Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalExploring 3 Promising Swedish Small Caps With Strong Potential

As European markets show signs of optimism with the pan-European STOXX Europe 600 Index rising amid potential interest rate cuts, investors are increasingly looking towards small-cap opportunities in regions like Sweden. In this context, identifying promising small-cap stocks involves assessing companies that demonstrate resilience and adaptability to shifting economic conditions, positioning them as potential hidden gems in a dynamic market landscape.

Top 10 Undiscovered Gems With Strong Fundamentals In Sweden

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Softronic | NA | 3.58% | 7.41% | ★★★★★★ |

| Bahnhof | NA | 9.02% | 15.02% | ★★★★★★ |

| Duni | 29.33% | 10.78% | 22.98% | ★★★★★★ |

| Firefly | NA | 16.04% | 32.29% | ★★★★★★ |

| AB Traction | NA | 5.38% | 5.19% | ★★★★★★ |

| AQ Group | 7.30% | 14.89% | 22.26% | ★★★★★★ |

| Byggmästare Anders J Ahlström Holding | NA | 30.31% | -9.00% | ★★★★★★ |

| Svolder | NA | -22.68% | -24.17% | ★★★★★★ |

| Linc | NA | 56.01% | 0.54% | ★★★★★★ |

| Solid Försäkringsaktiebolag | NA | 7.64% | 28.44% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

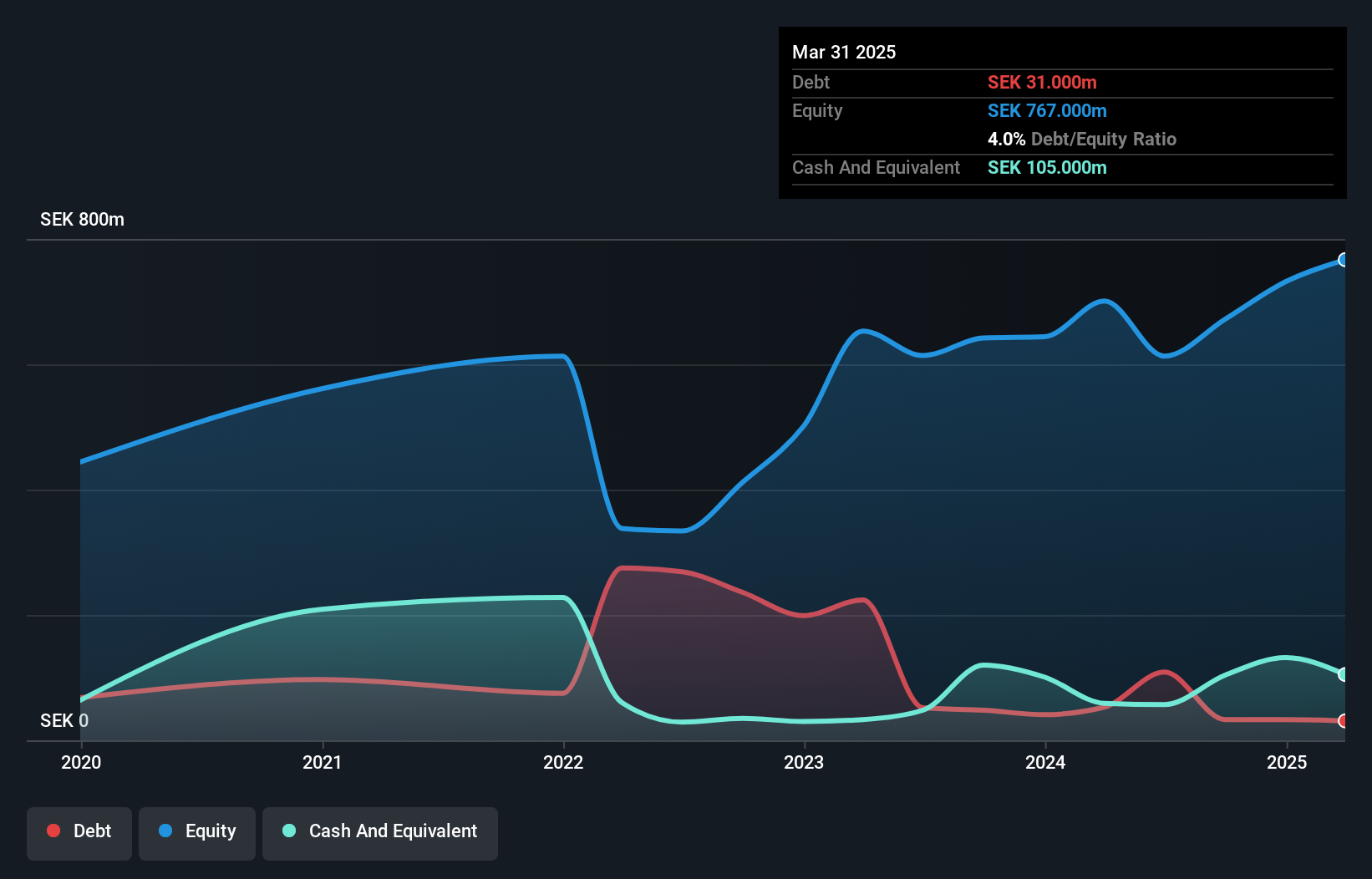

AQ Group (OM:AQ)

