Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalUndiscovered Gems Three Promising Small Caps with Potential

As global markets navigate a landscape of record highs in major indices and modestly higher-than-expected inflation, small-cap stocks have captured the attention of investors seeking growth opportunities amid fluctuating economic indicators. In this dynamic environment, identifying promising small-cap companies involves looking for those with strong fundamentals, innovative products or services, and the ability to adapt to changing market conditions.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Petrol d.d | 42.18% | 17.56% | -0.49% | ★★★★★★ |

| NJS | NA | 4.97% | 5.30% | ★★★★★★ |

| Al Sagr Cooperative Insurance | NA | 9.35% | 37.73% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Formula Systems (1985) | 35.62% | 10.91% | 13.89% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Kappa Create | 74.42% | -0.45% | 3.62% | ★★★★★☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

Oriental Weavers Carpets Company (S.A.E) (CASE:ORWE)

Simply Wall St Value Rating: ★★★★★☆

Overview: Oriental Weavers Carpets Company (S.A.E), along with its subsidiaries, is engaged in the global manufacturing and sale of carpets, rugs, and related raw materials, with a market capitalization of EGP18.22 billion.

Operations: Oriental Weavers generates revenue primarily from the manufacturing and sale of carpets, rugs, and related raw materials. The company operates globally, contributing to its market capitalization of EGP18.22 billion.

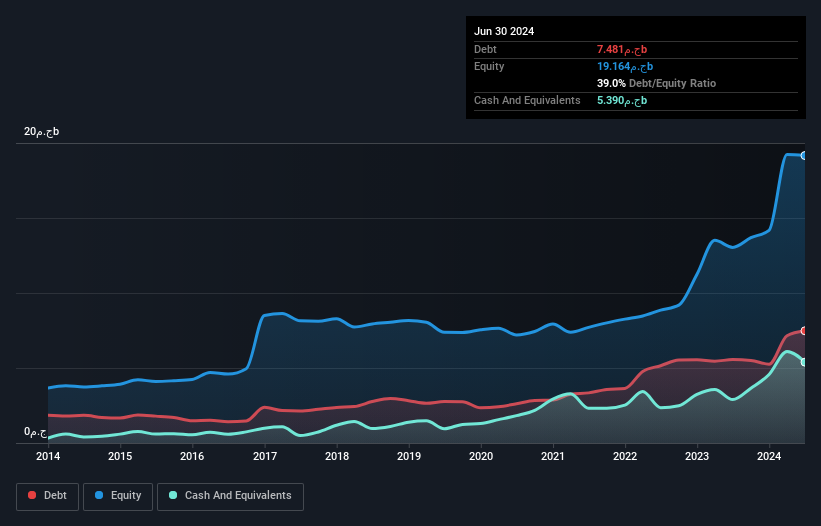

Oriental Weavers, a notable player in its industry, has shown impressive growth with earnings surging by 112.6% over the past year, outpacing the Consumer Durables sector's 6.6%. The company’s net income for Q2 2024 reached EGP 820 million from EGP 290 million last year, while its price-to-earnings ratio stands at an attractive 8.4x compared to the EG market's 8.8x. Additionally, being added to major indices like S&P Pan Arab Composite highlights its growing prominence in the market landscape.

Walaa Cooperative Insurance (SASE:8060)

Simply Wall St Value Rating: ★★★★★☆

Overview: Walaa Cooperative Insurance Company offers a range of insurance and reinsurance products and services in Saudi Arabia, with a market capitalization of SAR 1.94 billion.

Operations: The company's primary revenue streams include vehicle insurance at SAR 699.84 million and medical insurance at SAR 650.93 million, with additional contributions from protection and saving - non-linked products amounting to SAR 185.54 million.

