Understanding Different Types of Bond Yields

Yield to Maturity (YTM): The Long-Term Return

Yield to maturity (YTM) represents the total return an investor can expect to earn if the bond is held until it matures. It assumes that all coupon payments are reinvested at the same rate and that the bond is not sold before maturity.

What sets YTM apart is that it incorporates:

- The bond’s current market price (which may be above or below face value)

- The annual interest payments (coupons)

- The full repayment of the bond’s face value at maturity

YTM provides a comprehensive, time-weighted measure of return. For example, if you buy a 10-year bond for $950 and it pays $50 per year in interest, your return includes both those coupon payments and the $50 capital gain you earn when the bond matures at its $1,000 face value. In this case, your YTM would be higher than the 5% coupon rate.

YTM is best used by long-term investors who plan to hold the bond to maturity and want a clear view of their total expected return.

Yield to Call (YTC): The Return If the Bond Gets Called Early

Some bonds come with a call feature, meaning the issuer has the option to redeem (pay off) the bond before its maturity date. If interest rates fall after the bond is issued, the issuer may choose to refinance its debt by calling the bond and reissuing new bonds at a lower rate. There are other reasons an issuer might redeem a bond early, and issuers do not have to provide a reason in order to exercise a call feature.

Yield to call (YTC) tells you what your return would be if the bond is called at the earliest allowed date. It’s an important calculation for any bond that carries call provisions, especially if you are interested in a bond that is selling over it’s callable price (usually 100).

For instance, if you buy a 10-year bond that is callable after 5 years, and the issuer exercises that option, your total return will be based on just 5 years of interest—not 10. Your capital gain or loss, along with fewer coupon payments, results in a different yield than YTM.

YTC is relevant when evaluating callable bonds selling above their callable price (usually 100), as it reflects the potential reduction in income due to early redemption.

Yield to Worst (YTW): The Most Conservative View

Yield to worst (YTW) takes both YTM and YTC into account and identifies the lowest possible yield an investor could receive, assuming the bond is held until the worst possible outcome—whether it’s maturity or the earliest call date.

This is not a separate yield calculation so much as a comparison of the others. If a bond’s YTM is 5%, but it could be called in three years with a YTC of 3%, then the YTW is 3%. That’s the worst-case scenario in terms of return.

YTW is often used for risk management. It gives a conservative estimate and sets realistic expectations for investors who don’t want to be caught off guard if the bond is called early or performs below its advertised yield.

Typically, the YTW on bonds priced at a discount will be equal to the YTM. For bonds priced at a premium, the YTW is typically the YTC.

YTW is useful for evaluating downside scenarios and should always be reviewed when investing in callable bonds.

Current Yield: A Simple Snapshot

Current yield offers a quick way to measure the income a bond is generating today, without considering future changes in price or reinvestment assumptions. It’s calculated by dividing the bond’s annual coupon payment by its current market price.

Current Yield = Annual Coupon Payment ÷ Current Market Price

For example, if a bond pays $50 per year in interest and is trading at $1,000, the current yield is 5%. If the same bond is trading at $950, the current yield would be slightly higher. Conversely, if it’s trading at a premium of $1,050, the current yield would be lower.

Current yield is simple, but limited. It does not factor in gains or losses at maturity or whether the bond was purchased at a discount or premium. It also ignores reinvestment assumptions. As such, it’s more of a snapshot than a full picture.

One common mistake retail investors make is comparing the TTM (training 12-month yield) of a bond mutual fund/ETF with the yield quoted on an individual bond. The problem here is that TTM is most similar to the current yield, while they’re typically looking at the YTM or YTW on the individual bond. So, if the bond fund contains a lot of bonds that were bought at a premium, the TTM might look more attractive than what the investor will actually experience in reality.

Current yield is helpful for quickly comparing income potential across bonds, but it should not be relied on alone to evaluate total return.

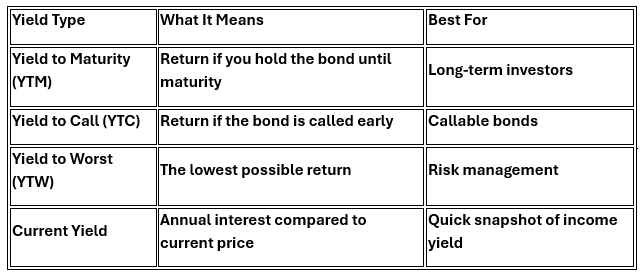

Summary of Key Yield Types

To keep the various yields in context, here’s a breakdown of what each one tells you and when it’s most useful:

Bottom Line

Each yield metric answers a different question:

- If you plan to hold a bond until it matures, YTM gives you the most accurate estimate of your total return.

- If the bond is callable, you need to know the YTC and the YTW—both help assess whether the bond could be redeemed early and how that impacts your returns.

- If you just want a fast look at income potential, current yield gives a simple answer, but one that lacks long-term context.

When evaluating bonds, always consider the yield that best reflects your investing horizon, the bond’s features, and your risk tolerance. Understanding the differences helps you avoid surprises and make better decisions about where to allocate capital.

For more educational content on fixed income and portfolio strategy, explore Webull Learn.