Simply Wall St Value Rating: ★★★★★★

Overview: AQ Group AB (publ) is a company that manufactures and sells components and systems for industrial customers across Sweden, other European countries, and internationally, with a market cap of SEK11.71 billion.

Operations: AQ Group generates revenue primarily from its Component segment, which accounts for SEK7.87 billion, and the System segment contributing SEK1.78 billion. The company's focus on these segments highlights its strategic revenue streams within the industrial sector.

AQ Group, a small player in Sweden's market, has caught attention with its robust financial health and strategic growth. The company is trading at 87.6% below its estimated fair value, indicating potential undervaluation. Over the past five years, AQ's debt to equity ratio impressively decreased from 36.3% to 7.3%, while earnings surged by 19%. Recently added to the S&P Global BMI Index, AQ showcases high-quality earnings and strong industry performance with EBIT covering interest payments by 32 times.

- Navigate through the intricacies of AQ Group with our comprehensive health report here.

Explore historical data to track AQ Group's performance over time in our Past section.

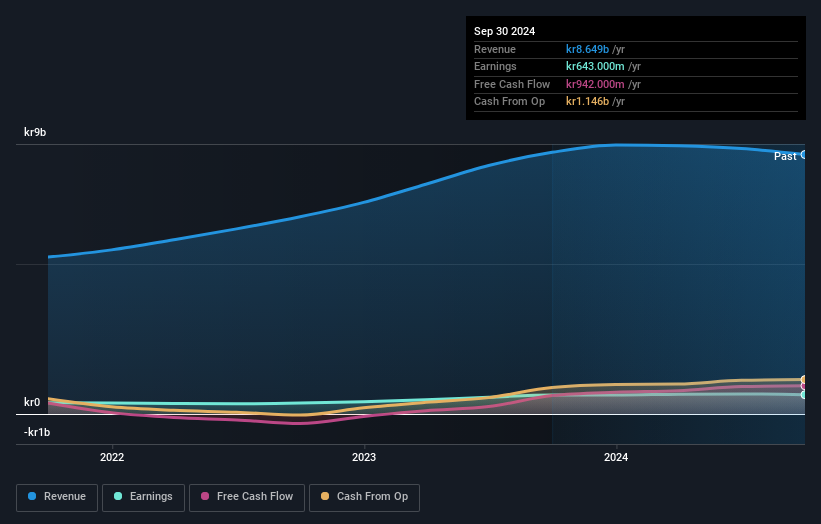

engcon (OM:ENGCON B)

Simply Wall St Value Rating: ★★★★★☆

Overview: Engcon AB (publ) specializes in the design, production, and sale of excavator tools across various international markets including Europe, the Americas, and Asia-Pacific regions, with a market cap of approximately SEK16.91 billion.

Operations: Engcon AB generates revenue primarily from its Construction Machinery & Equipment segment, amounting to SEK1.54 billion. The company's financial performance is reflected in its gross profit margin, which showcases notable trends over recent periods.

Engcon, a niche player in the machinery sector, has faced challenges with earnings growth, showing a negative 60.6% over the past year despite high-quality earnings and satisfactory debt levels with a net debt to equity ratio of 8.5%. The company's interest payments are well covered by EBIT at 20.4 times, indicating solid financial management. Recent reports highlighted declining sales from SEK 508 million to SEK 450 million in Q2, impacting net income which fell from SEK 83 million to SEK 55 million.

- Click to explore a detailed breakdown of our findings in engcon's health report.

Examine engcon's past performance report to understand how it has performed in the past.

