Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalBadger Infrastructure Solutions And 2 Canadian Undervalued Small Caps With Insider Buying

The Canadian market has shown robust performance, climbing 1.6% in the past week and rising 25% over the last year, with earnings projected to grow by 16% annually. In such a dynamic environment, identifying stocks that are perceived as undervalued with insider buying can present intriguing opportunities for investors seeking potential value plays.

Top 10 Undervalued Small Caps With Insider Buying In Canada

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Trican Well Service | 7.1x | 0.9x | 20.26% | ★★★★★★ |

| VersaBank | 12.0x | 4.8x | 48.92% | ★★★★★☆ |

| Spartan Delta | 4.3x | 2.2x | 38.86% | ★★★★★☆ |

| AutoCanada | NA | 0.1x | 39.58% | ★★★★★☆ |

| Nexus Industrial REIT | 3.7x | 3.7x | 17.56% | ★★★★☆☆ |

| Rogers Sugar | 15.6x | 0.6x | 47.36% | ★★★★☆☆ |

| Primaris Real Estate Investment Trust | 13.1x | 3.5x | 43.71% | ★★★★☆☆ |

| Sagicor Financial | 1.4x | 0.3x | -46.33% | ★★★★☆☆ |

| Calfrac Well Services | 2.5x | 0.2x | 17.47% | ★★★★☆☆ |

| Vermilion Energy | NA | 1.2x | -6.59% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