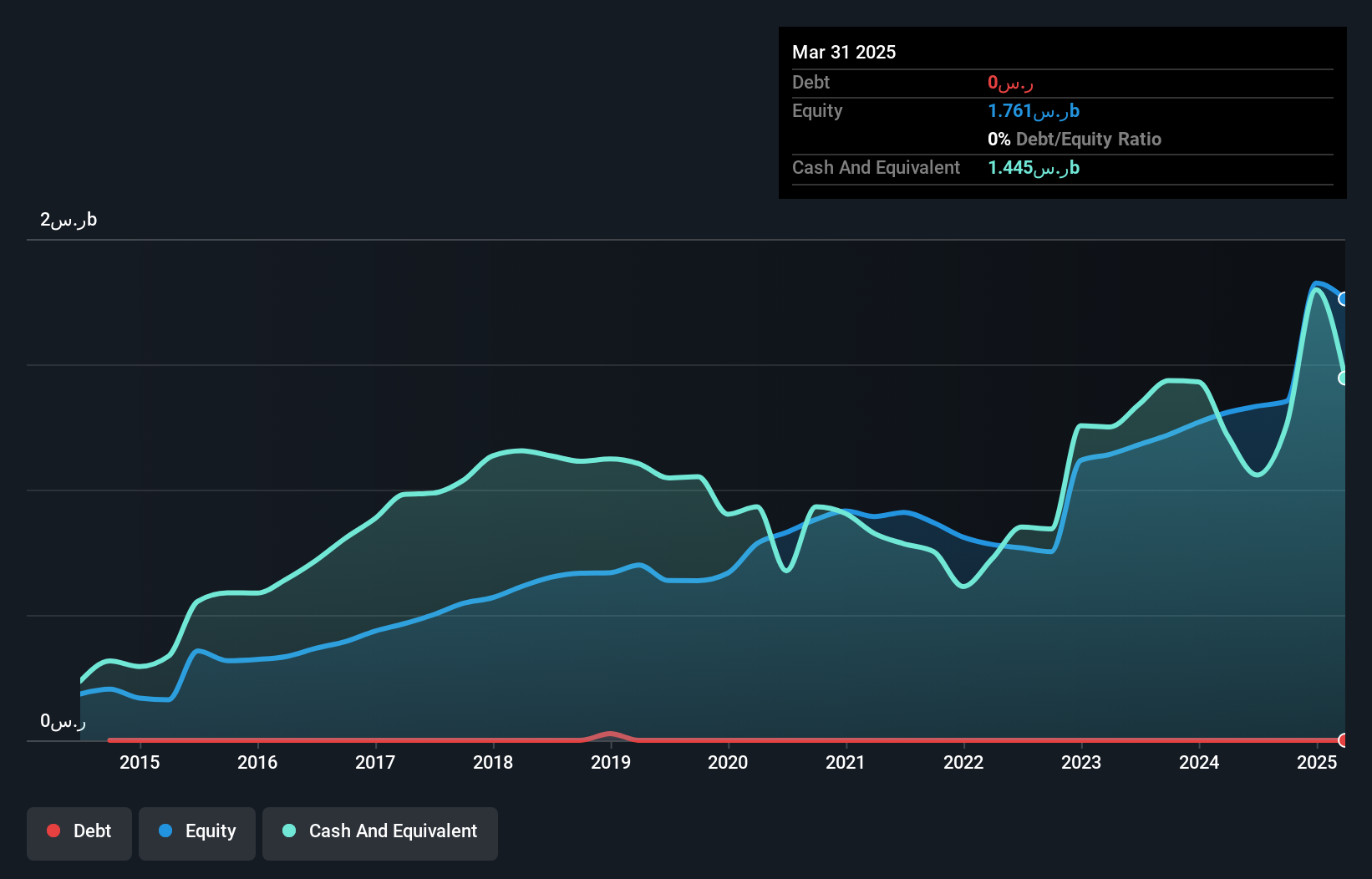

Walaa Insurance, a smaller player in the insurance sector, has demonstrated impressive earnings growth of 139% over the past year, outpacing its industry. With a price-to-earnings ratio of 13x, it appears undervalued against the SA market's 25x. Despite recent volatility in share price and a dip in quarterly net income to SAR 24 million from SAR 39 million last year, Walaa maintains high-quality earnings and remains debt-free.

Rasan Information Technology (SASE:8313)

Simply Wall St Value Rating: ★★★★★★

Overview: Rasan Information Technology Company is a FinTech firm offering digital insurance and financial services to individuals and businesses, with a market cap of SAR4.77 billion.

Operations: The company generates revenue through its digital platforms offering insurance and financial services to both individuals and businesses. It operates with a market capitalization of SAR4.77 billion, focusing on leveraging technology for its service delivery.

