Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalUK Value Stocks That Might Be Priced Below Intrinsic Estimates In October 2024

The United Kingdom market has remained flat over the last week but is up 6.5% over the past year, with earnings forecasted to grow by 14% annually. In this environment, identifying stocks that may be priced below their intrinsic value can offer investors potential opportunities for growth and resilience.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| GlobalData (AIM:DATA) | £1.96 | £3.72 | 47.2% |

| S&U (LSE:SUS) | £19.20 | £36.58 | 47.5% |

| Informa (LSE:INF) | £8.27 | £16.13 | 48.7% |

| Redcentric (AIM:RCN) | £1.20 | £2.39 | 49.8% |

| Gulf Keystone Petroleum (LSE:GKP) | £1.298 | £2.46 | 47.2% |

| Loungers (AIM:LGRS) | £2.71 | £5.41 | 49.9% |

| Foxtons Group (LSE:FOXT) | £0.64 | £1.20 | 46.7% |

| SysGroup (AIM:SYS) | £0.325 | £0.65 | 49.9% |

| BATM Advanced Communications (LSE:BVC) | £0.19 | £0.37 | 48.4% |

| Genel Energy (LSE:GENL) | £0.78 | £1.51 | 48.2% |

We'll examine a selection from our screener results.

Smith & Nephew (LSE:SN.)

Overview: Smith & Nephew plc develops, manufactures, markets, and sells medical devices and services globally, with a market cap of £9.55 billion.

Operations: The company's revenue segments include Orthopaedics at $2.26 billion, Sports Medicine & ENT at $1.77 billion, and Advanced Wound Management (AWM) at $1.61 billion.

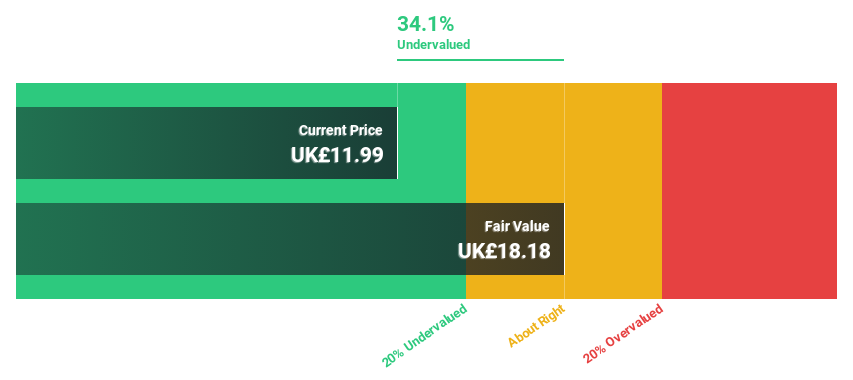

Estimated Discount To Fair Value: 33.8%

Smith & Nephew is trading at £10.85, significantly below its estimated fair value of £16.39, suggesting it may be undervalued based on cash flows. Despite high debt levels and a dividend not well covered by earnings or free cash flows, the company's strategic collaborations like the recent co-marketing agreement with JointVue for 3D surgery planning technology could enhance operational efficiency and patient outcomes. Earnings are forecast to grow annually by 22.75%, outpacing the UK market's growth rate.

- Upon reviewing our latest growth report, Smith & Nephew's projected financial performance appears quite optimistic.

- Get an in-depth perspective on Smith & Nephew's balance sheet by reading our health report here.

Senior (LSE:SNR)

Overview: Senior plc designs, manufactures, and sells high-technology components and systems for major original equipment manufacturers in aerospace, defense, land vehicle, and power and energy markets globally; it has a market cap of £551.24 million.

Operations: The company's revenue is derived from two main segments: Aerospace, contributing £651.10 million, and Flexonics, accounting for £333 million.

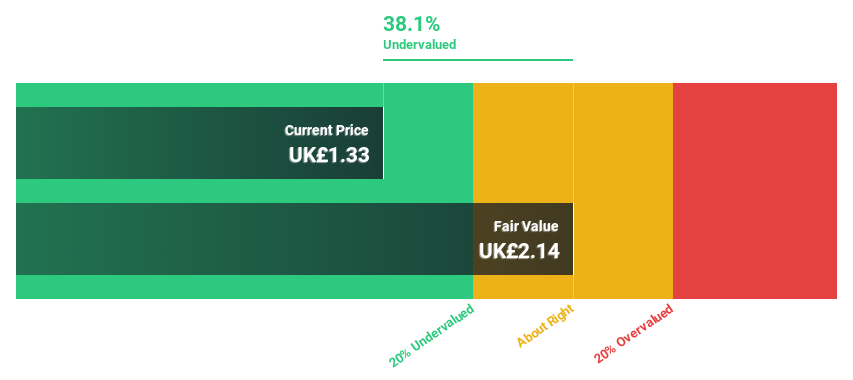

Estimated Discount To Fair Value: 37.3%

Senior plc is trading at £1.35, well below its estimated fair value of £2.15, indicating potential undervaluation based on cash flows. Despite a forecasted low return on equity of 9% in three years, earnings are expected to grow significantly at 31.5% annually, outpacing the UK market's growth rate. Recent developments include securing contracts with Deutsche Aircraft and Rolls-Royce, which may bolster future revenue streams despite current challenges in net income performance.