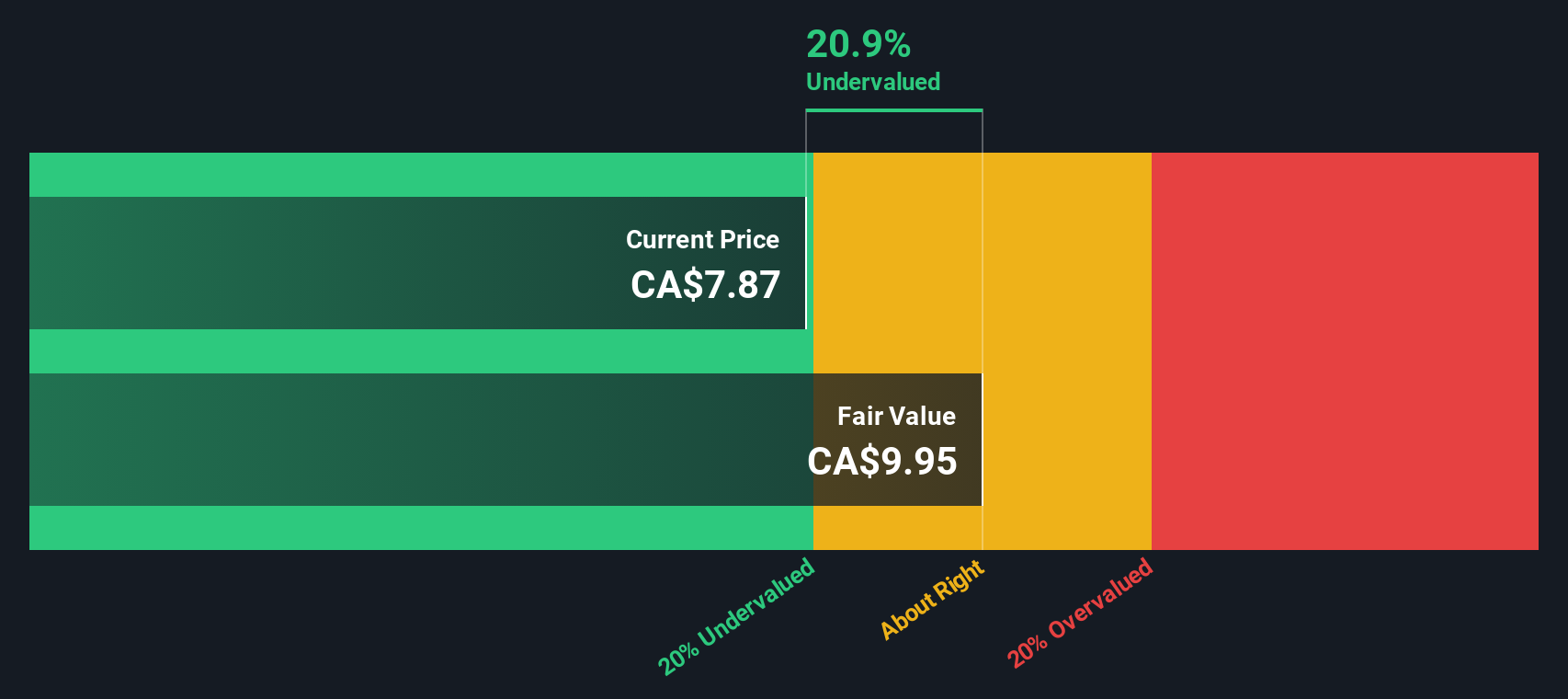

Badger Infrastructure Solutions (TSX:BDGI)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Badger Infrastructure Solutions specializes in non-destructive excavating services and has a market capitalization of approximately $1.26 billion CAD.

Operations: The company generates revenue primarily from its Non-Destructive Excavating Services, with a gross profit margin of 28.29% as of the latest period. The cost of goods sold (COGS) accounts for a significant portion of expenses, and operating expenses include notable depreciation and amortization costs.

PE: 24.6x

Badger Infrastructure Solutions, a small cap in Canada, recently showed insider confidence with share purchases. In the second quarter of 2024, sales increased to US$186.84 million from US$171.89 million year-over-year, while net income rose slightly to US$11.91 million. Despite high debt levels and reliance on external borrowing, earnings are forecasted to grow by 36% annually. The company also affirmed a quarterly dividend of C$0.18 per share for Q3 2024 and is considering a share repurchase program for future value enhancement.

Nexus Industrial REIT (TSX:NXR.UN)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Nexus Industrial REIT is a Canadian real estate investment trust focused on acquiring and managing industrial properties, with a market capitalization of CA$1.14 billion.

Operations: Nexus Industrial REIT generates revenue primarily from its investment properties, with the latest reported revenue at CA$167.21 million. The company has seen fluctuations in net income margin, reaching 1.23% as of March 2024 after a period of varied performance. Operating expenses are consistently managed below CA$9 million, contributing to a gross profit margin that recently stood at 71.56%.

PE: 3.7x

Nexus Industrial REIT, a Canadian investment trust, is attracting attention for its potential value in the small-cap sector. Despite facing challenges such as declining earnings forecasts and reliance on external borrowing, the company maintains consistent cash distributions of C$0.05333 per unit monthly. Recent insider confidence is evident with purchases made earlier this year, suggesting belief in long-term prospects. The appointment of Mary Vitug to the board adds strategic depth with her extensive capital markets experience, potentially enhancing future growth strategies.

