Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street Journal3 Growth Companies With High Insider Ownership On Euronext Paris Featuring 46% Revenue Growth

As the French CAC 40 Index experiences modest gains amid hopes for accelerated European Central Bank interest rate cuts, investors are keenly observing growth companies with significant insider ownership on Euronext Paris. In such a market environment, stocks that combine robust revenue growth with high insider stakes can be particularly appealing, as they often indicate strong confidence from those closest to the company's operations.

Top 10 Growth Companies With High Insider Ownership In France

| Name | Insider Ownership | Earnings Growth |

| Groupe OKwind Société anonyme (ENXTPA:ALOKW) | 20.6% | 36% |

| VusionGroup (ENXTPA:VU) | 13.4% | 81.7% |

| Icape Holding (ENXTPA:ALICA) | 30.2% | 33.9% |

| Arcure (ENXTPA:ALCUR) | 21.4% | 26.6% |

| STIF Société anonyme (ENXTPA:ALSTI) | 16.4% | 22.9% |

| La Française de l'Energie (ENXTPA:FDE) | 19.9% | 31.9% |

| S.M.A.I.O (ENXTPA:ALSMA) | 17.4% | 35.2% |

| Adocia (ENXTPA:ADOC) | 11.7% | 64% |

| Munic (ENXTPA:ALMUN) | 27.1% | 174.1% |

| MedinCell (ENXTPA:MEDCL) | 15.8% | 93.9% |

Let's review some notable picks from our screened stocks.