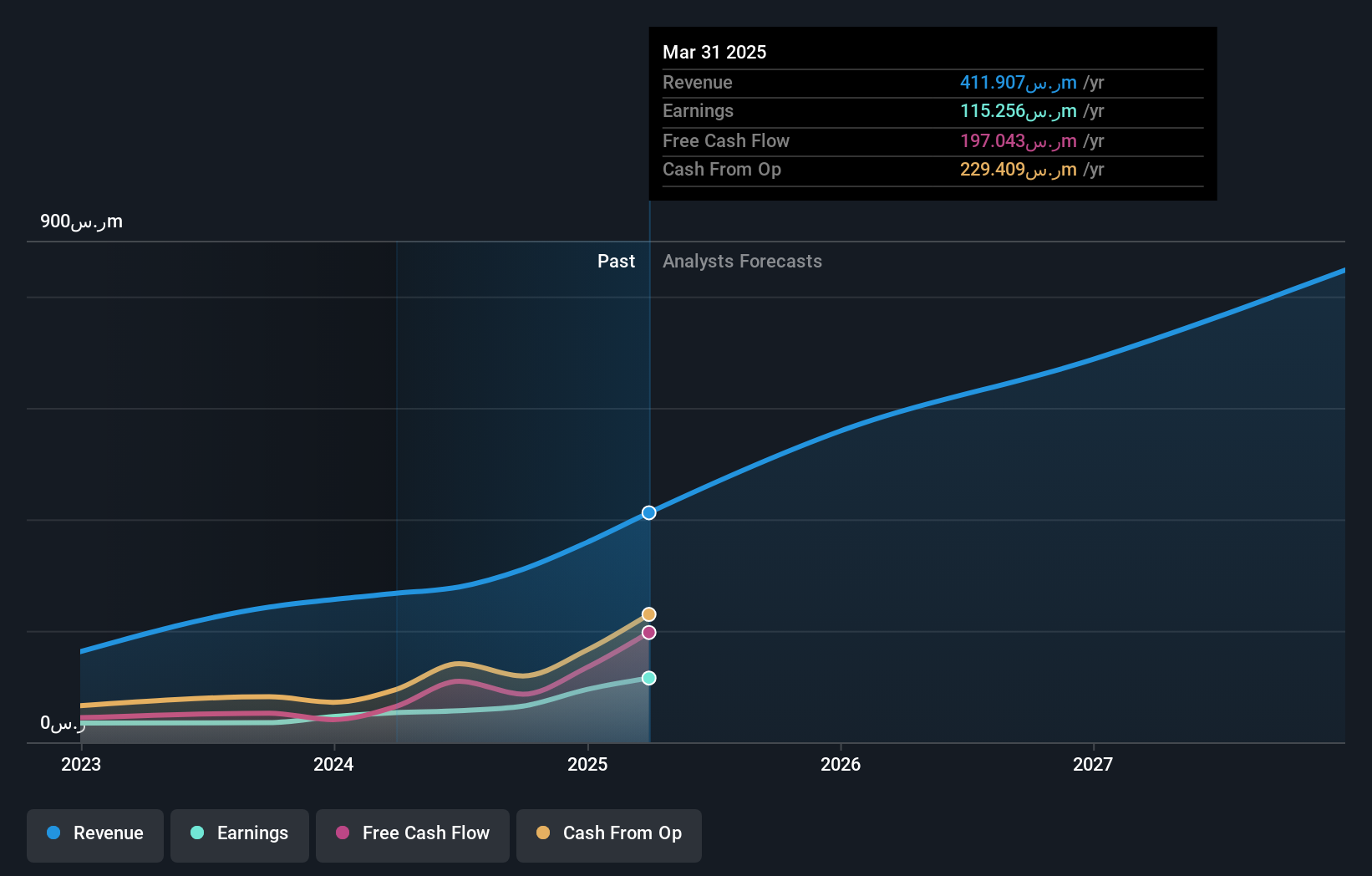

Rasan Information Technology, a small player in its sector, has shown impressive financial performance recently. The company is debt-free and boasts high-quality earnings with a notable 62% growth in the past year, outpacing industry averages. Despite its volatile share price over the last three months, Rasan's levered free cash flow reached US$109.65 million as of October 2024. With revenue projected to grow annually by 29%, prospects appear promising for future expansion.

Taking Advantage

- Unlock our comprehensive list of 4777 Undiscovered Gems With Strong Fundamentals by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com