- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalIs It Too Late To Consider Banco Latinoamericano de Comercio Exterior After Its Strong 2025 Rally?

- If you are wondering whether Banco Latinoamericano de Comercio Exterior S. A at around $45 a share is still a smart buy or if the easy money has already been made, you are not alone, and that is exactly what we are going to unpack.

- The stock is up 26.8% year to date and 34.9% over the last year, while longer term holders have seen gains of 228.1% over three years and 291.7% over five years, even though the last week has been basically flat at around -0.1% and the last month up 4.1%.

- Those moves have come as investors have been paying closer attention to the bank's role in financing trade flows across Latin America, alongside broader optimism toward regional financials as risk appetite improves. At the same time, shifting expectations around interest rates and global trade demand have added an extra layer of intrigue to how sustainable these gains might be.

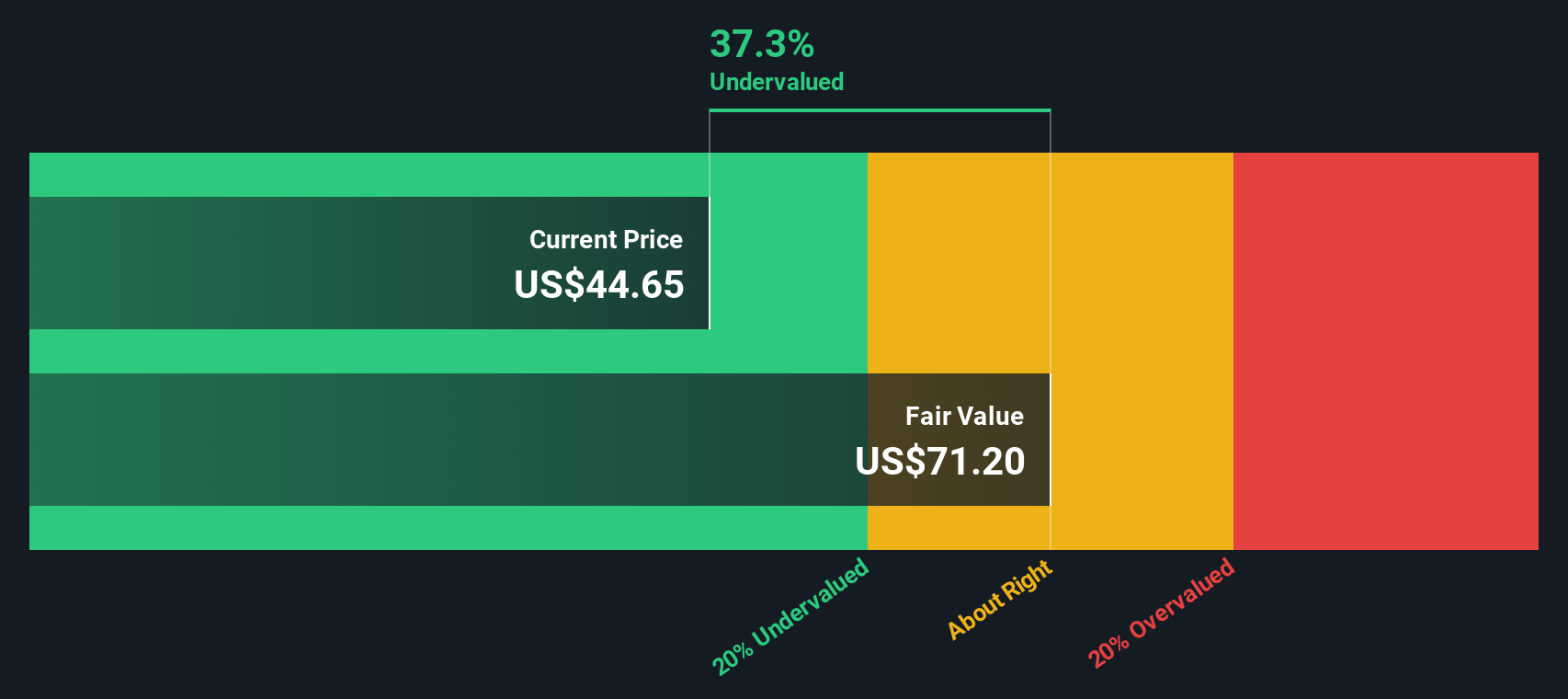

- Right now the stock scores a strong 5 out of 6 on our valuation checks, suggesting it still looks undervalued on most of the metrics that matter. Next we will walk through those valuation approaches, before finishing with a more holistic way to decide what the stock is really worth.

Approach 1: Banco Latinoamericano de Comercio Exterior S. A Excess Returns Analysis

The Excess Returns model looks at how much value a bank creates above the minimum return investors require, then capitalizes those surplus profits into an intrinsic value per share. In simple terms, it asks whether Banco Latinoamericano de Comercio Exterior S. A is earning enough on its equity to justify a premium over book value.

For BLX, the model starts with a Book Value of $44.22 per share and a Stable EPS of $6.31 per share, based on the median return on equity from the past 5 years. With an Average Return on Equity of 14.58% and a Cost of Equity of $4.40 per share, the bank generates an Excess Return of $1.91 per share on a Stable Book Value base of $43.25 per share, supported by estimates from two analysts.

When those excess returns are projected forward and discounted, the Excess Returns valuation implies an intrinsic value of about $70.94 per share, indicating the stock is roughly 36.4% undervalued versus the current market price.

Result: UNDERVALUED

Our Excess Returns analysis suggests Banco Latinoamericano de Comercio Exterior S. A is undervalued by 36.4%. Track this in your watchlist or portfolio, or discover 912 more undervalued stocks based on cash flows.

