Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalPassenger Link Branch: Retail sales of 823,000 vehicles in the passenger car market increased 20% year-on-year from October 1-13

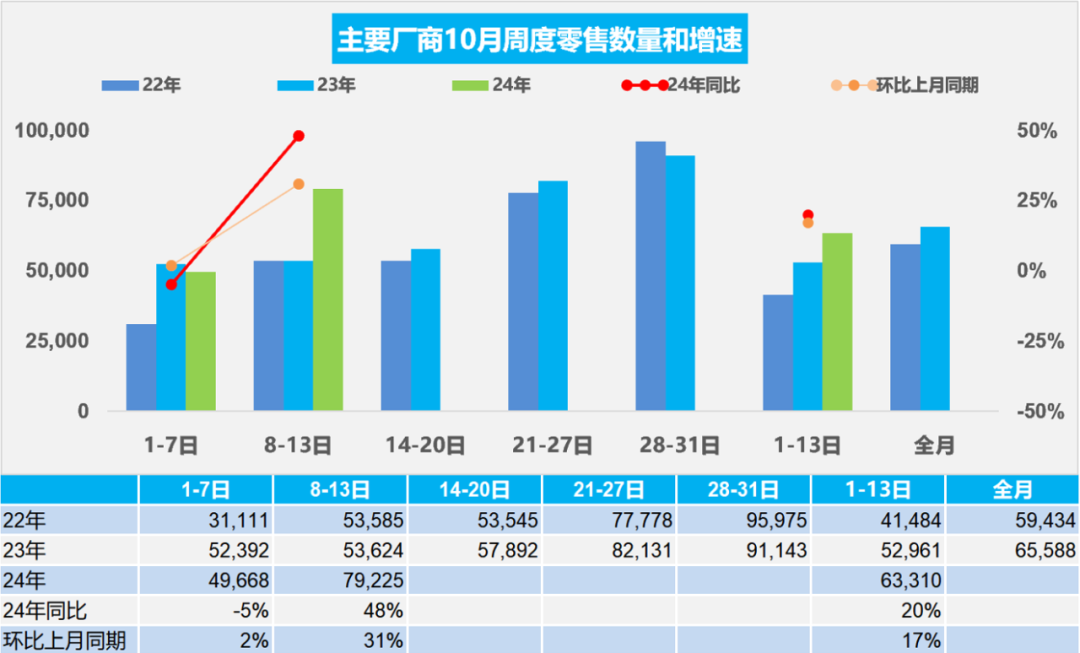

The Zhitong Finance App learned that on October 16, the Passenger Link Branch released a car market scan (October 1 to October 13, 2024). From October 1 to 13, the passenger car market retailed 823,000 vehicles, up 20% from the same period in October last year, up 17% from the same period last month. Since October 1, 397 million vehicles have been sold, up 3% year on year; from October 1 to 13, passenger car manufacturers nationwide wholesale 713,000 vehicles, up 20% from the same period last month, down 2% from the same period last month. Since this year, 19.157 million vehicles have been sold, up 4% year on year.

From October 1 to 13, the passenger car NEV market retailed 408,000 vehicles, up 64% from the same period last month, up 8% from the same period last month, with cumulative retail sales of 7.54 million units since this year, up 39% year on year. From October 1 to 13, passenger car manufacturers across the country sold 383,000 new energy vehicles, up 55% from the same period last year, up 3% from the same period last month, and a total of 8.293 million vehicles have been sold since this year, up 35% year on year.

The passenger car market sold an average of 50,000 units per day in the first week of October, down 5% from the same period in October last year, and up 2% from the same period last month.

In the second week of October, the passenger car market sold an average of 79,000 vehicles per day, up 48% from the same period in October last year, and 31% higher than the same period last month.

From October 1 to 13, the passenger car market retailed 823,000 vehicles, an increase of 20% over the same period in October last year, and an increase of 17% over the same period last month. Since this year, 16.397 million vehicles have been sold, an increase of 3% over the previous year.

Due to the different timing of the National Day holiday, retail sales in the first week of October were lower than the first week of October last year. The National Day holiday in October last year was from the end of September to October 6, so there was a difference in the first week. With the advancement of a package of national policies to promote consumption, and the recent strong growth in the stock market, the appreciation of residents' assets is conducive to the restoration of household balance sheets. Consumer confidence has increased, and consumption releases during the National Day have been outstanding. Encouraged by end-of-life renewal and trade-in subsidies, there was a good situation where car purchase consumption during the National Day grew strongly.

