Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street Journal3 Growth Companies With High Insider Ownership On The UK Exchange

The United Kingdom market has shown robust performance with a 1.6% increase in the last week and an impressive 11% rise over the past year, while earnings are anticipated to grow by 14% annually in the coming years. In this thriving environment, growth companies with high insider ownership can be particularly appealing as they often indicate strong confidence from those closest to the business, aligning their interests with shareholders and potentially enhancing long-term value creation.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Gulf Keystone Petroleum (LSE:GKP) | 12.2% | 82.5% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 27.6% | 23.7% |

| LSL Property Services (LSE:LSL) | 10.8% | 28.2% |

| Judges Scientific (AIM:JDG) | 10.6% | 23% |

| Enteq Technologies (AIM:NTQ) | 20% | 53.8% |

| Facilities by ADF (AIM:ADF) | 22.7% | 144.7% |

| Foresight Group Holdings (LSE:FSG) | 31.9% | 29.0% |

| B90 Holdings (AIM:B90) | 24.4% | 166.8% |

| Mortgage Advice Bureau (Holdings) (AIM:MAB1) | 19.8% | 29.6% |

| Tortilla Mexican Grill (AIM:MEX) | 27.4% | 120.4% |

We're going to check out a few of the best picks from our screener tool.

Hochschild Mining (LSE:HOC)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hochschild Mining plc is a precious metals company involved in the exploration, mining, processing, and sale of gold and silver deposits across Peru, Argentina, the United States, Canada, Brazil, and Chile with a market cap of £1.22 billion.

Operations: The company's revenue is primarily derived from its San Jose segment, which generated $266.70 million, and its Inmaculada segment, which contributed $451.91 million.

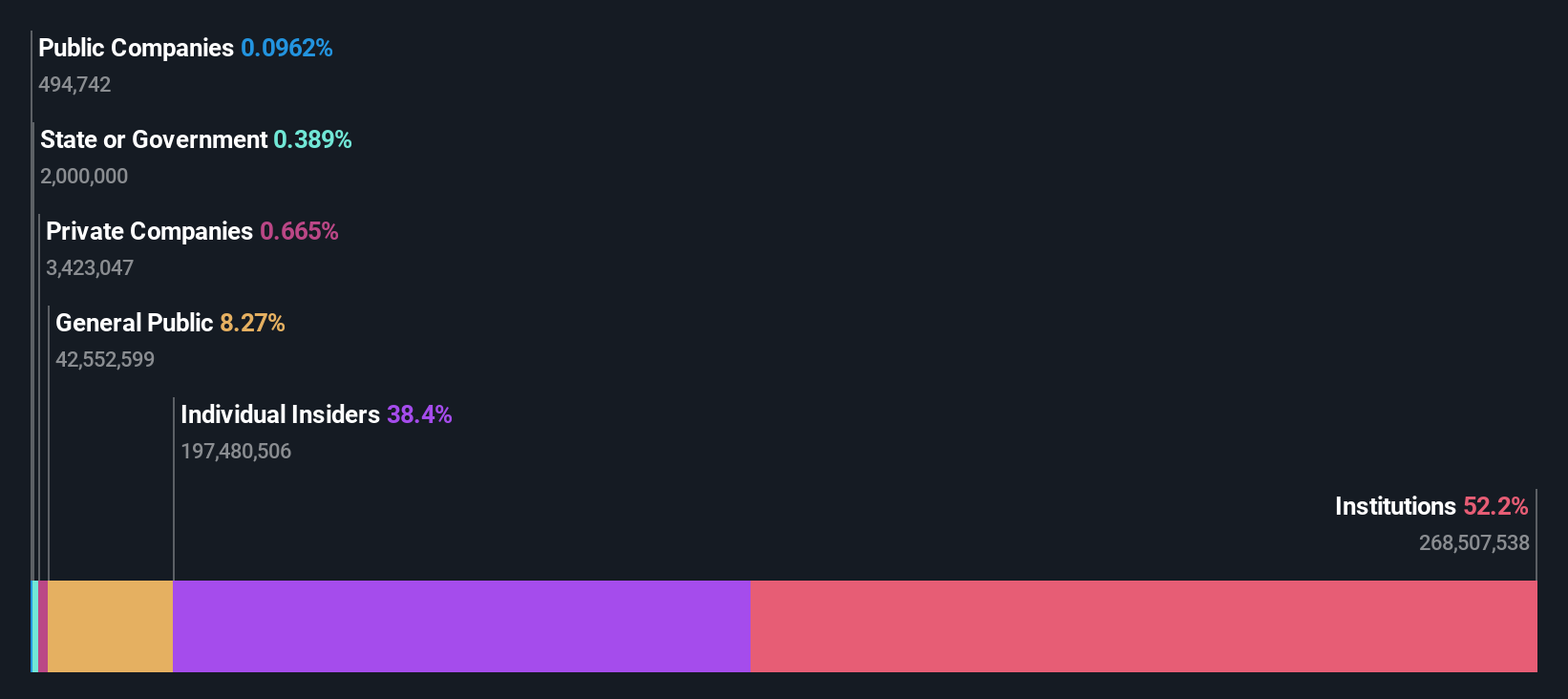

Insider Ownership: 38.4%

Hochschild Mining's earnings are forecast to grow significantly at 49.8% annually, outpacing the UK market's 14.1%. Despite high debt levels and volatile share prices, the company is trading at a substantial discount to its estimated fair value. Recent reports show improved financial performance, with net income reaching US$39.52 million for H1 2024 compared to a loss last year. However, revenue growth is expected to be moderate at 8.1% annually.

