- PREMIUM

- LIVE QUOTES

- INSTITUTION

Index Options

Index Options State Street

State Street CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalIs Roku Still Attractive After Its 26.9% 2025 Rally and Advertising Expansion?

- Wondering if Roku at around $94 is still a deal or if the easy money has already been made? You are not alone; that is exactly what we are going to unpack here.

- The stock is up 26.9% year to date and 12.4% over the last year, even after a choppy month where it slipped 10.5% and is down 2.3% in the last week, reminding investors that volatility and opportunity often travel together.

- Recent headlines have focused on Roku expanding its advertising ecosystem and deepening content partnerships, which investors see as key to monetizing its large user base. At the same time, ongoing competition in streaming hardware and platforms has kept sentiment mixed, helping to explain the sharp price swings.

- On our framework, Roku scores a 3/6 valuation check rating, suggesting it screens as undervalued on some metrics but not across the board. We will walk through what different valuation methods say about the stock today and finish with a more intuitive way to think about its true worth.

Approach 1: Roku Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a company is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today in dollar terms.

For Roku, the model starts with last twelve months Free Cash Flow of about $394.9 million and uses a 2 Stage Free Cash Flow to Equity approach. Analysts provide detailed estimates for the next few years, with Simply Wall St extrapolating further out. This results in projected Free Cash Flow rising to roughly $1.31 billion by 2029 and continuing to grow through 2035. Each of these future cash flows is discounted back, reflecting both the time value of money and Roku’s risk profile.

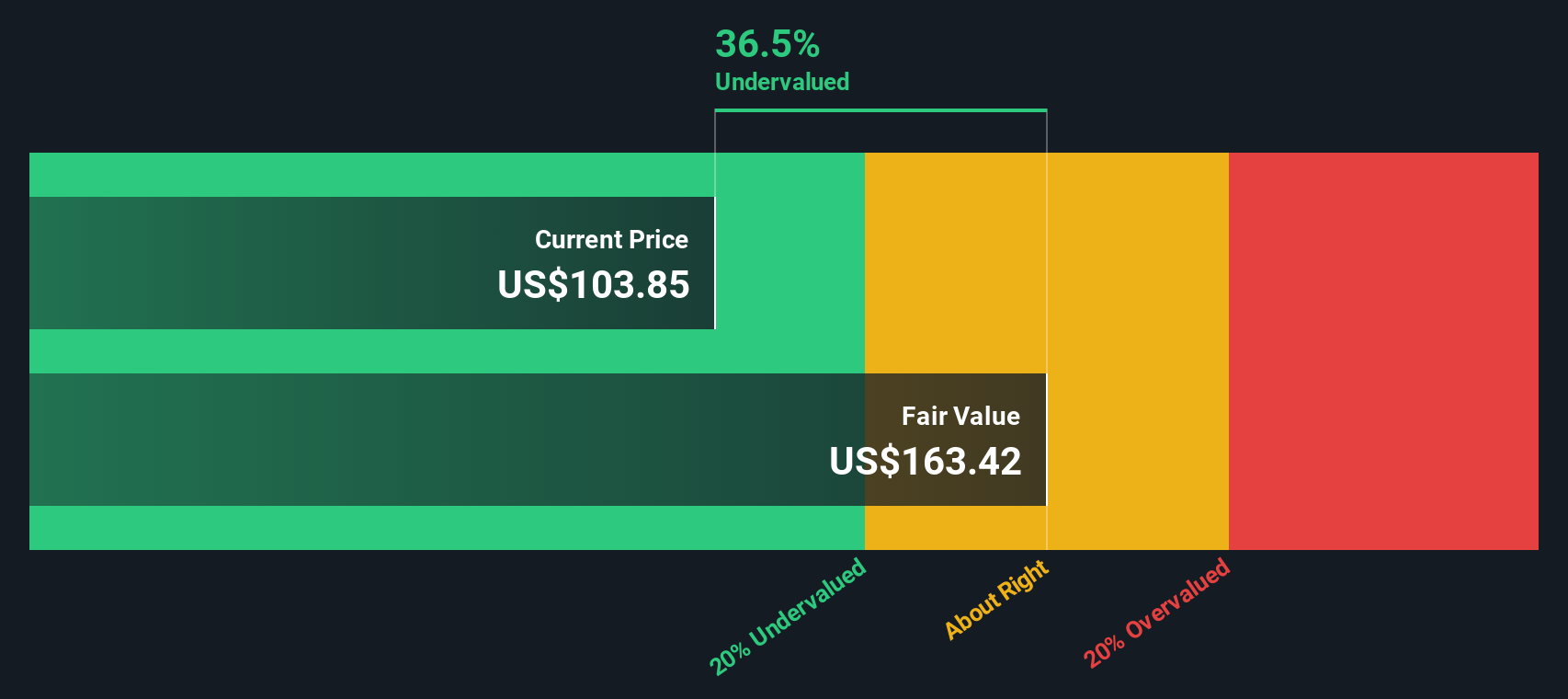

When all those discounted cash flows are combined, the model derives an estimated intrinsic value of $155.27 per share. Compared with a current share price around $94, this implies Roku is trading at about a 39.1% discount to its DCF fair value, suggesting potential upside if these projections prove accurate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Roku is undervalued by 39.1%. Track this in your watchlist or portfolio, or discover 912 more undervalued stocks based on cash flows.