Recently, the domestic stock market has achieved a strong rise, driven by favorable policies. Referring to the 2014-2016 results, when the stock market suddenly soars, more capital will enter the stock market, and it is difficult for the car market to achieve a rapid rise at the same time. If the stock market continues to rise steadily over a long period of time, then the strengthening of the car market is an inevitable trend.

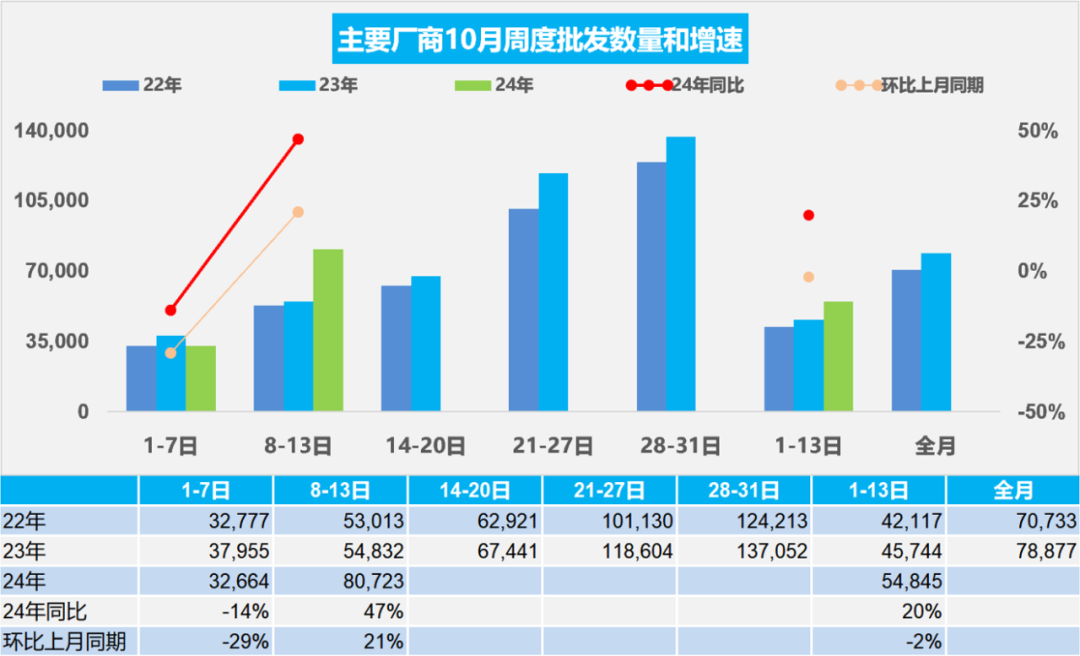

In the first week of October, passenger car manufacturers sold an average of 32,000 vehicles per day, down 14% from the same period last October and 29% from the same period last month.

In the second week of October, passenger car manufacturers sold an average of 81,000 vehicles per day, up 47% from the same period last October and 21% from the same period last month.

From October 1 to 13, passenger car manufacturers across the country wholesale 713,000 vehicles, an increase of 20% over the same period in October last year, and a decrease of 2% from the same period last month. Since this year, 19.157 million vehicles have been sold, an increase of 4% over the previous year.

Due to the different timing of the National Day holiday, the first week of October was lower than last year's. As the Federal Reserve cuts interest rates, the worldwide cycle of high interest rates comes to an end, and the market returns from economic austerity to a normal phase of low interest rates, which is conducive to the continuous recovery of consumption. The Politburo Working Conference of the Central Committee clearly proposed that promoting consumption should be combined with benefiting people's livelihood, increasing income for low- and middle-income groups, and improving the consumption structure. Car market consumption is currently the only consumption that has not been fully popularized. Raising the income of low- and middle-income earners and promoting private car consumption is the core of improving the consumption structure.

October-November should be a seasonal inventory increase period in the passenger car market. Since demand for car purchases is strong from winter to before the Spring Festival, this time has been a period of intense inventory increase over the years.

