- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalCellebrite DI (CLBT) Is Up 8.1% After Q3 Beat And Corellium Deal - What's Changed

- Cellebrite DI recently reported Q3 results that exceeded expectations, highlighting strong operational execution, resilient demand for its digital investigation platforms, and rapid growth of its Guardian solution among defense and intelligence agencies.

- The completed US$170 million Corellium acquisition adds Arm-based virtualization and strengthens Cellebrite’s AI-powered investigation stack, potentially broadening use cases across defense, intelligence, and enterprise customers.

- We’ll now examine how this stronger-than-expected Q3 performance, alongside Guardian’s momentum, reshapes Cellebrite’s investment narrative and longer-term outlook.

Outshine the giants: these 26 early-stage AI stocks could fund your retirement.

Cellebrite DI Investment Narrative Recap

To own Cellebrite, you need to believe digital investigations will keep moving toward integrated, AI-enabled platforms and that the company can convert this shift into durable, subscription-led growth. The Q3 beat and Guardian’s traction support this view, but contract delays in the U.S. federal segment remain the key near term swing factor, while execution on Corellium integration is an emerging risk that could affect how quickly new use cases translate into financial outcomes.

The completion of the US$170,000,000 Corellium acquisition looks most relevant here, as it deepens Cellebrite’s technology stack around Arm-based virtualization and device access. While management does not expect a material impact on near term guidance, Corellium’s capabilities sit directly against the main growth catalysts in digital forensics and advanced analytics, making execution on this deal an important test of Cellebrite’s ability to turn innovation investments into higher quality, recurring revenue over time.

Yet behind the strong Q3 share reaction, investors should also be aware of how persistent U.S. federal contract delays could...

Read the full narrative on Cellebrite DI (it's free!)

Cellebrite DI's narrative projects $671.4 million revenue and $128.8 million earnings by 2028. This requires 15.4% yearly revenue growth and a $279.7 million earnings increase from $-150.9 million today.

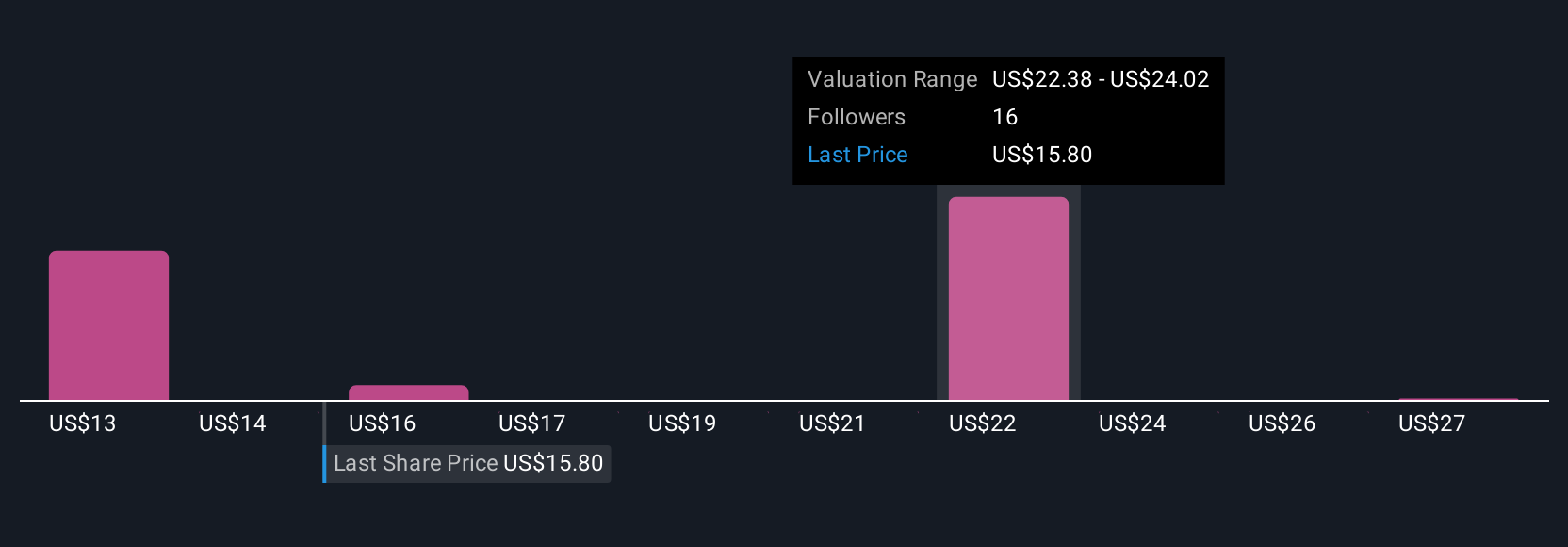

Uncover how Cellebrite DI's forecasts yield a $24.71 fair value, a 36% upside to its current price.

Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community span a wide range, from about US$13.60 up to US$32. Against this dispersion in expectations, the reliance on delayed U.S. federal contracts raises clear questions about how quickly Cellebrite can convert its product momentum into consistent growth, so it makes sense to review several viewpoints before deciding how these risks and opportunities might fit your portfolio.

Explore 6 other fair value estimates on Cellebrite DI - why the stock might be worth as much as 76% more than the current price!

Build Your Own Cellebrite DI Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cellebrite DI research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Cellebrite DI research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cellebrite DI's overall financial health at a glance.

Searching For A Fresh Perspective?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com