- PREMIUM

- LIVE QUOTES

- INSTITUTIONS

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalCall Backspread (also called Ratio Volatility Call Spread)

Introduction

You have been researching a stock and have formed a bullish opinion on its value, forecasting both a rise in price and high volatility over a given time period. You would also like to limit your risk if your forecast is incorrect and the stock trades within a narrow range instead.

Building on your foundational knowledge of call options as well as the risks and benefits of single-leg options trades (buy call, sell call, buy put, sell put), you recognize that a spread trade achieves some of the objectives you have outlined.

Taking this a step further, by adding an additional leg you can increase your exposure to potential upside gains.

Recall that the combination of a long call and a short call is referred to as a spread trade. When this ratio deviates from 1:1, the strategy is referred to as a ratio spread. The ratio can vary depending on the implied volatility of the option strikes and may include combinations such as 1:2, 2:3, or 1:5. The overall risks and benefits of each individual option component, or leg, offset one another to a degree in order to create the desired position and range of possible outcomes.

What is a 1x2 Ratio Volatility Call Spread?

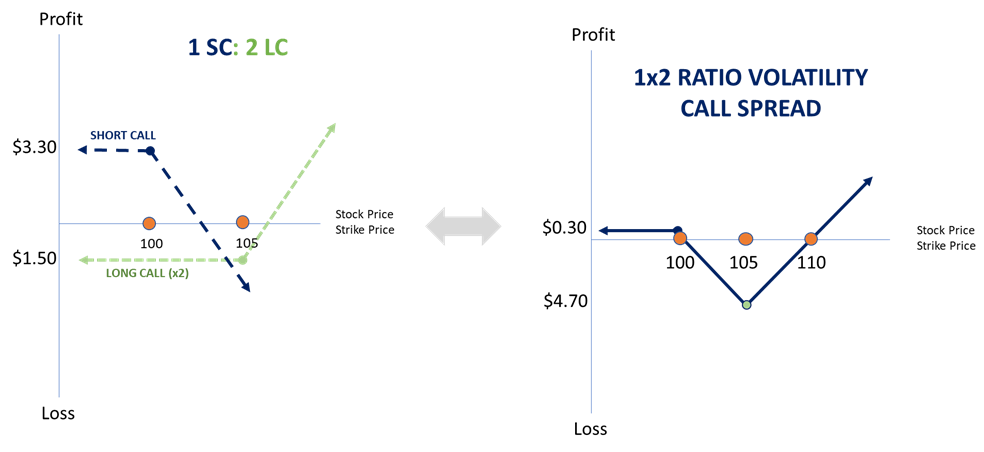

A 1x2 ratio volatility call spread consists of one short call with a lower strike price and two long calls with a higher strike price:

- Short 1 XYZ 100 call

- Long 2 XYZ 105 calls

This strategy can be established for either a net credit or for a net debit, depending on the time to expiration, the percentage distance between the strike prices, and the level of volatility.

Profit potential is unlimited as the stock price moves above the long call strike. Risk exposure is limited. It’s important to highlight that the maximum risk exposure is in fact higher than the initial cost to establish the position.

Additional Considerations

A 1x2 ratio volatility call spread is equivalent to combining a bear call spread and a long call (with the same strike as the long call in the bear call spread).

The net premium received from the bear call spread is used to (at least partially) pay for the long call. The position profits if the underlying stock rises sharply above the strike price of the long calls.

The advantage of this strategy is that an out-of-the-money call is purchased for a “low” cost, or possibly a net credit. The disadvantages include:

(1) Risk that is greater than the initial net cost, and

(2) A breakeven point that is further from the current stock price than an at-the-money long call.

A 1x2 ratio volatility spread with calls is very sensitive to changing volatility. A “small” increase in stock price accompanied by falling volatility might result in a loss, whereas an at-the-money long call might profit. It is therefore important to believe that volatility is low when establishing this strategy.

Worth noting: The term “volatility” in the strategy name implies that more options are purchased than sold. In contrast, a ratio “vertical” spread is a strategy in which more options are sold than purchased. The 1x2 ratio volatility call spread is also known as a “backspread” because it is generally used with longer-term, or “back-month,” options, as opposed to shorter-term, or “front-month,” options. Longer-term options are more suitable for this strategy because this strategy profits mostly from stock price movement and is hurt by time decay. Longer-term options not only decay at a slower rate than shorter-term options, but they also afford more time for the predicted stock price move to occur.

