- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalAssessing Ondas Holdings After a 1028% Surge and Strong DCF Valuation Estimate

- If you are looking at Ondas Holdings and wondering whether the jaw dropping share price run has already priced in the opportunity, you are not alone. That is exactly what this article is going to unpack.

- The stock has rocketed, up 14.8% over the last week, 56.1% over the last month, 244.9% year to date, and an eye catching 1028.2% over the past year, which naturally raises questions about whether this is sustainable growth or froth.

- Much of this momentum has been underpinned by investor excitement around Ondas Holdings position in wireless connectivity solutions and autonomous systems, where regulatory approvals and commercial partnerships have helped put the company on more radar screens. At the same time, coverage from niche tech and infrastructure outlets has framed Ondas as a speculative, high upside player, which can amplify both optimism and volatility when sentiment shifts.

- On our framework, Ondas scores a 3/6 valuation check score, with the details available in our valuation breakdown. In the rest of this piece, we will walk through those different lenses on value before finishing with a more holistic way to think about what the stock might really be worth.

Approach 1: Ondas Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it could generate in the future, then discounting those cash flows back to today in dollar terms.

For Ondas Holdings, the 2 Stage Free Cash Flow to Equity model starts from last twelve month free cash flow of about $35.2 million in the red, reflecting a business still investing heavily. Analysts provide detailed forecasts for the next few years, with Simply Wall St extrapolating beyond that and pointing to a sharp inflection as free cash flow is projected to reach roughly $535.7 million by 2035.