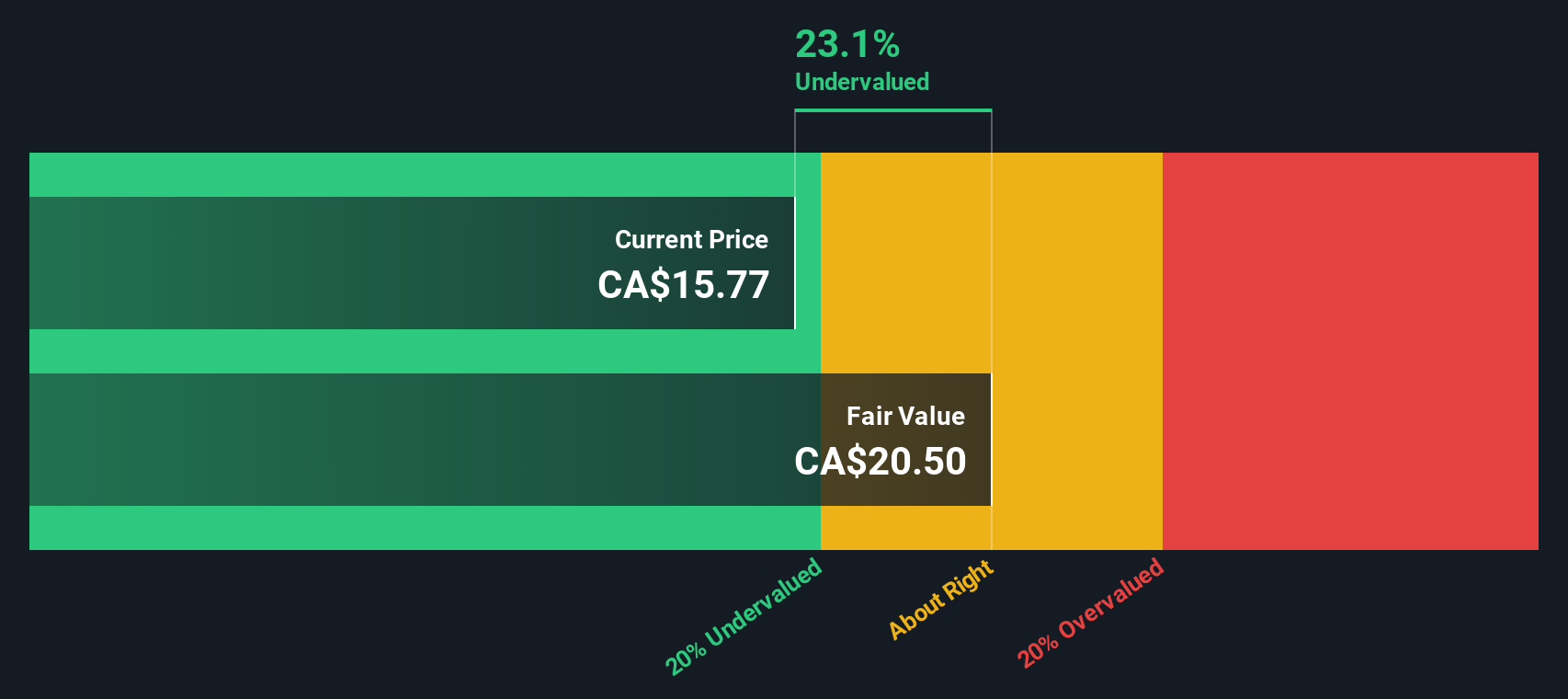

VersaBank (TSX:VBNK)

Simply Wall St Value Rating: ★★★★★☆

Overview: VersaBank is a Canadian financial institution specializing in digital banking and cybersecurity services, with a market capitalization of CA$0.35 billion.

Operations: VersaBank generates revenue primarily from its Digital Banking segment, contributing CA$105.16 million, and DRTC, which adds CA$10.75 million. The company consistently achieves a gross profit margin of 100%, indicating no cost of goods sold is reported in their financials. Operating expenses are primarily driven by general and administrative costs, with recent figures around CA$50.18 million as of October 2024.

PE: 12.0x

VersaBank, a smaller player in the Canadian market, is showing potential for growth with earnings projected to rise by 30.36% annually. Their recent financial results indicate stable performance with net interest income of C$24.94 million for Q3 2024, closely matching last year's figures. Insider confidence is evident as they have been purchasing shares over the past year, suggesting belief in future prospects. Additionally, consistent dividend announcements reinforce their commitment to shareholder returns amidst steady earnings per share performance.

- Unlock comprehensive insights into our analysis of VersaBank stock in this valuation report.

Assess VersaBank's past performance with our detailed historical performance reports.

Summing It All Up

- Dive into all 22 of the Undervalued TSX Small Caps With Insider Buying we have identified here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com