Approach 2: Banco Latinoamericano de Comercio Exterior S. A Price vs Earnings

For profitable banks, the price to earnings ratio is a straightforward way to judge whether investors are paying a reasonable price for each dollar of earnings. In general, faster growth and lower perceived risk justify a higher PE multiple, while slower growth or higher risk usually mean a lower, more conservative multiple is appropriate.

Banco Latinoamericano de Comercio Exterior S. A currently trades on about 7.46x earnings, which is well below both the Diversified Financial industry average of roughly 13.81x and the broader peer group average near 29.97x. On the surface, that discount suggests the market is cautious about the bank relative to its sector and peers.

Simply Wall St’s Fair Ratio framework estimates that, given BLX’s earnings growth outlook, profitability, size, industry positioning and risk profile, a more appropriate multiple would be around 12.25x. This is more tailored than a simple comparison to industry or peers, because it explicitly adjusts for company specific drivers such as growth, margins and risk. With the current PE of 7.46x sitting well below the 12.25x Fair Ratio, the multiple based view points to the shares still being undervalued at today’s price.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Banco Latinoamericano de Comercio Exterior S. A Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to turn your view of Banco Latinoamericano de Comercio Exterior S. A into a story that connects assumptions about future revenue, earnings and margins to a clear fair value estimate, all within Simply Wall St’s Community page that millions of investors use.

A Narrative is your personal storyline for the company, where you spell out why the business will or will not grow, translate that into a financial forecast, and then compare the resulting Fair Value to today’s Price to decide whether it looks like a buy, a hold or a sell, with the model updating dynamically whenever new information such as earnings or major news is released.

For example, one BLX investor might build a bullish Narrative that focuses on strong asset quality, the digital trade finance platform and stable margins to reach a Fair Value near the high analyst target of about $55. A more cautious investor could instead emphasize sovereign risk, reliance on large transactions and macro volatility to arrive closer to the low target near $37. This shows how different perspectives can coexist while still staying grounded in numbers.

Do you think there's more to the story for Banco Latinoamericano de Comercio Exterior S. A? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com