- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalMarket Participants Recognise Lumos Diagnostics Holdings Limited's (ASX:LDX) Revenues Pushing Shares 37% Higher

Despite an already strong run, Lumos Diagnostics Holdings Limited (ASX:LDX) shares have been powering on, with a gain of 37% in the last thirty days. The last 30 days were the cherry on top of the stock's 515% gain in the last year, which is nothing short of spectacular.

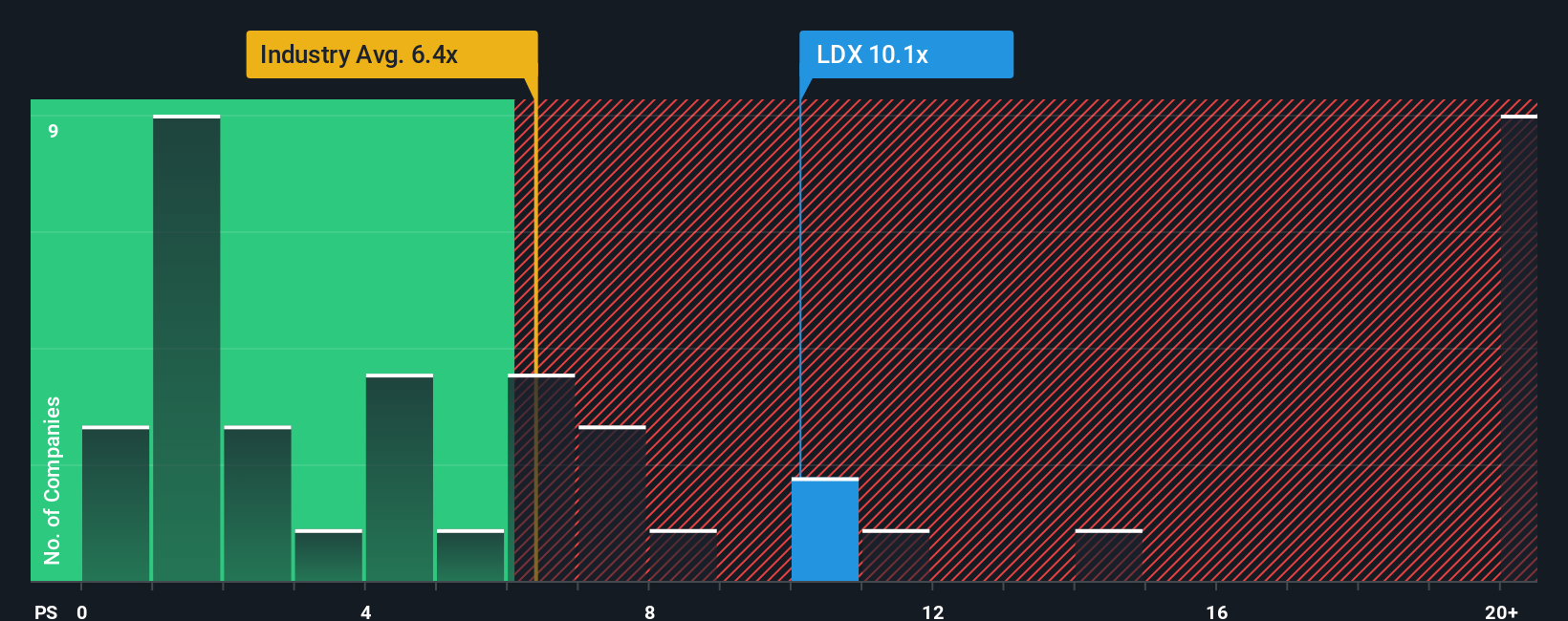

After such a large jump in price, Lumos Diagnostics Holdings may be sending strong sell signals at present with a price-to-sales (or "P/S") ratio of 10.1x, when you consider almost half of the companies in the Medical Equipment industry in Australia have P/S ratios under 6.4x and even P/S lower than 2x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

View our latest analysis for Lumos Diagnostics Holdings

How Has Lumos Diagnostics Holdings Performed Recently?

Lumos Diagnostics Holdings' revenue growth of late has been pretty similar to most other companies. One possibility is that the P/S ratio is high because investors think this modest revenue performance will accelerate. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Lumos Diagnostics Holdings.How Is Lumos Diagnostics Holdings' Revenue Growth Trending?

The only time you'd be truly comfortable seeing a P/S as steep as Lumos Diagnostics Holdings' is when the company's growth is on track to outshine the industry decidedly.

If we review the last year of revenue growth, the company posted a worthy increase of 11%. Revenue has also lifted 6.6% in aggregate from three years ago, partly thanks to the last 12 months of growth. Therefore, it's fair to say the revenue growth recently has been respectable for the company.

Looking ahead now, revenue is anticipated to climb by 69% during the coming year according to the lone analyst following the company. That's shaping up to be materially higher than the 43% growth forecast for the broader industry.

With this in mind, it's not hard to understand why Lumos Diagnostics Holdings' P/S is high relative to its industry peers. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

The Final Word

Lumos Diagnostics Holdings' P/S has grown nicely over the last month thanks to a handy boost in the share price. Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our look into Lumos Diagnostics Holdings shows that its P/S ratio remains high on the merit of its strong future revenues. Right now shareholders are comfortable with the P/S as they are quite confident future revenues aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

You need to take note of risks, for example - Lumos Diagnostics Holdings has 2 warning signs (and 1 which doesn't sit too well with us) we think you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.