Understanding Different Types of Bond Duration

Modified Duration: Measuring Price Sensitivity

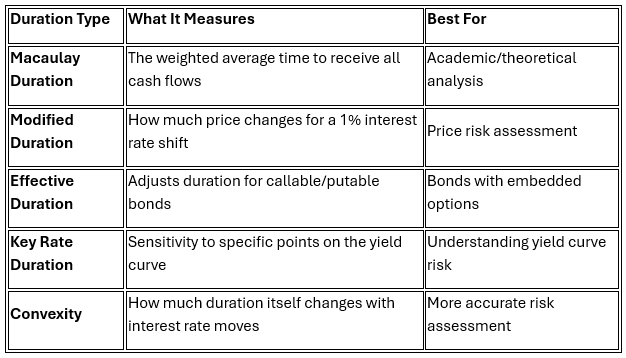

Modified duration is the most commonly used duration measure, especially on trading platforms and brokerage tools. It estimates how much a bond’s price will change for every 1% move in interest rates.

If a bond has a modified duration of 6, a 1% increase in interest rates would result in approximately a 6% decrease in the bond’s price. On the other hand, if rates fall by 1%, the bond’s price would rise by 6%.

This is a linear estimate, meaning it assumes a straight-line relationship between price and yield changes. While it's not perfect in extreme rate environments, modified duration is reliable for small changes and is the go-to measure for evaluating interest rate risk in practice.

Use modified duration to assess price risk across traditional, non-callable bonds.

Macaulay Duration: The Time-Weighted Average

Macaulay duration measures the weighted average time it takes to receive all of a bond’s cash flows, including both coupon payments and the repayment of principal. This metric is expressed in years and serves as a theoretical tool more than a practical investment guide.

For example, a bond with a Macaulay duration of 7 years means that, on average, you’ll receive your money back over a 7-year time frame when accounting for the timing and size of each cash flow.

Effective Duration: The Real-World Adjusted Measure

Not all bonds have fixed cash flows. Bonds with embedded options, such as call or put provisions, can have their payment structures change based on interest rate movements. That’s where effective duration comes in.

Effective duration adjusts the standard duration calculation to account for how a bond’s price might respond if the issuer calls it early or the bondholder exercises a put option. This makes it a better measure for mortgage-backed securities, callable corporate bonds, or any bond with features that could shorten or extend its life.

If a callable bond has a Macaulay duration of 7 years but could realistically be called in 5, its effective duration might be closer to 5 years. This reflects the true price sensitivity of the bond, given the likelihood of early redemption.

Use effective duration when analyzing bonds with embedded options. It offers a more realistic view of interest rate sensitivity.

Key Rate Duration: Pinpointing Yield Curve Changes

Key rate duration breaks the interest rate sensitivity down further by focusing on individual points along the yield curve—such as the 2-year, 5-year, or 10-year Treasury rate. This matters because yield curve movements are often uneven. Short-term and long-term rates can rise or fall independently.

For example, a bond might be more sensitive to changes in the 5-year rate than the 10-year rate, even though both could move in a given market event. Key rate duration helps identify which segment of the curve is driving a bond’s price movements.

This tool is valuable for portfolio managers and analysts trying to hedge or position portfolios around specific curve movements rather than broad rate shifts.

Use key rate duration when evaluating how a bond reacts to non-parallel shifts in the yield curve.

Convexity: One Step Further

While duration estimates the first-order (aka first derivative) price movement, convexity captures the second-order (aka second derivative) effects. It provides a more accurate view of risk when rate changes are large or unpredictable.

Duration assumes a linear relationship between bond prices and interest rates. Convexity accounts for the curve in that relationship.

Convexity measures how much a bond’s duration changes as interest rates change. A bond with high convexity will lose less value when rates rise and gain more value when rates fall compared to a bond with similar duration but lower convexity. This makes convexity a highly desirable trait, especially in volatile markets.

Use convexity to refine your understanding of price sensitivity, especially when managing interest rate risk in volatile environments.

Quick Reference: Duration Types at a Glance

To summarize the distinctions between each measure:

Bottom Line

Duration is essential for understanding bond risk, but not all durations tell the same story.

- For traditional bonds, modified duration gives the best snapshot of how prices may move with interest rates.

- For callable or option-embedded bonds, effective duration provides a more realistic picture.

- When dissecting yield curve exposure, key rate duration shows which parts of the curve matter most.

- And when risk needs to be modeled more precisely, especially in uncertain markets, convexity offers valuable insights beyond duration alone.

While Macaulay duration has its place in academic theory, most investors rely on modified or effective duration when making real-world decisions.

The better you understand each measure, the more accurately you can evaluate bond risk, price sensitivity, and positioning within your broader portfolio. For more fixed-income insights, visit Webull Learn.