- Click here to discover the nuances of Hochschild Mining with our detailed analytical future growth report.

- In light of our recent valuation report, it seems possible that Hochschild Mining is trading beyond its estimated value.

International Workplace Group (LSE:IWG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: International Workplace Group plc, along with its subsidiaries, offers workspace solutions across the Americas, Europe, the Middle East, Africa, and the Asia Pacific with a market cap of £1.78 billion.

Operations: The company's revenue segments include $1.29 billion from the Americas, $341.30 million from the Asia Pacific, $1.69 billion from Europe, the Middle East and Africa (EMEA), and $400.56 million from Worka.

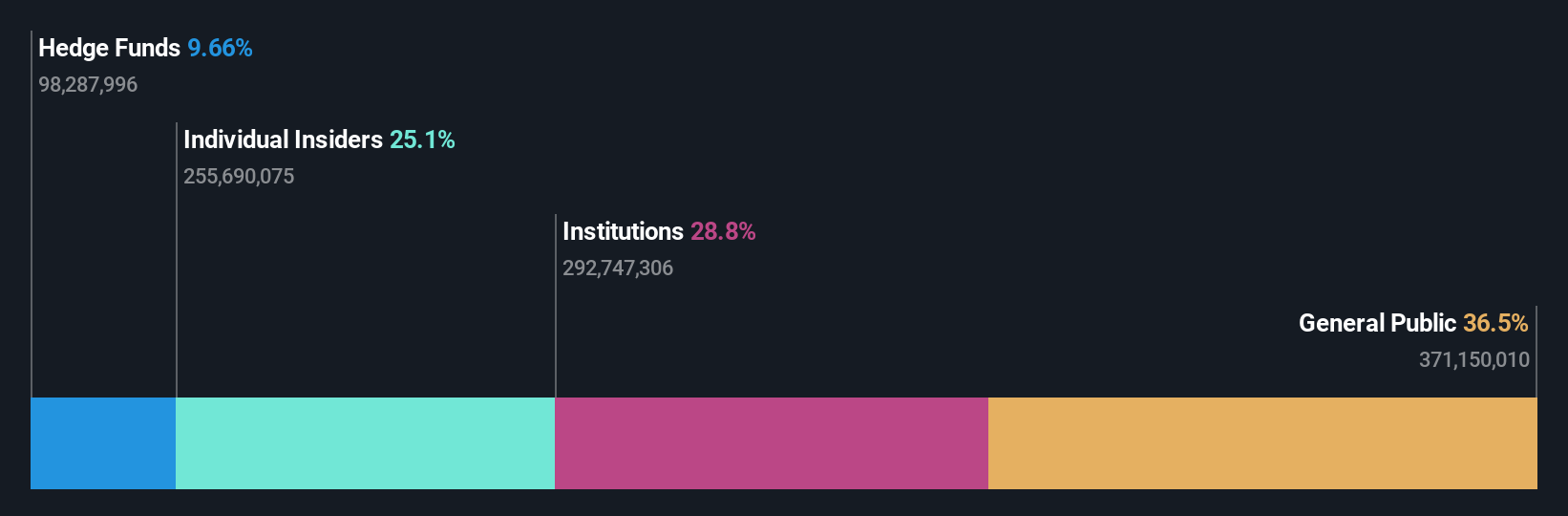

Insider Ownership: 25.2%

International Workplace Group is experiencing a positive shift, with insiders buying more shares than selling in recent months. Despite a 50% share price drop over five years, the company shows strong fundamentals and record EBITDA. Buckley Capital Management urges management to consider a US listing and share buyback program to unlock value. Recent earnings reflect improvement, with net income reaching US$16 million compared to last year's loss, supported by an 8.2% annual revenue growth forecast exceeding UK market averages.

- Dive into the specifics of International Workplace Group here with our thorough growth forecast report.

- Our valuation report unveils the possibility International Workplace Group's shares may be trading at a discount.

TBC Bank Group (LSE:TBCG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: TBC Bank Group PLC operates through its subsidiaries to offer banking, leasing, insurance, brokerage, and card processing services to corporate and individual customers in Georgia, Azerbaijan, and Uzbekistan with a market cap of £1.50 billion.

Operations: The company's revenue segments include GEL 2.13 billion from segment adjustments and GEL 236.42 million from Uzbekistan operations.

Insider Ownership: 17.6%

TBC Bank Group shows promising growth prospects with forecasted earnings and revenue growth rates of 15.3% and 18.9% annually, outpacing the UK market averages. Trading at a significant discount to its estimated fair value, it offers good relative value compared to peers. Despite an unstable dividend track record, recent financial performance is robust, with net interest income rising to GEL 862.2 million for H1 2024. The appointment of Giorgi Giguashvili as Company Secretary strengthens corporate governance capabilities.

- Click to explore a detailed breakdown of our findings in TBC Bank Group's earnings growth report.

- Our valuation report here indicates TBC Bank Group may be undervalued.

Summing It All Up

- Embark on your investment journey to our 62 Fast Growing UK Companies With High Insider Ownership selection here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com