Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalHigh Insider Ownership Growth Stocks On Indian Exchange October 2024

The Indian market has experienced a flat performance over the last week but has seen an impressive 40% increase over the past year, with earnings forecasted to grow by 17% annually. In this context, growth companies with high insider ownership can be particularly appealing as they often indicate strong internal confidence and alignment of interests with shareholders.

Top 10 Growth Companies With High Insider Ownership In India

| Name | Insider Ownership | Earnings Growth |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 34% |

| Kirloskar Pneumatic (BSE:505283) | 30.3% | 30.1% |

| Jupiter Wagons (NSEI:JWL) | 10.8% | 27.4% |

| Dixon Technologies (India) (NSEI:DIXON) | 24.6% | 30.6% |

| Paisalo Digital (BSE:532900) | 16.3% | 24.8% |

| Apollo Hospitals Enterprise (NSEI:APOLLOHOSP) | 10.4% | 32.3% |

| Rajratan Global Wire (BSE:517522) | 18.3% | 35.8% |

| KEI Industries (BSE:517569) | 19.2% | 21.9% |

| Pricol (NSEI:PRICOLLTD) | 25.5% | 24% |

| Aether Industries (NSEI:AETHER) | 31.1% | 45.8% |

Here we highlight a subset of our preferred stocks from the screener.

