Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalWe Think Guangzhou Hangxin Aviation Technology (SZSE:300424) Can Stay On Top Of Its Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. Importantly, Guangzhou Hangxin Aviation Technology Co., Ltd. (SZSE:300424) does carry debt. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for Guangzhou Hangxin Aviation Technology

What Is Guangzhou Hangxin Aviation Technology's Net Debt?

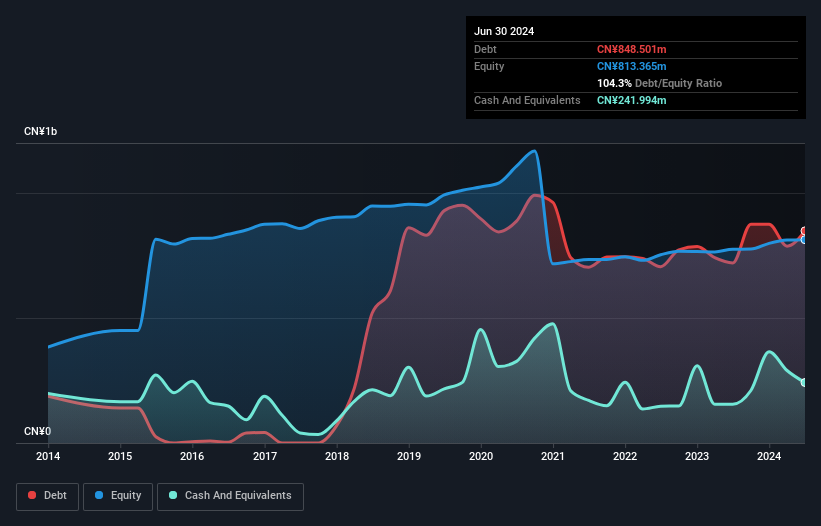

You can click the graphic below for the historical numbers, but it shows that as of June 2024 Guangzhou Hangxin Aviation Technology had CN¥848.5m of debt, an increase on CN¥720.3m, over one year. However, it also had CN¥242.0m in cash, and so its net debt is CN¥606.5m.

How Healthy Is Guangzhou Hangxin Aviation Technology's Balance Sheet?

According to the last reported balance sheet, Guangzhou Hangxin Aviation Technology had liabilities of CN¥1.01b due within 12 months, and liabilities of CN¥547.2m due beyond 12 months. Offsetting this, it had CN¥242.0m in cash and CN¥752.6m in receivables that were due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥561.9m.

Given Guangzhou Hangxin Aviation Technology has a market capitalization of CN¥3.72b, it's hard to believe these liabilities pose much threat. However, we do think it is worth keeping an eye on its balance sheet strength, as it may change over time.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

While we wouldn't worry about Guangzhou Hangxin Aviation Technology's net debt to EBITDA ratio of 4.3, we think its super-low interest cover of 1.9 times is a sign of high leverage. It seems that the business incurs large depreciation and amortisation charges, so maybe its debt load is heavier than it would first appear, since EBITDA is arguably a generous measure of earnings. It seems clear that the cost of borrowing money is negatively impacting returns for shareholders, of late. Looking on the bright side, Guangzhou Hangxin Aviation Technology boosted its EBIT by a silky 63% in the last year. Like a mother's loving embrace of a newborn that sort of growth builds resilience, putting the company in a stronger position to manage its debt. There's no doubt that we learn most about debt from the balance sheet. But it is Guangzhou Hangxin Aviation Technology's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So it's worth checking how much of that EBIT is backed by free cash flow. In the last three years, Guangzhou Hangxin Aviation Technology's free cash flow amounted to 30% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Our View

On our analysis Guangzhou Hangxin Aviation Technology's EBIT growth rate should signal that it won't have too much trouble with its debt. However, our other observations weren't so heartening. In particular, interest cover gives us cold feet. We would also note that Infrastructure industry companies like Guangzhou Hangxin Aviation Technology commonly do use debt without problems. Considering this range of data points, we think Guangzhou Hangxin Aviation Technology is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Be aware that Guangzhou Hangxin Aviation Technology is showing 3 warning signs in our investment analysis , and 2 of those are potentially serious...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.