Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalThere Might Be More To ABEJA's (TSE:5574) Story Than Just Weak Earnings

The market shrugged off ABEJA, Inc.'s (TSE:5574) weak earnings report. Despite the market responding positively, we think that there are several concerning factors that investors should be aware of.

Check out our latest analysis for ABEJA

Examining Cashflow Against ABEJA's Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

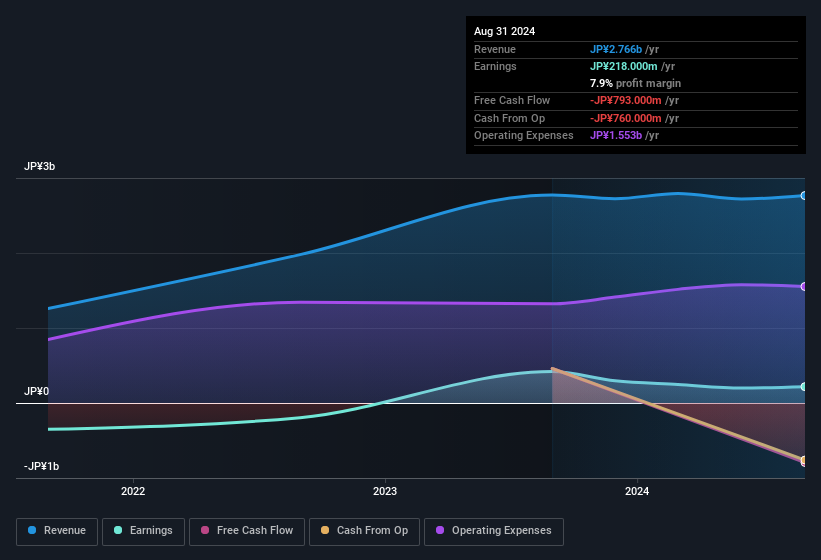

Over the twelve months to August 2024, ABEJA recorded an accrual ratio of 1.93. Statistically speaking, that's a real negative for future earnings. And indeed, during the period the company didn't produce any free cash flow whatsoever. In the last twelve months it actually had negative free cash flow, with an outflow of JP¥793m despite its profit of JP¥218.0m, mentioned above. We saw that FCF was JP¥460m a year ago though, so ABEJA has at least been able to generate positive FCF in the past. Notably, the company has issued new shares, thus diluting existing shareholders and reducing their share of future earnings. The good news for shareholders is that ABEJA's accrual ratio was much better last year, so this year's poor reading might simply be a case of a short term mismatch between profit and FCF. As a result, some shareholders may be looking for stronger cash conversion in the current year.

Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of ABEJA.

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. In fact, ABEJA increased the number of shares on issue by 7.7% over the last twelve months by issuing new shares. As a result, its net income is now split between a greater number of shares. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. Check out ABEJA's historical EPS growth by clicking on this link.

A Look At The Impact Of ABEJA's Dilution On Its Earnings Per Share (EPS)

ABEJA was losing money three years ago. And even focusing only on the last twelve months, we see profit is down 48%. Sadly, earnings per share fell further, down a full 55% in that time. So you can see that the dilution has had a bit of an impact on shareholders.

If ABEJA's EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Our Take On ABEJA's Profit Performance

In conclusion, ABEJA has weak cashflow relative to earnings, which indicates lower quality earnings, and the dilution means that shareholders now own a smaller proportion of the company (assuming they maintained the same number of shares). Considering all this we'd argue ABEJA's profits probably give an overly generous impression of its sustainable level of profitability. Keep in mind, when it comes to analysing a stock it's worth noting the risks involved. When we did our research, we found 5 warning signs for ABEJA (3 are potentially serious!) that we believe deserve your full attention.

Our examination of ABEJA has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.