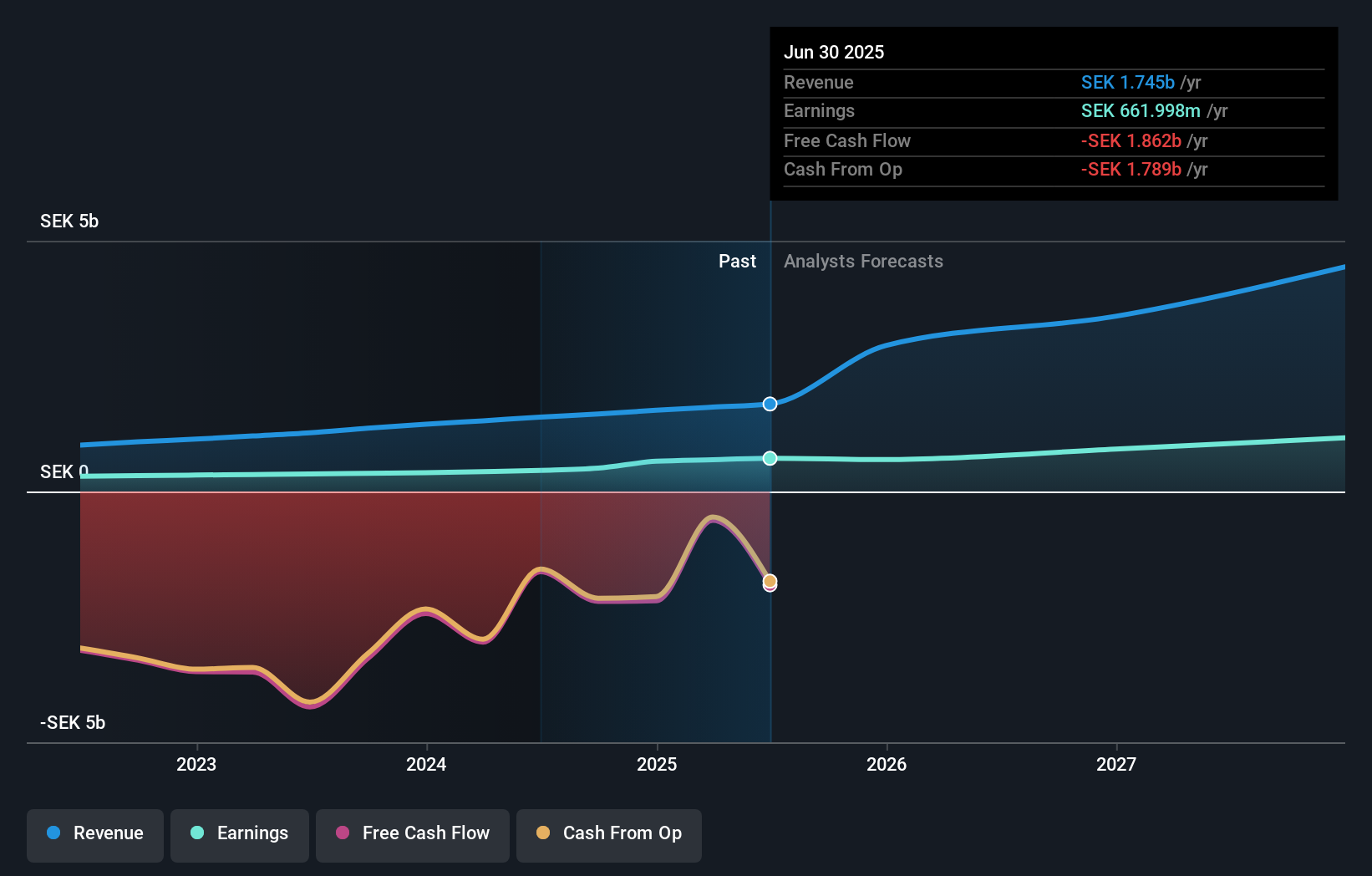

TF Bank (OM:TFBANK)

Simply Wall St Value Rating: ★★★★☆☆

Overview: TF Bank AB (publ) is a digital bank offering consumer banking services and e-commerce solutions via its proprietary IT platform, with a market cap of SEK6.51 billion.

Operations: TF Bank AB (publ) generates revenue primarily from three segments: Credit Cards (SEK511.24 million), Consumer Lending (SEK607.24 million), and Ecommerce Solutions excluding Credit Cards (SEK363.28 million).

TF Bank, with assets totaling SEK24.1 billion and equity of SEK2.4 billion, navigates the financial landscape with a focus on low-risk funding—95% from customer deposits. Despite trading 50.9% below estimated fair value, it grapples with high bad loans at 10.6%, offset by a modest allowance of 62%. Recent earnings grew by 21.3%, outpacing the industry average of 11.8%, highlighting its potential amidst ongoing challenges in non-performing loans management and free cash flow deficits.

- Click here and access our complete health analysis report to understand the dynamics of TF Bank.

Gain insights into TF Bank's historical performance by reviewing our past performance report.

Key Takeaways

- Unlock more gems! Our Swedish Undiscovered Gems With Strong Fundamentals screener has unearthed 51 more companies for you to explore.Click here to unveil our expertly curated list of 54 Swedish Undiscovered Gems With Strong Fundamentals.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com