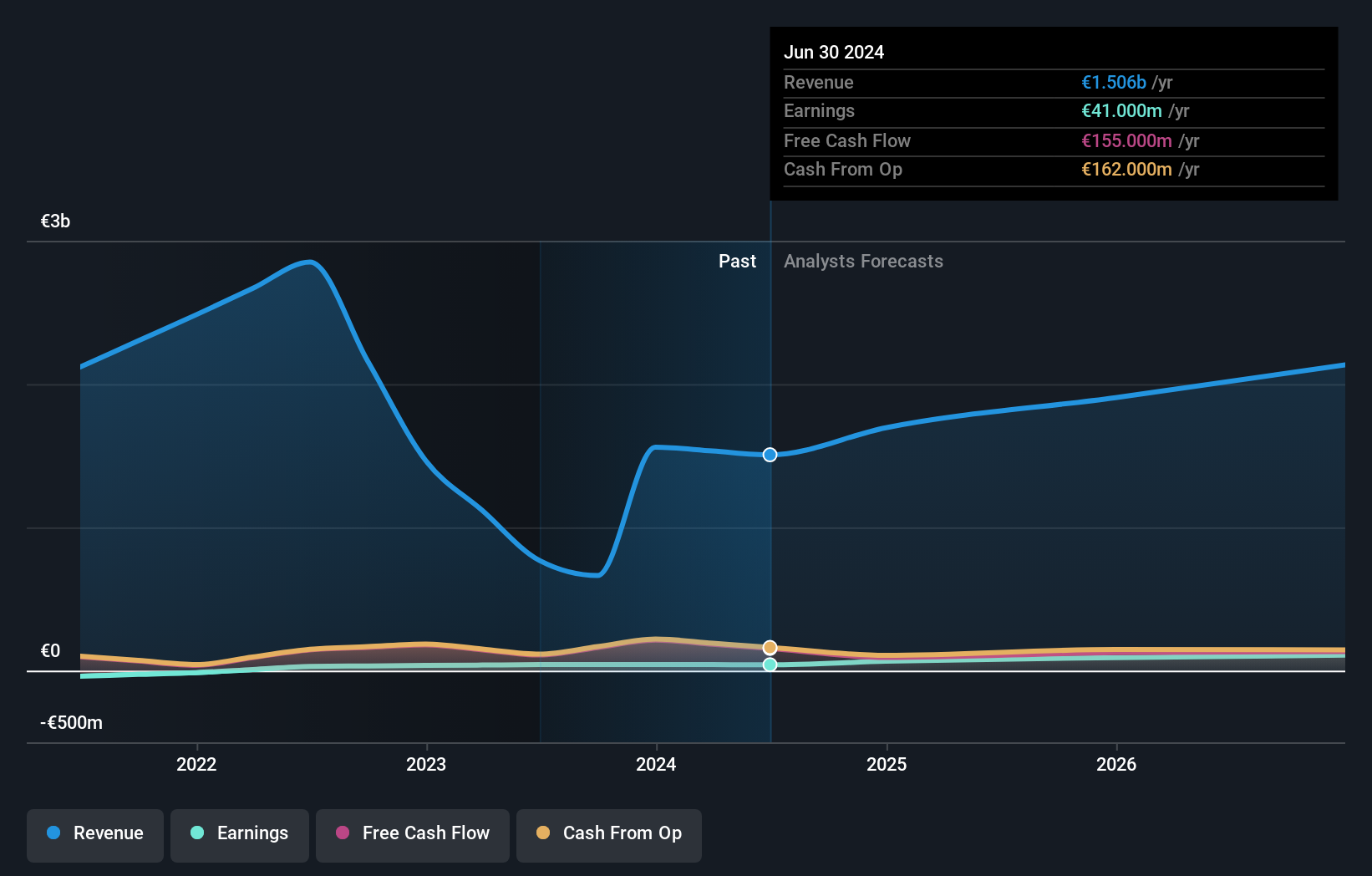

Exclusive Networks (ENXTPA:EXN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Exclusive Networks SA is a global cybersecurity specialist focused on digital infrastructure, with a market cap of €2.14 billion.

Operations: The company generates revenue from various regions, including €480 million from APAC, €4.19 billion from EMEA, and €705 million from the Americas.

Insider Ownership: 13.1%

Revenue Growth Forecast: 13.1% p.a.

Exclusive Networks, a French cybersecurity firm, is experiencing significant insider ownership with 66.7% held by Permira's entity and founder Olivier Breittmayer. The company's earnings are forecast to grow at 33.5% annually, outpacing the French market average of 12.1%. Despite lower profit margins this year, Exclusive Networks is trading below its estimated fair value and is subject to a proposed acquisition by CD&R and Permira for €2.2 billion (US$2.4 billion).

- Click to explore a detailed breakdown of our findings in Exclusive Networks' earnings growth report.

- In light of our recent valuation report, it seems possible that Exclusive Networks is trading beyond its estimated value.

Lectra (ENXTPA:LSS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Lectra SA offers industrial intelligence solutions for the fashion, automotive, and furniture markets across Northern Europe, Southern Europe, the Americas, and the Asia Pacific with a market cap of €1.07 billion.

Operations: The company's revenue segments include €172.65 million from the Americas and €118.54 million from the Asia-Pacific region.

Insider Ownership: 19.6%

Revenue Growth Forecast: 10.4% p.a.

Lectra, a French technology firm, is trading significantly below its estimated fair value and boasts strong growth prospects. Despite being dropped from the S&P Global BMI Index recently, Lectra's earnings are forecast to grow at 29.3% annually over the next three years, outpacing the French market average. Revenue growth is expected to surpass market rates at 10.4% per year. However, recent earnings showed a decline in net income compared to last year despite increased sales.

- Dive into the specifics of Lectra here with our thorough growth forecast report.

- In light of our recent valuation report, it seems possible that Lectra is trading behind its estimated value.