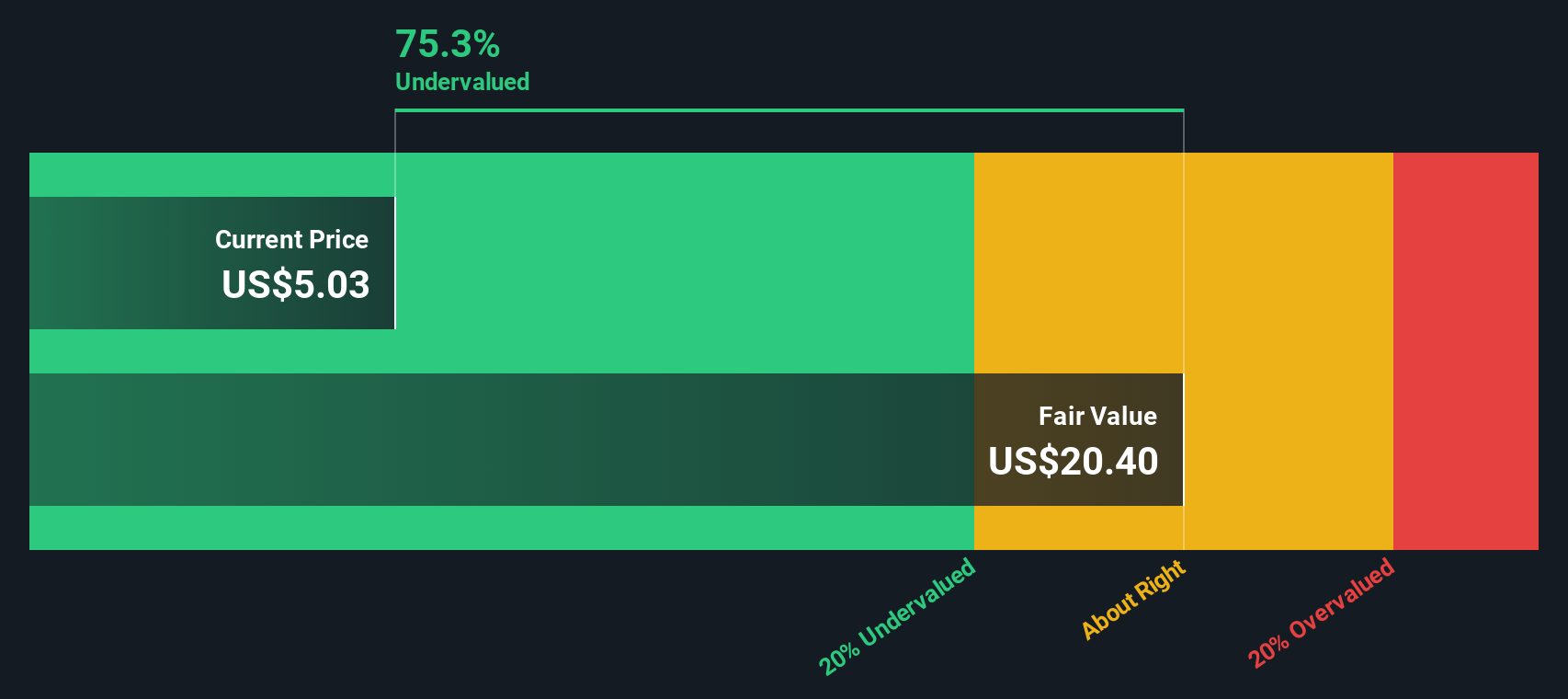

When all those projected cash flows are discounted back, the intrinsic value from this DCF comes out at about $17.84 per share. Compared with the current market price, this implies the stock is roughly 49.2% undervalued. This suggests investors may not be fully pricing in the potential cash generation implied by the model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Ondas Holdings is undervalued by 49.2%. Track this in your watchlist or portfolio, or discover 908 more undervalued stocks based on cash flows.

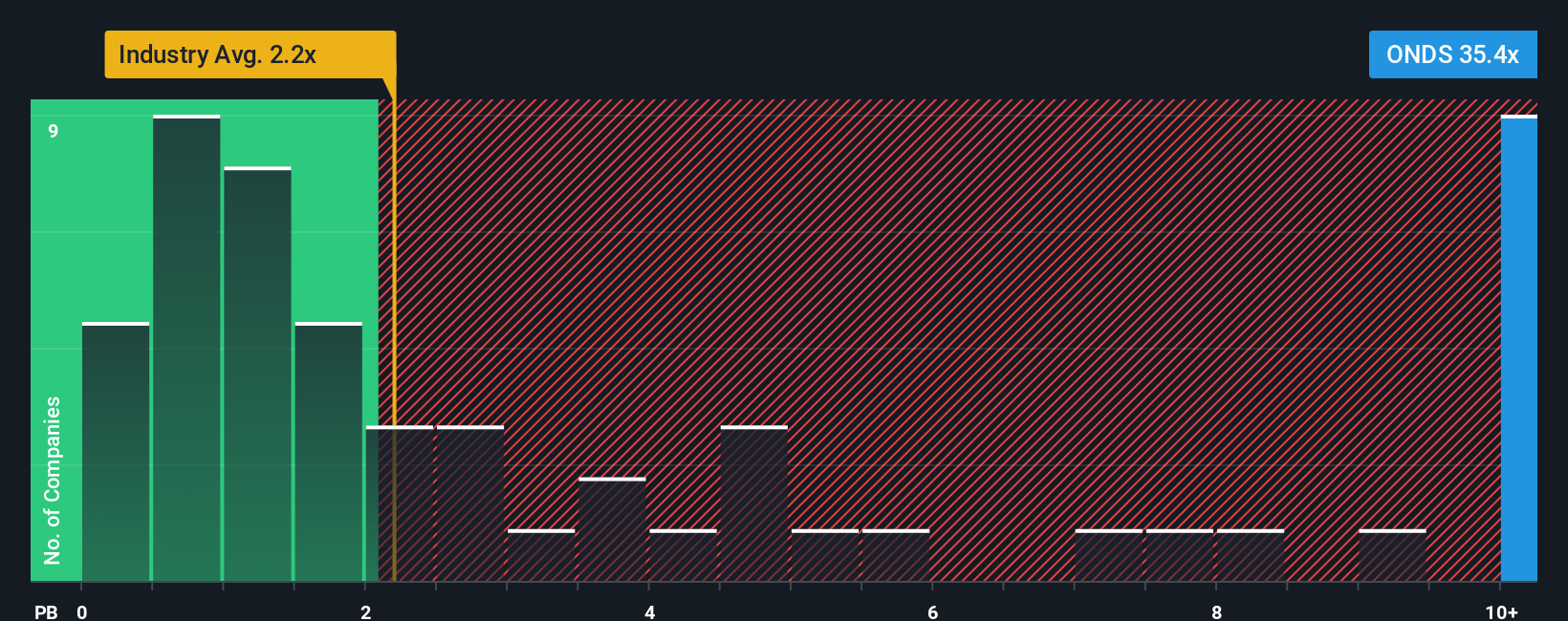

Approach 2: Ondas Holdings Price vs Book

For companies that are still loss making or early in their commercial ramp up, price to book is often a more useful anchor than earnings based metrics, because it relates the share price to the net assets supporting the business rather than volatile or negative profits.