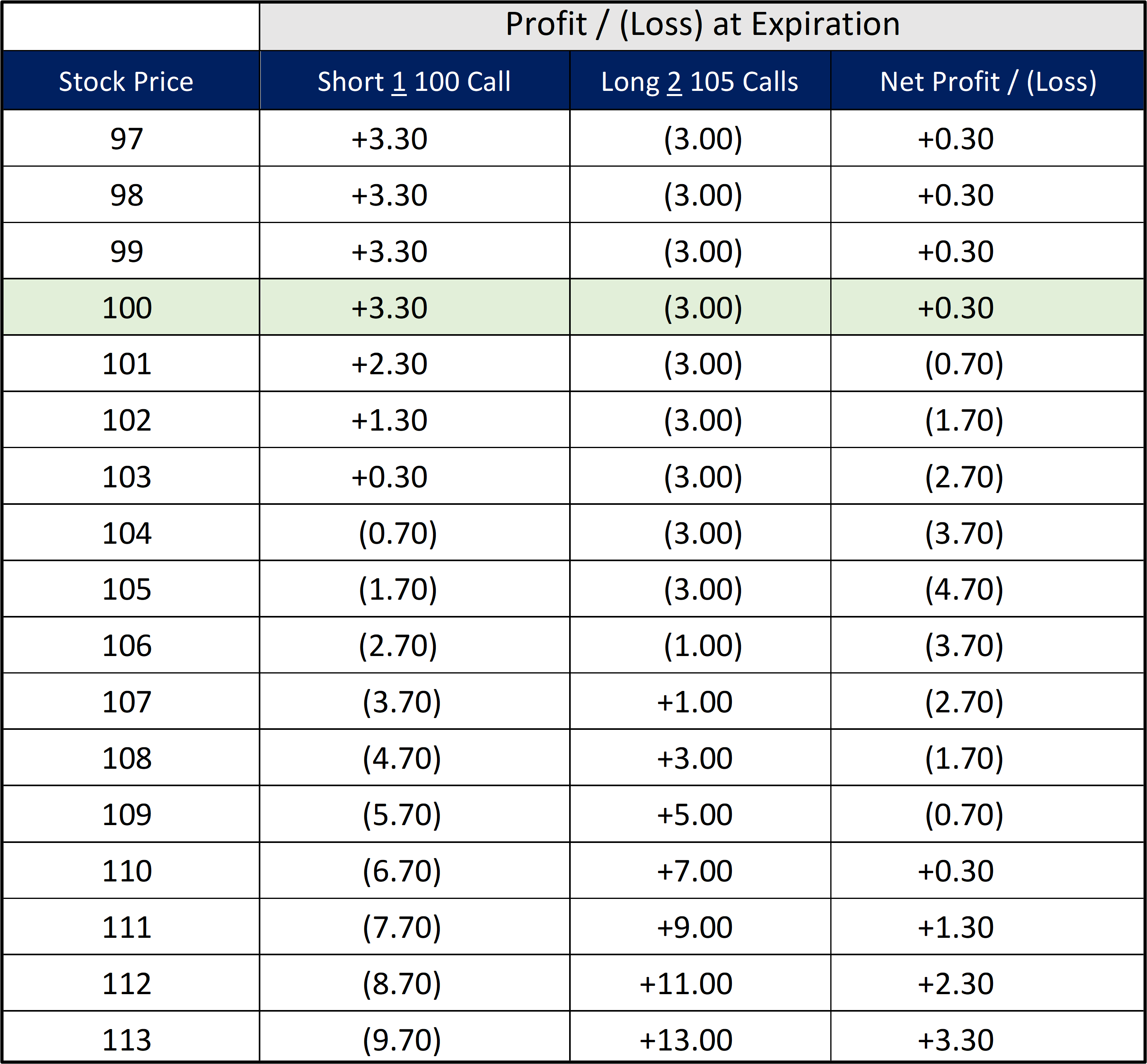

Example

- Short 1 XYZ January 100 call at $3.30

- Long 2 XYZ January 105 calls for $1.50

In our example, assume stock XYZ is currently trading at $100.

We sell 1 XYZ January 100 call for a total of $330 (1 x 100 multiplier x $3.30) and buy 2 XYZ January 105 calls for a total of $300 (2 x 100 multiplier x $1.50).

In this example the 1x2 ratio volatility call spread (1 short call + 2 long calls) positions were established for a net credit of $30 ($330 - $300 = $30).

Outcome 1: Profit

With a 1x2 ratio volatility call spread position, potential profit is unlimited to the upside and limited below the short call strike to the downside.

On the downside, potential profit depends on whether the position is established for a net credit or net debit.

- If established for a net credit including commissions, then

Profit = Net Premium Received

If the stock price is below the lower strike price at expiration, then all options expire worthless and the net credit is kept as a profit.

- If established for a net debit including commissions, then there is no profit on the downside; a loss equal to the net debit is incurred if all options expire worthless.

First, let’s recall the formulas for individual options positions:

Call Options:

If S – K > 0,

Long Call Profit = Current Stock Price – Strike Price – Net Premium Paid

Short Call Loss = -(Current Stock Price – Strike Price – Net Premium Received)

If S – K < 0,

Short Call Profit = Net Premium Received

Long Call Loss = Net Premium Paid

To calculate our profit on the position we established, we use the formula:

Profit = Profit/Loss on Long Calls + Profit/Loss on Short Call

Example

Stock XYZ is trading at $100 and you establish a 1x2 ratio volatility call spread for a $0.30 credit.