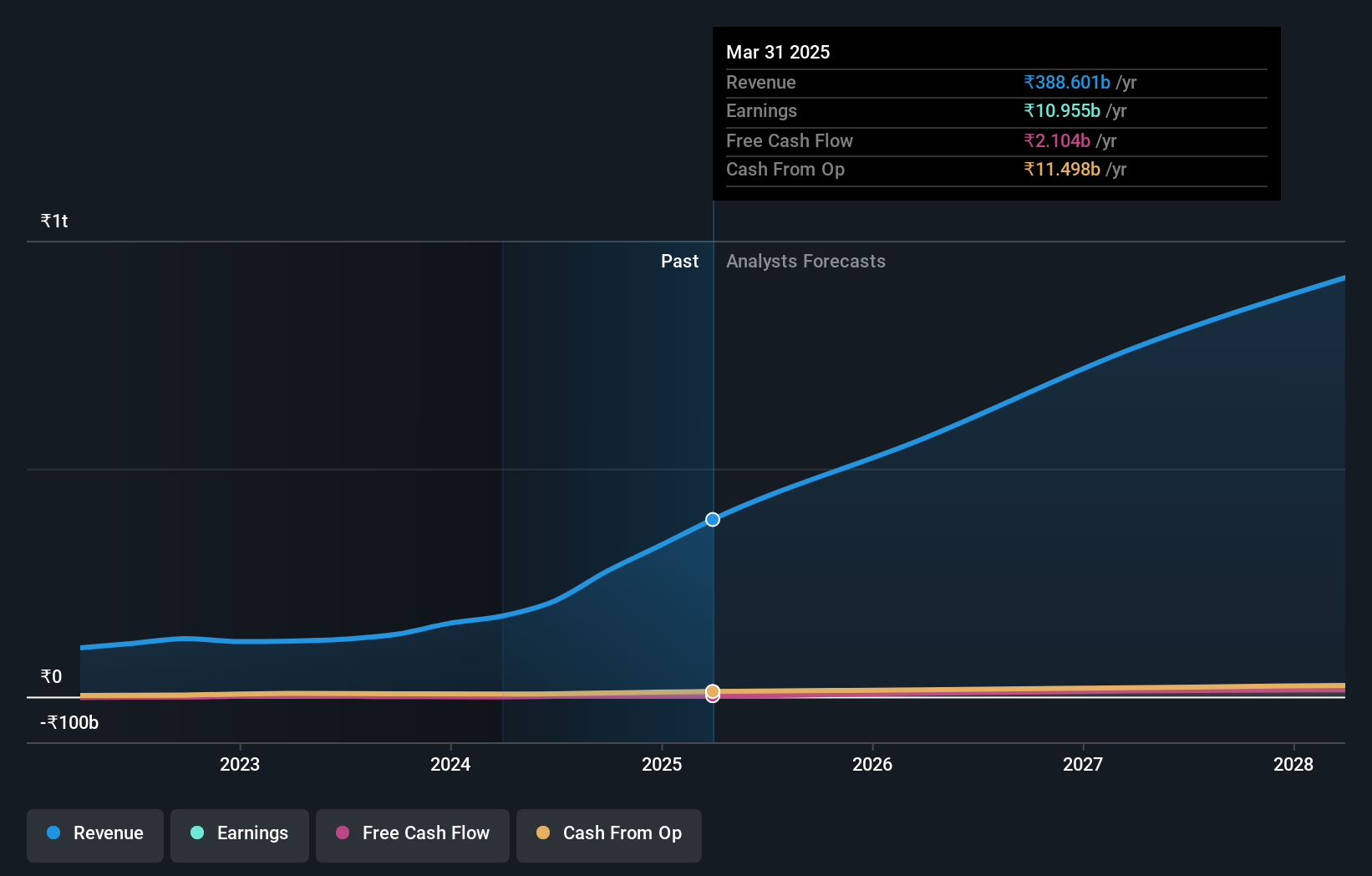

Dixon Technologies (India) (NSEI:DIXON)

Simply Wall St Growth Rating: ★★★★★★

Overview: Dixon Technologies (India) Limited provides electronic manufacturing services both in India and internationally, with a market cap of ₹921.75 billion.

Operations: The company's revenue segments include Home Appliances at ₹12.51 billion, Lighting Products at ₹7.92 billion, Mobile & EMS Division at ₹143.16 billion, and Consumer Electronics & Appliances at ₹41.21 billion.

Insider Ownership: 24.6%

Dixon Technologies (India) shows strong growth potential with forecasted revenue and earnings growth rates of 23.7% and 30.6% per year, respectively, outpacing the Indian market averages. The company reported significant earnings increases for the first quarter of 2024, with net income rising to ₹1.34 billion from ₹688.2 million a year ago. Despite no recent insider trading activity, Dixon's high insider ownership aligns management interests with shareholders, supporting its growth trajectory amidst strategic leadership changes and robust financial performance.

- Get an in-depth perspective on Dixon Technologies (India)'s performance by reading our analyst estimates report here.

- The analysis detailed in our Dixon Technologies (India) valuation report hints at an inflated share price compared to its estimated value.