The sales volume of manufacturers in August was far lower than retail sales in the car market, resulting in a sharp inventory removal characteristic. Therefore, there was a reasonable demand to increase inventory in October, which contributed greatly to the growth of the car market.

The price war in the national passenger car market in previous years was generally about 4 points higher at the end of each year than at the end of the previous year. However, in 2024, the price war in the national passenger car market continued to be intense, and the peak promotion for new energy vehicles had already risen 7 points and solidified into price cuts. The scale of the price reduction of 195 models from January to September 2024 has already exceeded 150 models for the whole of 2023, and also greatly surpassed the total price reduction of 95 models in 2022.

In 2024, the price of plug-in hybrid models was reduced by 29 models, with an average price reduction of 24,000 yuan, an average price reduction of 13.7%. In 2024, the price of 69 pure electric models was reduced, with an average price reduction of 23,000 yuan, an average price reduction of 13.5%. In 2024, the price of 13 extended-range models was reduced, with an average price reduction of 14,000 yuan, an average price reduction of 7.6%. In 2024, the price of 13 hybrid models was reduced, with an average price reduction of 15,000 yuan, an average price reduction of 8.4%. In 2024, the price of 71 conventional fuel models was reduced, with an average price reduction of 15,000 yuan, an average price reduction of 9.3%. As the wave of price cuts gradually stabilized in the fall, the market gradually returned to the normalized competitive situation of incremental promotions.

As the country's promotional subsidies for scrapping and renewal were strengthened, the market picked up, and the driving effect on the car market was obvious. As a result, the pressure of the price war eased relatively, and the car market entered a good state of continuous strengthening at the end of the year.

According to data from the Passenger Transport Association, the price segment sales structure trend in the national passenger car market has continued to rise in recent years. The share of sales of high-end models has increased markedly, and the share of sales of medium- and low-price models has decreased. This is driving consumption upgrading, and it is also driven by the consumption upgrade of buyers. With the implementation of the national scrap renewal subsidy policy, the new energy market of less than 100,000 yuan strengthened in the third quarter of 2024, the trend of 50,000 yuan pure electric vehicles improved, and the 100,000 yuan hybrid grew rapidly, further dividing the fuel vehicle market share.

The average price of 174,000 yuan in September decreased from the average annual price of 182,000 yuan, mainly due to the increase in entry-level electric vehicles and plug-in hybrid sales in September. The structural factors behind the fall in average prices in September were obvious. The share of entry-level pure electric vehicles increased, and the share of more expensive hybrids and extenders declined, creating structural impetus. At the same time, the average sales price of original fuel vehicles also declined, and the entry-level performance of fuel vehicles also improved.

Within the price segment market, the distribution of power is relatively uneven. Among them, pure electric performance is the strongest in the market below 50,000 yuan, while extended-range electric vehicles have the strongest performance distribution in the high-end market, while hybrids are relatively strong at 200,000 to 300,000 yuan.

Traditional fuel vehicles have a relatively strong performance of 100,000 to 150,000 yuan, forming the characteristics of differentiated distribution. In particular, the distribution of hybrid power is relatively narrow, and products are mainly in the middle to high price range. Plug-in hybrids, on the other hand, are mainly mainstream models, with excellent performance in the 100,000 yuan class. The low-end market shrank more severely at the beginning of the year. This is also the impact of weak consumption on the lower end.

The number of recalls from January to September 2024 reached 137 batches of 7.38 million vehicles. There were many recalls in March, then relatively stable. An automobile product recall is a process carried out by a manufacturer of a defective automobile product to eliminate defects in its products in accordance with legal requirements and procedures. Currently, there are many recalls of foreign-funded enterprises, and the number of independent recalls is gradually increasing.

As domestic car companies' awareness has increased and the complexity of automobile products has increased, there have been more and more recalls in recent years. The recall has become a mature mechanism for resolving automobile product defects, and has contributed greatly to safeguarding the safety of the public's personal and property and the healthy development of the automobile industry in various countries. The number of new energy vehicle recalls has gradually increased this year. Apart from Tesla (TSLA.US) energy recovery software recalls on a large scale, the overall number of new energy vehicle recalls is small. There are no new trending events in traditional car recalls, and the consumer policy environment is very supportive of promoting consumption.