In general, faster growth and lower risk justify a higher multiple, while slower growth, weak profitability or balance sheet strain usually mean investors should demand a lower, more conservative ratio. Against that backdrop, Ondas currently trades on a price to book of about 6.95x, well above both the Communications industry average of roughly 1.95x and a peer group average near 3.58x. This signals that the market is paying a hefty premium to the sector for each dollar of equity on the balance sheet.

Simply Wall St’s Fair Ratio is a proprietary estimate of what Ondas price to book should be, after accounting for factors like expected growth, profitability, risk profile, industry positioning and market capitalization. Because it blends all of these drivers into a single yardstick, it offers a more tailored benchmark than simple peer or industry comparisons. On this view, Ondas current 6.95x multiple screens as stretched relative to where the Fair Ratio would likely sit. This points to a stock that is priced ahead of fundamentals.

Result: OVERVALUED

PB ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1452 companies where insiders are betting big on explosive growth.

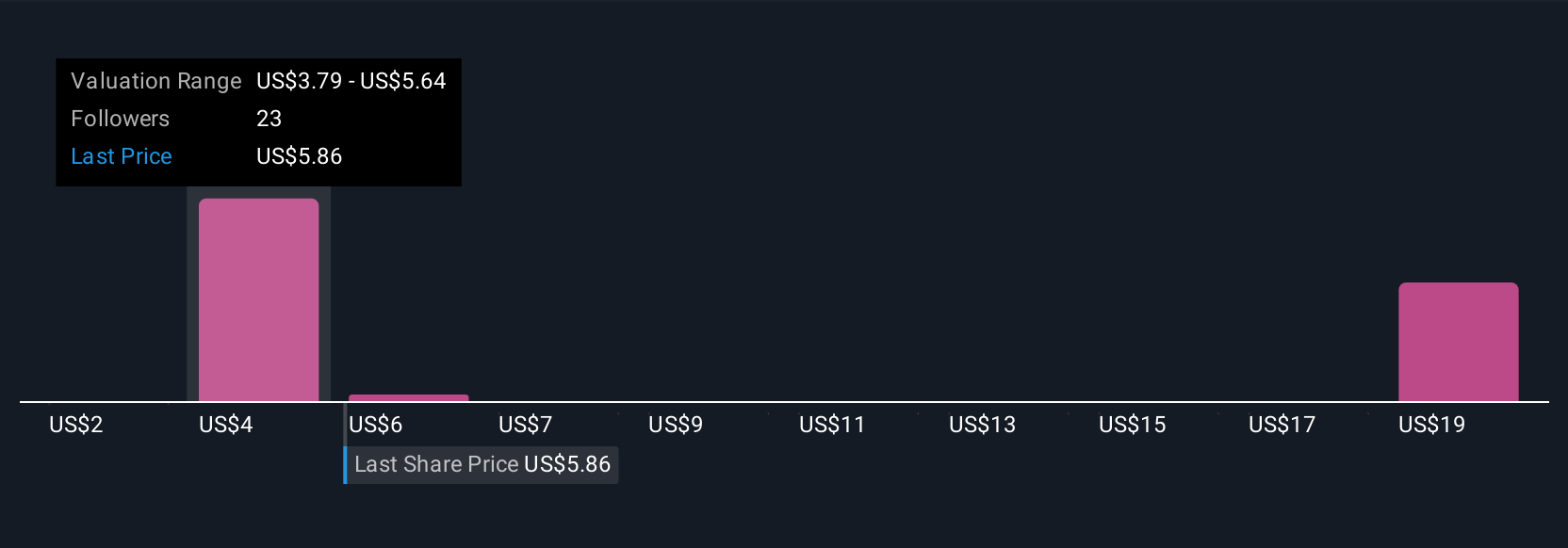

Upgrade Your Decision Making: Choose your Ondas Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple framework on Simply Wall St’s Community page. There, you connect your story about Ondas Holdings with your own numbers for future revenue, earnings and margins, link that story to a financial forecast and a fair value estimate, then compare that fair value to today’s price to decide whether you think the stock is a buy, hold or sell. The platform dynamically updates your Narrative as fresh news or earnings arrive. For example, one investor might build a bullish Ondas Narrative anchored around an $11.00 fair value driven by backlog expansion and defense contracts. Another could create a more cautious Narrative with a much lower fair value that leans on concerns about debt, dilution and execution risk. Both views can coexist transparently so you can see exactly which assumptions would have to be true for each version of the story to play out.

Do you think there's more to the story for Ondas Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com