Approach 2: Roku Price vs Sales

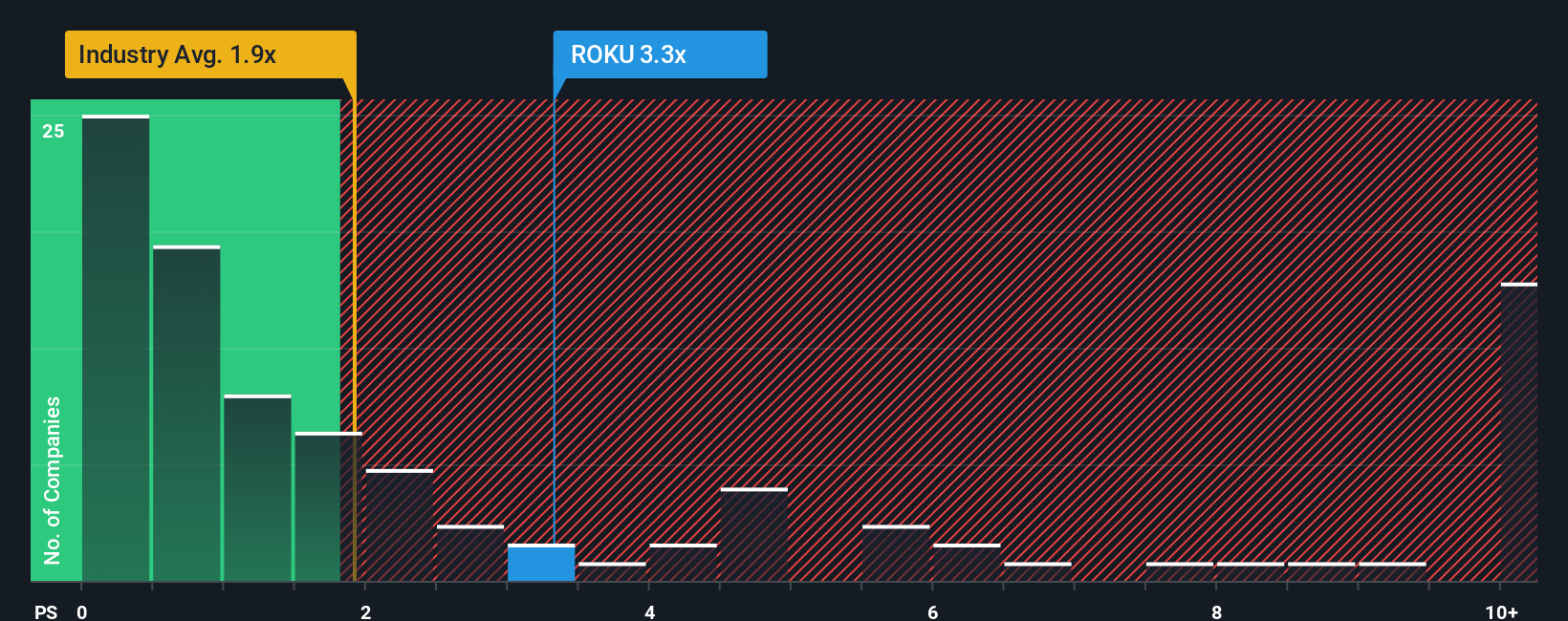

For a company like Roku that is still prioritizing scale and reinvestment over steady profits, the Price to Sales ratio is a more reliable valuation lens than earnings based metrics. It focuses on how much investors are paying for each dollar of revenue, which is especially useful when margins are still normalizing.

In general, higher expected growth and lower perceived risk justify a higher normal or fair multiple. Slower growth or greater uncertainty should pull that multiple down. Roku currently trades on a Price to Sales ratio of about 3.07x, ahead of the Entertainment industry average of roughly 1.47x and below the peer average of around 3.97x. Simply Wall St’s proprietary Fair Ratio for Roku is 2.41x, which estimates the multiple the stock deserves once you factor in its growth outlook, profitability profile, industry, market cap and risk characteristics.

This Fair Ratio is more informative than a simple peer or industry comparison because it explicitly adjusts for Roku’s specific mix of strengths and risks rather than assuming all streaming or media names deserve the same multiple. With the current 3.07x sitting above the 2.41x Fair Ratio, Roku screens as somewhat expensive on a sales basis.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Roku Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a feature on Simply Wall St’s Community page that lets you turn your view of Roku’s future into a simple story linked to a financial forecast and a fair value. You can then compare that fair value with today’s price to decide whether to buy or sell. The Narrative automatically updates as new news or earnings arrive so your assumptions stay fresh. One investor might build a bullish Roku Narrative that leans into accelerating streaming ad spend, improving margins and a fair value around $130 per share. Another, more cautious investor could focus on intensifying competition, ad cyclicality and execution risk and land on a $70 fair value. Both are using the same structured, accessible framework to explain their assumptions about future revenue, earnings and margins rather than just blindly following headline multiples.

Do you think there's more to the story for Roku? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com