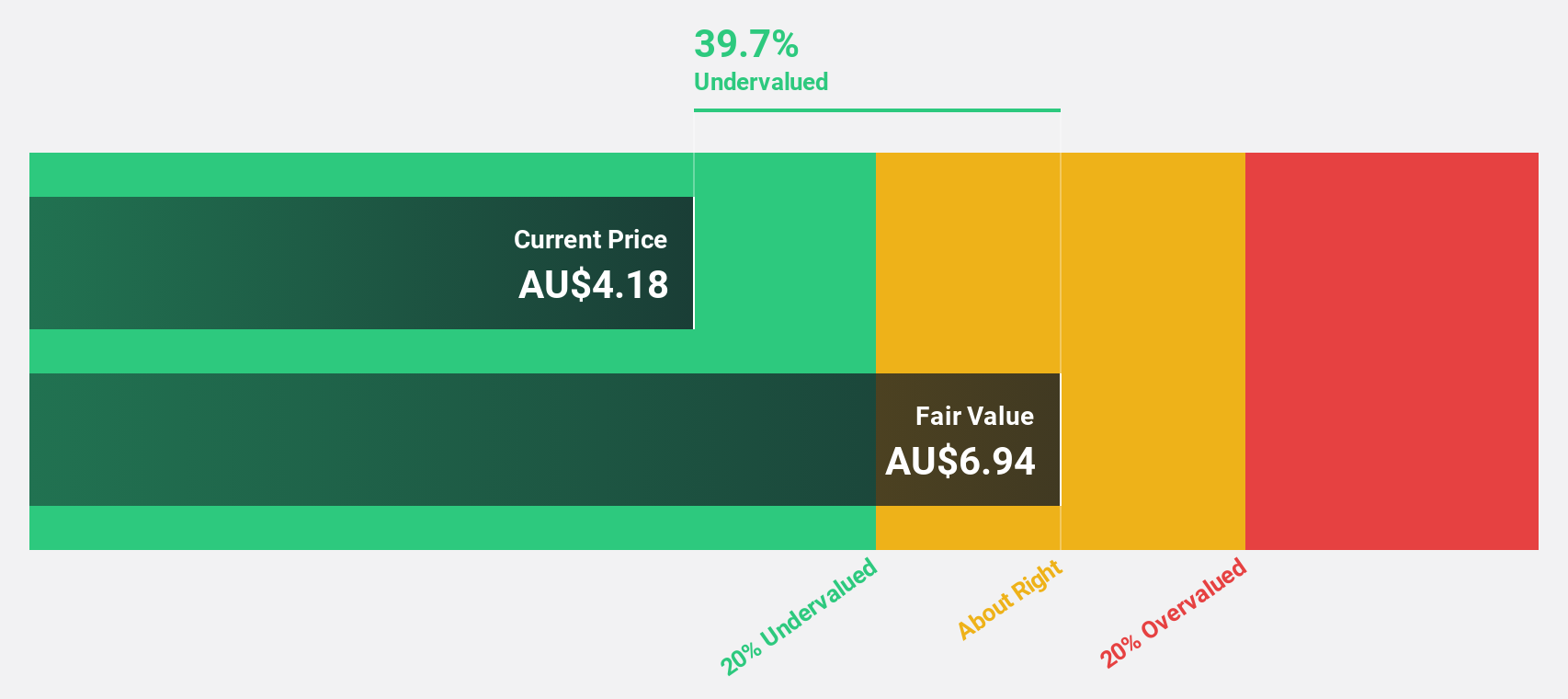

Nanosonics (ASX:NAN)

Overview: Nanosonics Limited is a global infection prevention company with a market cap of A$1.12 billion.

Operations: The company's revenue is derived from its Healthcare Equipment segment, which generated A$170.01 million.

Estimated Discount To Fair Value: 27.5%

Nanosonics is trading at A$3.69, below its estimated fair value of A$5.09, suggesting potential undervaluation based on cash flows. Despite a recent drop from the S&P/ASX 200 Index and declining profit margins from 12% to 7.6%, earnings are forecasted to grow significantly at 23.6% annually over the next three years, surpassing the Australian market's growth rate of 12.2%. However, revenue growth remains modest at an expected annual rate of 8.7%.

- The growth report we've compiled suggests that Nanosonics' future prospects could be on the up.

- Click here and access our complete balance sheet health report to understand the dynamics of Nanosonics.