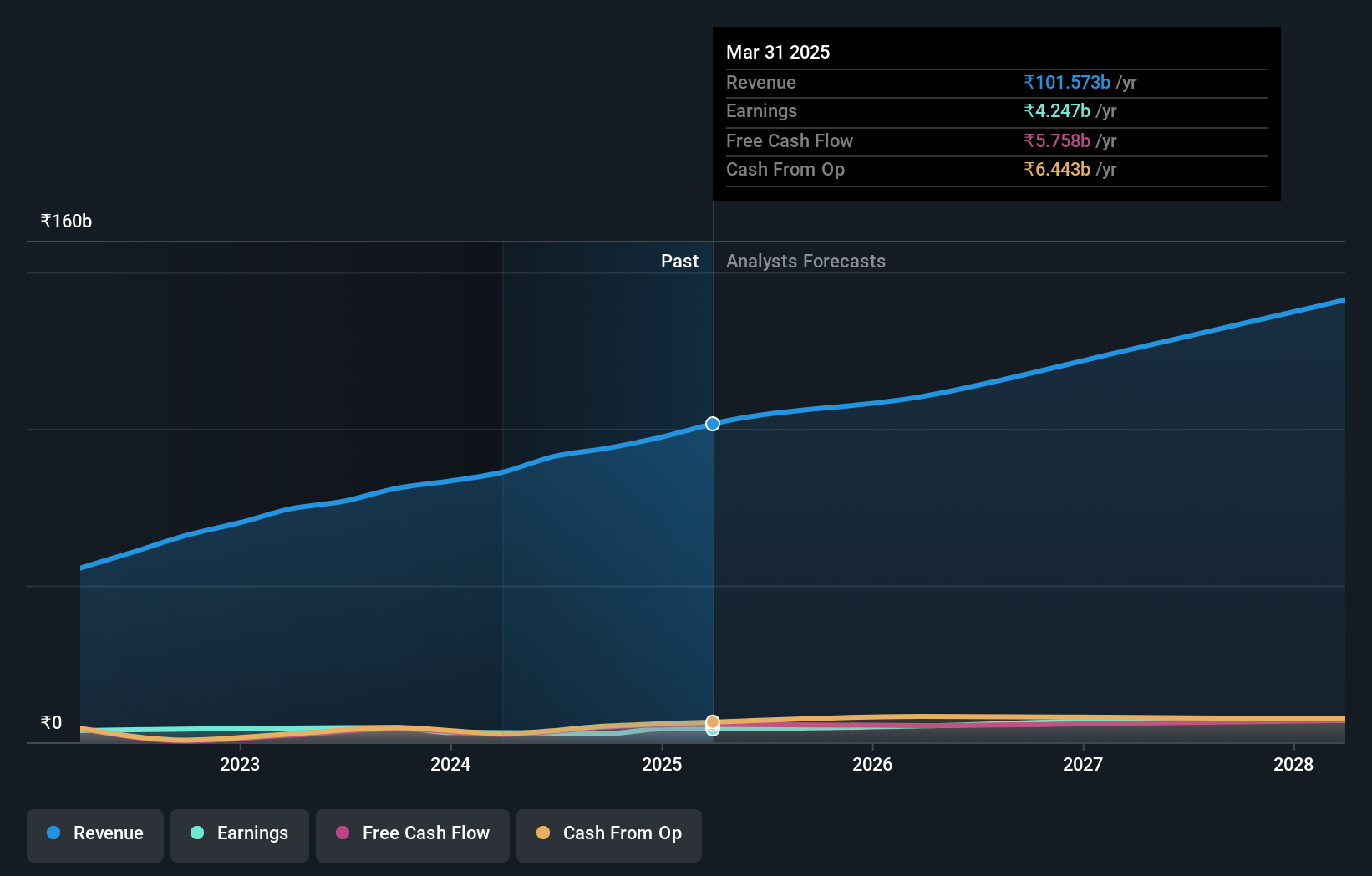

Sonata Software (NSEI:SONATSOFTW)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Sonata Software Limited, along with its subsidiaries, offers information technology services and solutions across the United States, Europe, the Middle East, Asia, India, and Australia with a market cap of ₹172.46 billion.

Operations: Sonata Software's revenue segments include providing IT services and solutions across various regions, including the United States, Europe, the Middle East, Asia, India, and Australia.

Insider Ownership: 37.7%

Sonata Software is poised for growth with forecasted earnings and revenue growth rates of 29.6% and 13.4% per year, respectively, surpassing Indian market averages. Despite no substantial insider buying recently, the company's strategic partnerships, such as with iNube for insurance solutions in the US and UK, enhance its market position. However, challenges include declining profit margins from 6% to 3.2%, highlighting operational efficiency needs amidst its ambitious expansion efforts in healthcare IT outsourcing.

- Take a closer look at Sonata Software's potential here in our earnings growth report.

- The valuation report we've compiled suggests that Sonata Software's current price could be inflated.

Varun Beverages (NSEI:VBL)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Varun Beverages Limited, along with its subsidiaries, operates as a franchisee for PepsiCo's carbonated and non-carbonated beverages, with a market cap of ₹1.98 trillion.

Operations: The company's revenue from manufacturing and selling beverages amounts to ₹180.52 billion.

