- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalFintech Integrations Might Change The Case For Investing In Moody's (MCO)

- Pegasystems and Entegra recently announced separate collaborations with Moody’s, embedding its entity verification and cash flow analytics into their platforms to streamline KYC, client onboarding, and structured finance trading workflows for financial institutions.

- By plugging Moody’s real-time data and analytics into widely used financial technology systems, these deals deepen its role in day‑to‑day risk, compliance, and trading decisions across global markets.

- Next, we’ll examine how embedding Moody’s real-time data into third-party platforms could influence its investment narrative and growth outlook.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

Moody's Investment Narrative Recap

To own Moody’s, you generally need to believe its data, analytics, and ratings will stay embedded in the core plumbing of global finance, supporting steady earnings growth despite its premium valuation and high leverage. The Pegasystems and Entegra integrations modestly reinforce the near term catalyst around expanding analytics distribution, but do not fundamentally change the most important swing factor right now, which remains regulatory and political scrutiny of fast growing private credit markets.

Among recent developments, the Pegasystems collaboration is most directly connected to this story, because it pushes Moody’s KYC and entity verification data deeper into everyday onboarding and compliance workflows at major financial institutions. That kind of integration aligns with the broader catalyst of using AI enabled products and third party partnerships to build recurring, workflow based revenue streams that can help offset margin pressure if regulation tightens or pricing power is challenged elsewhere.

Yet while these integrations can help entrench Moody’s data, rising scrutiny of opaque private credit exposure is a risk investors should be aware of, especially if...

Read the full narrative on Moody's (it's free!)

Moody's narrative projects $9.0 billion revenue and $3.0 billion earnings by 2028.

Uncover how Moody's forecasts yield a $545.50 fair value, a 10% upside to its current price.

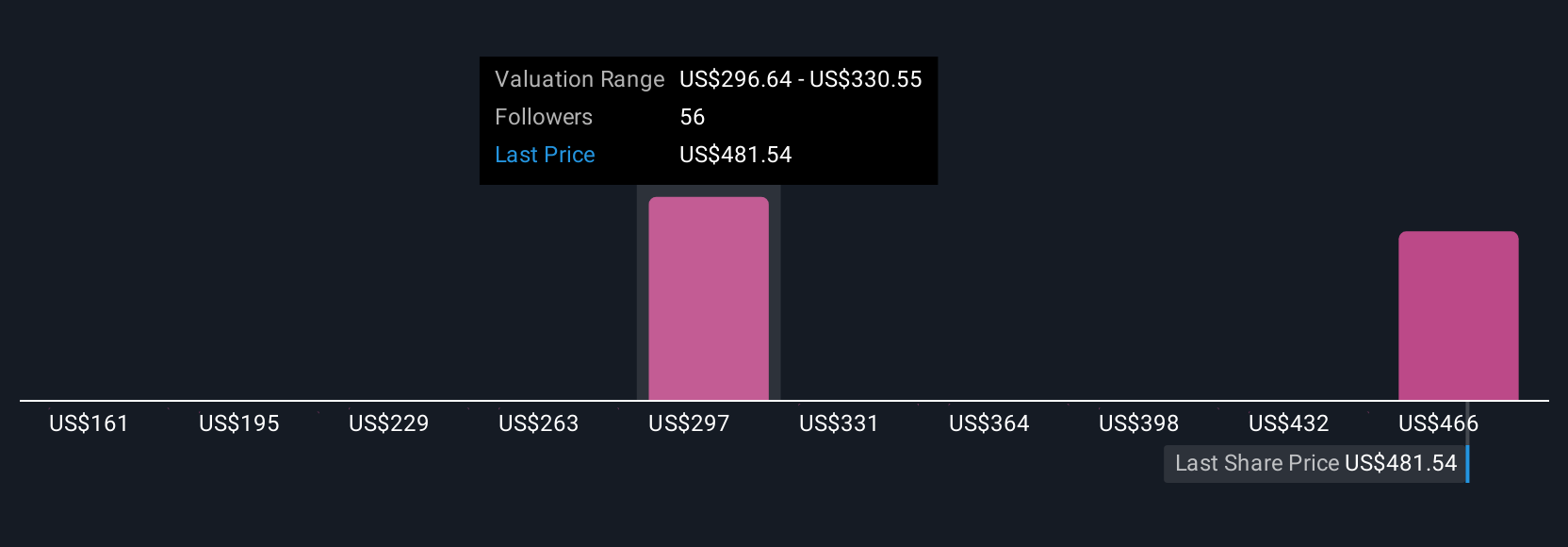

Exploring Other Perspectives

Eight members of the Simply Wall St Community currently see Moody’s fair value spread widely between about US$321 and US$546 per share. Against that backdrop, ongoing investment in AI powered analytics and third party integrations could be an important swing factor for how reliably Moody’s converts its entrenched position into future earnings power, so it is worth comparing several of these viewpoints before deciding where you stand.

Explore 8 other fair value estimates on Moody's - why the stock might be worth as much as 10% more than the current price!

Build Your Own Moody's Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Moody's research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Moody's research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Moody's overall financial health at a glance.

No Opportunity In Moody's?

Our top stock finds are flying under the radar-for now. Get in early:

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 36 companies in the world exploring or producing it. Find the list for free.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com