- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalDoes Hong Kong Johnson Holdings (HKG:1955) Have A Healthy Balance Sheet?

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Hong Kong Johnson Holdings Co., Ltd. (HKG:1955) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

How Much Debt Does Hong Kong Johnson Holdings Carry?

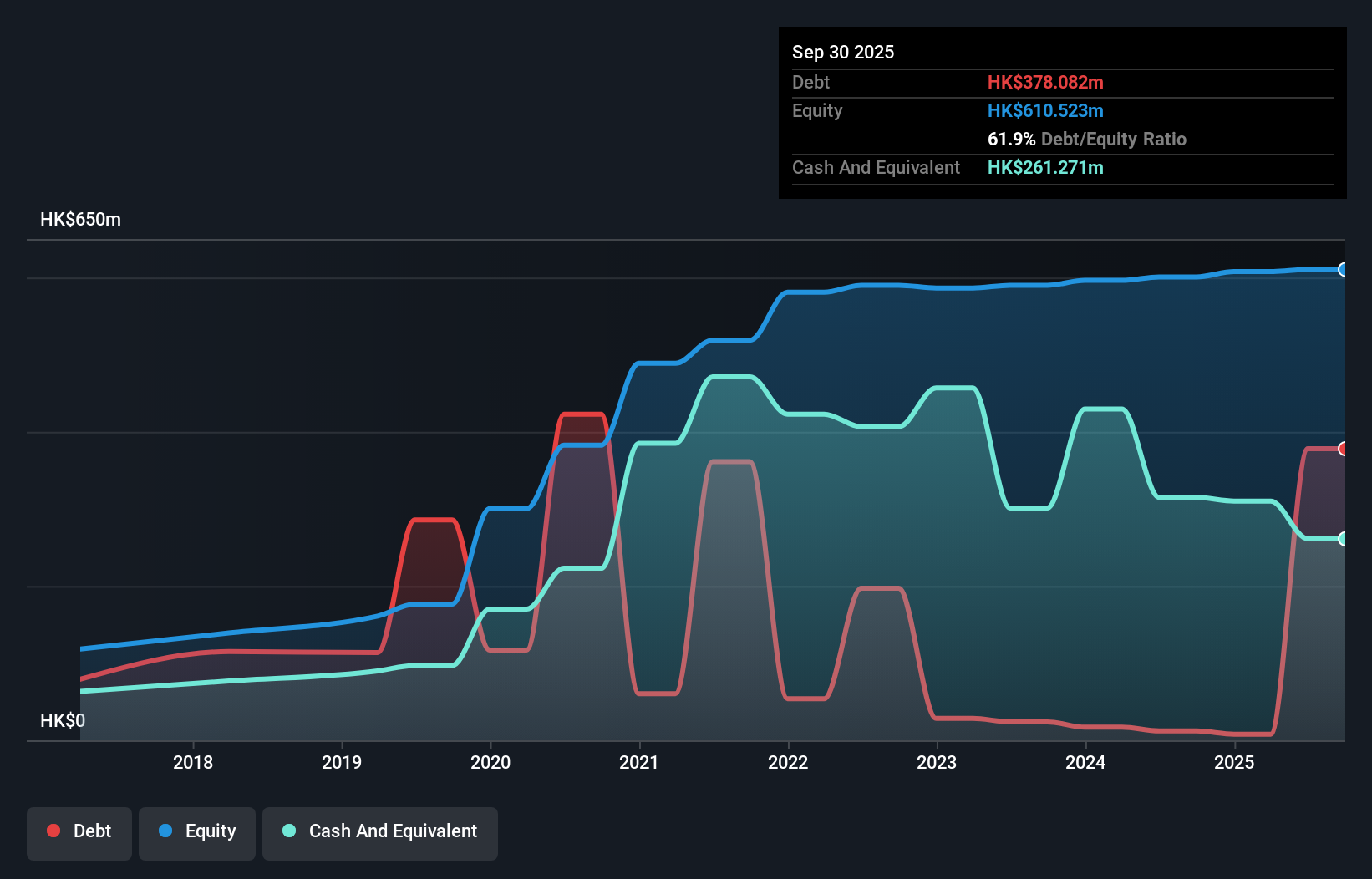

The image below, which you can click on for greater detail, shows that at September 2025 Hong Kong Johnson Holdings had debt of HK$378.1m, up from HK$12.1m in one year. However, it does have HK$261.3m in cash offsetting this, leading to net debt of about HK$116.8m.

A Look At Hong Kong Johnson Holdings' Liabilities

The latest balance sheet data shows that Hong Kong Johnson Holdings had liabilities of HK$790.3m due within a year, and liabilities of HK$13.5m falling due after that. Offsetting these obligations, it had cash of HK$261.3m as well as receivables valued at HK$851.8m due within 12 months. So it can boast HK$309.3m more liquid assets than total liabilities.

This luscious liquidity implies that Hong Kong Johnson Holdings' balance sheet is sturdy like a giant sequoia tree. On this view, lenders should feel as safe as the beloved of a black-belt karate master.

See our latest analysis for Hong Kong Johnson Holdings

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Hong Kong Johnson Holdings's net debt is 2.8 times its EBITDA, which is a significant but still reasonable amount of leverage. But its EBIT was about 24.7 times its interest expense, implying the company isn't really paying a high cost to maintain that level of debt. Even were the low cost to prove unsustainable, that is a good sign. Importantly, Hong Kong Johnson Holdings grew its EBIT by 63% over the last twelve months, and that growth will make it easier to handle its debt. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since Hong Kong Johnson Holdings will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Looking at the most recent three years, Hong Kong Johnson Holdings recorded free cash flow of 45% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

Hong Kong Johnson Holdings's interest cover suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. But, on a more sombre note, we are a little concerned by its net debt to EBITDA. It looks Hong Kong Johnson Holdings has no trouble standing on its own two feet, and it has no reason to fear its lenders. For investing nerds like us its balance sheet is almost charming. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for Hong Kong Johnson Holdings (1 is a bit concerning!) that you should be aware of before investing here.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.