Insider Ownership: 36.2%

Varun Beverages is set for robust growth, with earnings projected to increase by 22.38% annually, outpacing the Indian market. The company plans to raise ₹75 billion through a Qualified Institutional Placement to fund expansions and repay debt, enhancing its financial position despite high debt levels. Recent investments include a $50 million Pepsi production facility in the DRC, demonstrating strategic international expansion efforts that align with its growth trajectory and insider ownership dynamics.

- Navigate through the intricacies of Varun Beverages with our comprehensive analyst estimates report here.

- In light of our recent valuation report, it seems possible that Varun Beverages is trading beyond its estimated value.

Key Takeaways

- Click through to start exploring the rest of the 87 Fast Growing Indian Companies With High Insider Ownership now.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

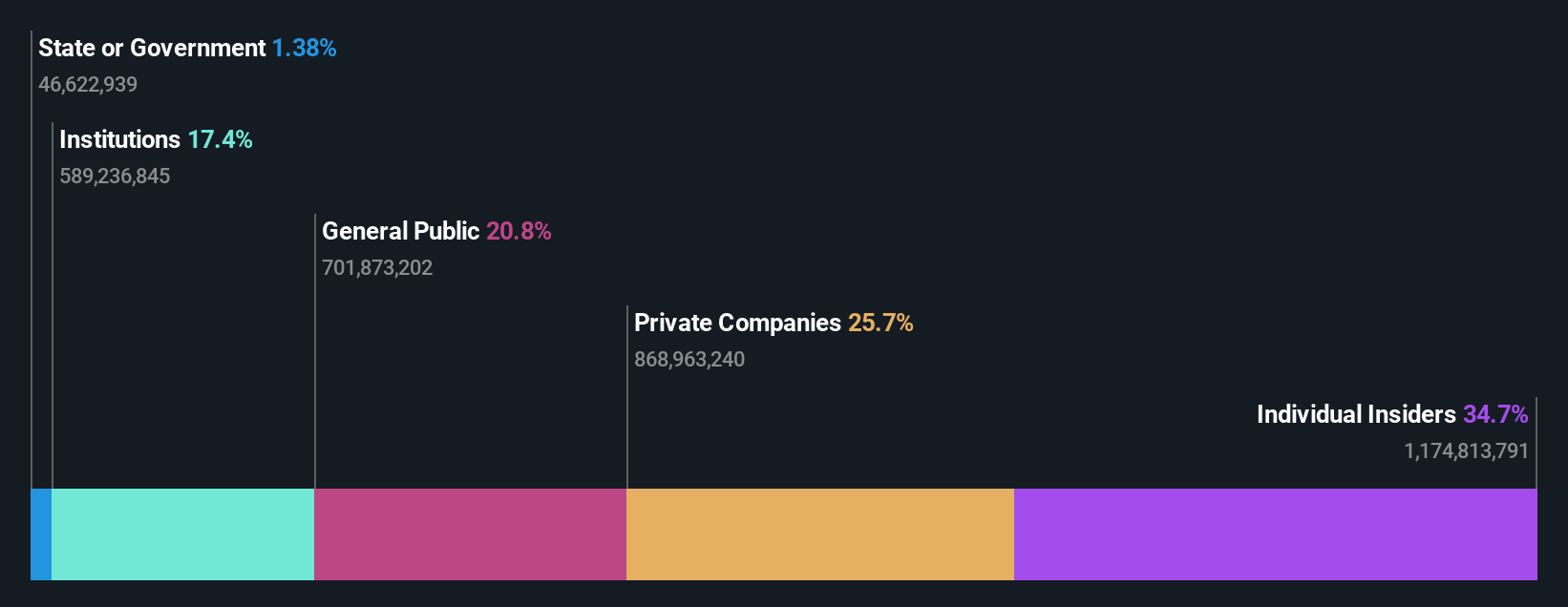

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com