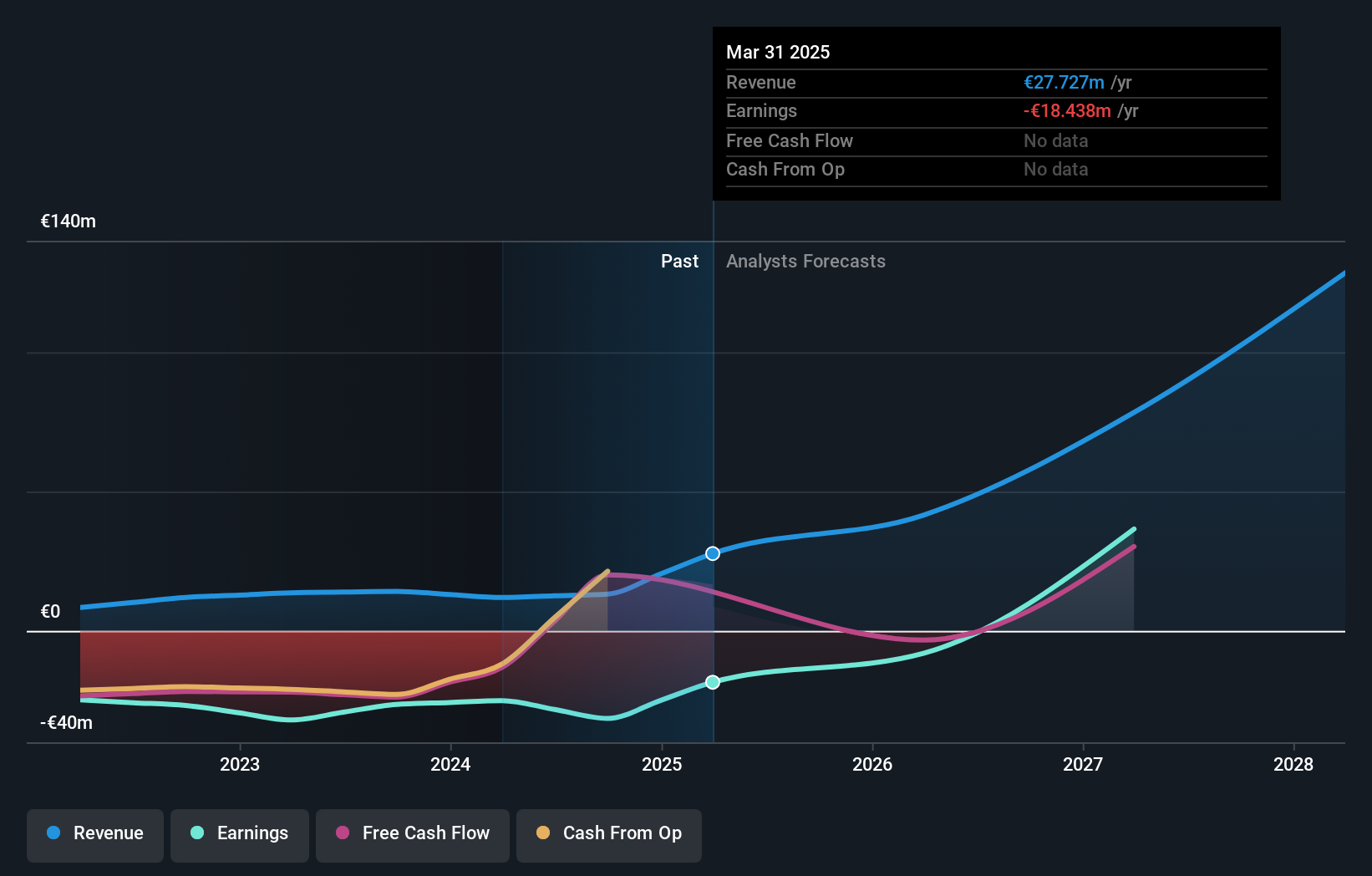

MedinCell (ENXTPA:MEDCL)

Simply Wall St Growth Rating: ★★★★★☆

Overview: MedinCell S.A. is a pharmaceutical company in France that develops long-acting injectables across various therapeutic areas, with a market cap of €442.13 million.

Operations: The company's revenue primarily comes from its pharmaceuticals segment, totaling €11.95 million.

Insider Ownership: 15.8%

Revenue Growth Forecast: 46.2% p.a.

MedinCell, a French pharmaceutical company, is trading significantly below its estimated fair value and demonstrates robust growth potential. With revenue expected to grow at 46.2% annually, it outpaces the French market average. The recent strategic partnership with AbbVie for co-developing therapeutic products highlights its innovative BEPO® technology's commercial appeal. Despite negative shareholders' equity, MedinCell's inclusion in the S&P Global BMI Index and anticipated profitability within three years underscore its promising trajectory in the industry.

- Delve into the full analysis future growth report here for a deeper understanding of MedinCell.

- Insights from our recent valuation report point to the potential undervaluation of MedinCell shares in the market.

Turning Ideas Into Actions

- Gain an insight into the universe of 22 Fast Growing Euronext Paris Companies With High Insider Ownership by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com