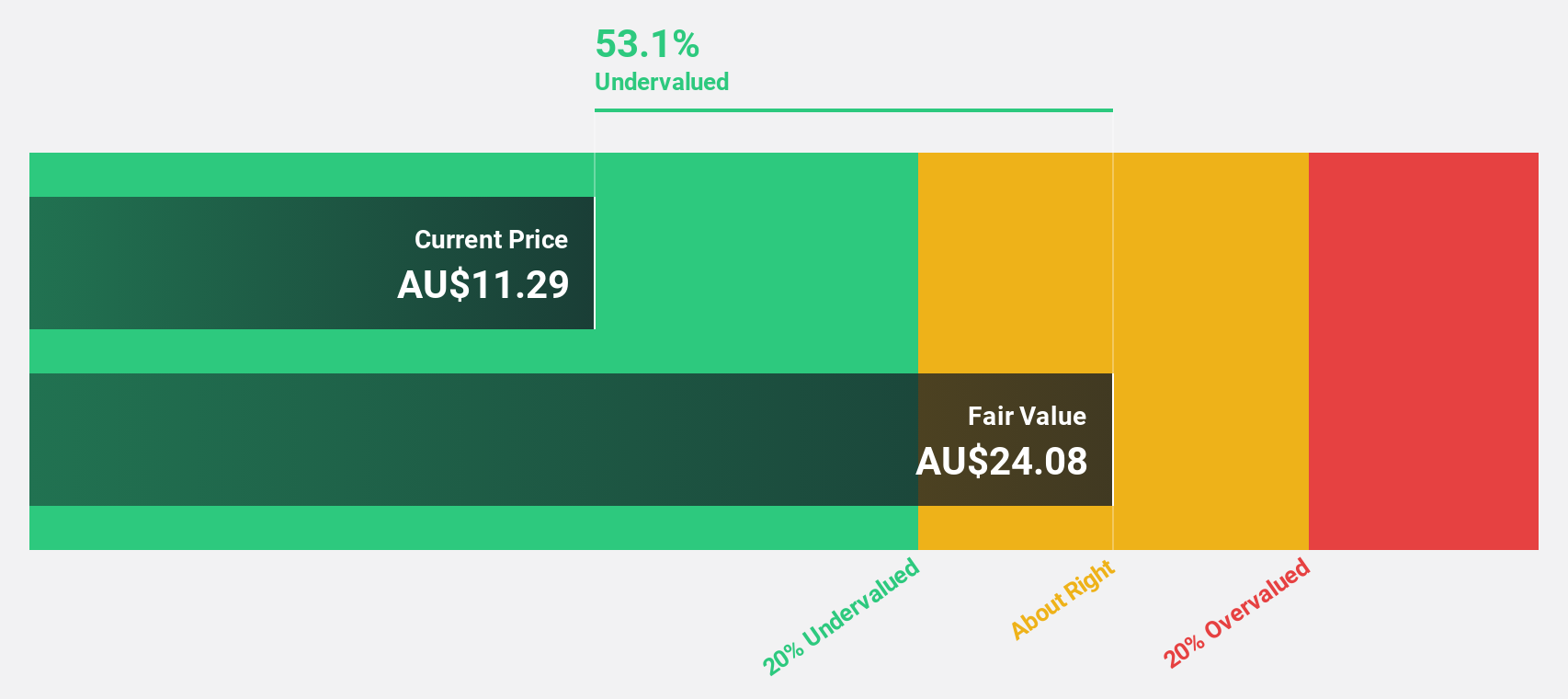

Sandfire Resources (ASX:SFR)

Overview: Sandfire Resources Limited is a mining company involved in the exploration, evaluation, and development of mineral tenements and projects, with a market cap of A$5.10 billion.

Operations: The company's revenue is primarily derived from the MATSA Copper Operations at $565.68 million, the Motheo Copper Project at $346.47 million, and the Degrussa Copper Operations at $29.40 million.

Estimated Discount To Fair Value: 25.5%

Sandfire Resources is trading at A$11.14, below its estimated fair value of A$14.96, indicating it is undervalued based on cash flows. Despite reporting a net loss of US$17.35 million for the fiscal year ending June 2024, the company has been added to the S&P/ASX 100 Index and expects significant annual earnings growth of 40.24%. Revenue is forecasted to grow faster than the Australian market at 8.8% annually over three years.

- Our earnings growth report unveils the potential for significant increases in Sandfire Resources' future results.

- Take a closer look at Sandfire Resources' balance sheet health here in our report.

Next Steps

- Unlock more gems! Our Undervalued ASX Stocks Based On Cash Flows screener has unearthed 44 more companies for you to explore.Click here to unveil our expertly curated list of 47 Undervalued ASX Stocks Based On Cash Flows.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com