- Short 1 XYZ January 100 call for $3.30

- Long 2 XYZ January 105 calls at $1.50

Outcome 2: Loss

Let’s assume we are incorrect in our sentiment, and the stock price rises slightly. To calculate our loss on the position, use the following formula:

Loss = Profit/Loss on Long Calls + Profit/Loss on Short Call

Risk is limited and the maximum loss is realized if the stock price is at the strike price of the long calls at expiration.

At the strike price of the long calls at expiration, the bear call spread is at its maximum value (and maximum loss) and the long calls expire worthless.

§ If the position is established for a net credit (amount received),

Maximum loss = difference between the strike prices − the net credit

In the example above, the maximum risk is 4.70, because the difference between the strike prices is 5.00 (105.00 – 100.00) and the net credit is 0.30. Therefore, 5.00 −0.30 = 4.70.

§ If the position is established for a net debit (cost),

Maximum loss = difference between the strike prices + the net debit

Instead, if the position had been established for a net debit of 50 cents (0.50), the maximum risk would be 5.50, because the difference between the strikes is 5.00 (105.00 – 100.00) so that the maximum loss is 5.00 + 0.50 = 5.50.

Example

See Profit/(Loss) table above.

Outcome 3: Breakeven

If the position is established for a net credit, there are two breakeven points:

- Lower breakeven point: Lower strike price + the net credit

- Higher breakeven point: Higher strike price + the maximum loss

If the position is established for a net debit, there is one breakeven point:

- Breakeven point: Higher strike price + the maximum loss

Note: If this position is established for a net debit, there is no “lower breakeven point.” If the stock price is below the lower strike price at expiration, then all options expire worthless, and the net debit plus commissions is lost.

Example

- Short 1 XYZ January 100 call for $3.30

- Long 2 XYZ January 105 calls at $1.50

Lower Breakeven Price = $100 + $0.30 = $100.30

Higher Breakeven Price = $105 + $4.70 = $109.70

At-A-Glance

Strategy

1x2 ratio volatility call spread

Alternative Name

n/a

Pre-Requisite Strategy Knowledge

Long Call

Short Call

Bear Call Spread

Legs of Trade

2 legs

Sentiment

Bullish

Example

· Short 1 XYZ January 100 call

· Long 2 XYZ January 105 calls

Rule to Remember

n/a

Max Potential Profit (GAIN)

On the upside, profit potential is unlimited, because the position has a long call, and the stock price can rise indefinitely. On the downside, potential profit depends on whether the position is established for a net credit or net debit.

Break-Even Point

See details above

Max Potential Risk (LOSS)

Risk is limited and the maximum is realized if the stock price is at the strike price of the long calls at expiration.

Ideal Outcome

XYZ price rises to or above the long call strike price

Early Assignment Risk

Early assignment risk applies to short options positions only.

Equity options in the United States can be exercised on any business day, and the holder of a short stock options position has no control over when they will be required to fulfill the obligation. Therefore, the risk of early assignment must be considered when entering positions involving short options. Early assignment of stock options is generally related to dividends.

The long calls (higher strike) in a 1x2 ratio volatility call spread have no risk of early assignment.

The short call (lower strike) does have such risk.

If assignment is deemed likely, there are two possibilities:

- First, the short call is assigned. In this case, 100 shares of stock are sold short, and the two long calls remain open.

- Second, the call is not assigned. No matter how likely assignment may seem, there is no assurance that it will occur. In this case the 1x2 ratio volatility spread with calls remains intact.

If early assignment of the short call occurs, stock is sold, and a short stock position of 100 shares is created. Assignment of the short call does not increase the maximum potential risk, because the long calls that limit position risk remain intact.

If early assignment of the short call does occur and if a short stock position is not wanted, the short stock position can be closed by either exercising one of the long calls and leaving the other call open or by purchasing 100 shares in the marketplace and leaving both long calls open.

Note, however, that whichever method is used, the date of the stock purchase will be one day later than the date of the short sale (by assignment of the short call). This difference will result in additional fees, including interest charges and commissions. Assignment of a short call might also trigger a margin call if there is not sufficient account equity to support the short stock position.

Potential Position Created at Expiration

The position at expiration depends on the relationship of the stock price to the strike prices. If the stock price is at or below the strike price of the short call (lower strike), then all options expire worthless and there is no stock position.

If the stock price is above the lower strike but not above the higher strike, then the short call is assigned, and the long calls expire. Assignment of a short call causes stock to be sold at the strike price, so the result is a short stock position. Since options are exercised at expiration if they are one cent ($0.01) in the money, if a short stock position is not wanted, then the short call must be closed (purchased) prior to expiration.

If the stock price is above the higher strike price, then the short call is assigned and both long calls are exercised. In the example above, this means that 100 shares are sold, and 200 shares are purchased. The result is a net long position of 100 shares. If the stock price is above the higher strike immediately prior to expiration, and if a long position of 100 shares is not wanted, then one of the long calls must be sold.

Charts

-Powered by The Options Institute