- Our expertly prepared growth report on Senior implies its future financial outlook may be stronger than recent results.

- Click to explore a detailed breakdown of our findings in Senior's balance sheet health report.

Savills (LSE:SVS)

Overview: Savills plc, along with its subsidiaries, provides real estate services across the United Kingdom, Continental Europe, Asia Pacific, Africa, North America, and the Middle East with a market cap of £1.54 billion.

Operations: The company's revenue segments consist of Consultancy (£464.80 million), Transaction Advisory (£803.60 million), Investment Management (£100.50 million), and Property and Facilities Management (£920.90 million).

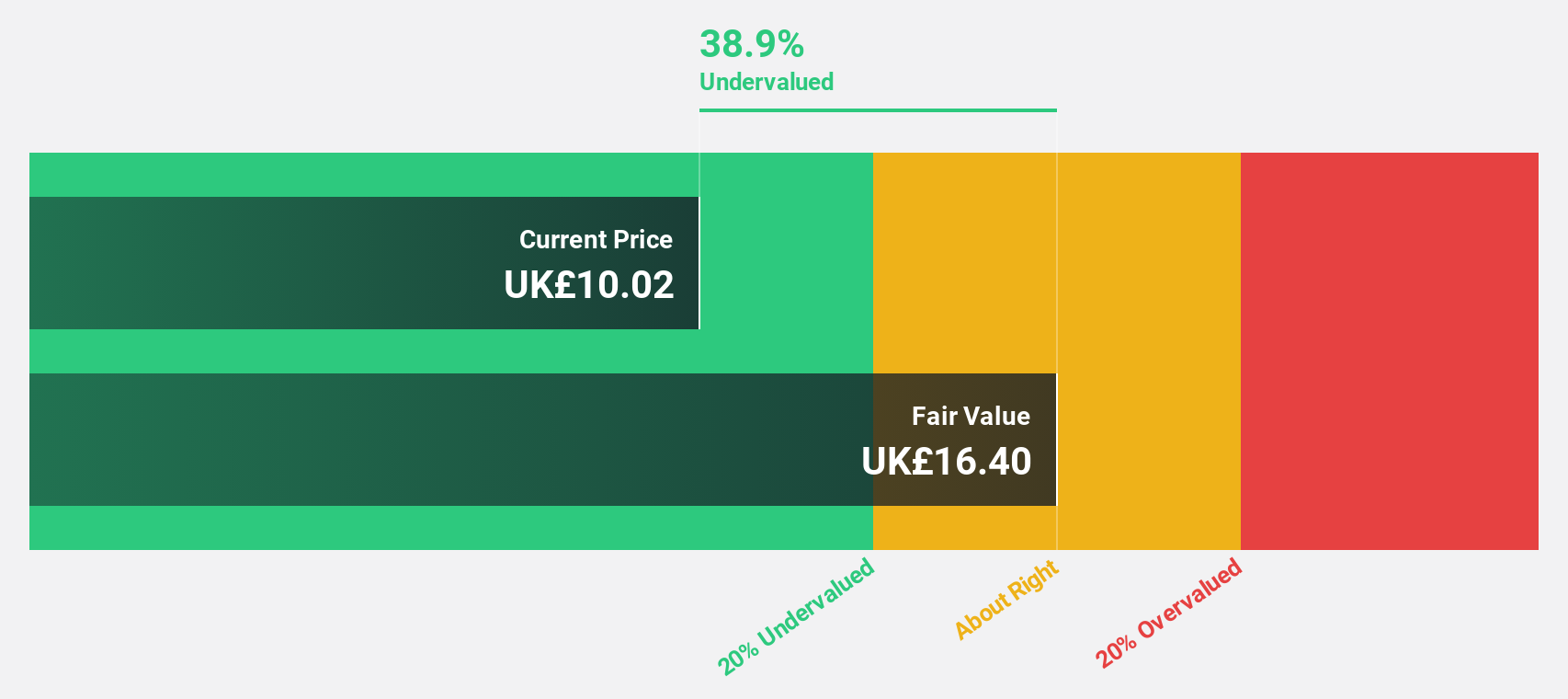

Estimated Discount To Fair Value: 24.6%

Savills is trading at £11.4, significantly below its estimated fair value of £15.12, suggesting it may be undervalued based on cash flows. Earnings are projected to grow at 33.3% annually, surpassing the UK market's growth rate. However, profit margins have declined from 3.8% to 1.9%. Recent strategic moves include appointing Toby Hall to enhance their commercial agency services in the Middle East amidst regional growth opportunities, potentially impacting future revenue positively.

- Our earnings growth report unveils the potential for significant increases in Savills' future results.

- Dive into the specifics of Savills here with our thorough financial health report.

Turning Ideas Into Actions

- Unlock our comprehensive list of 59 Undervalued UK Stocks Based On Cash Flows by clicking here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com