Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalJapan Investment Adviser (TSE:7172) Is Due To Pay A Dividend Of ¥12.00

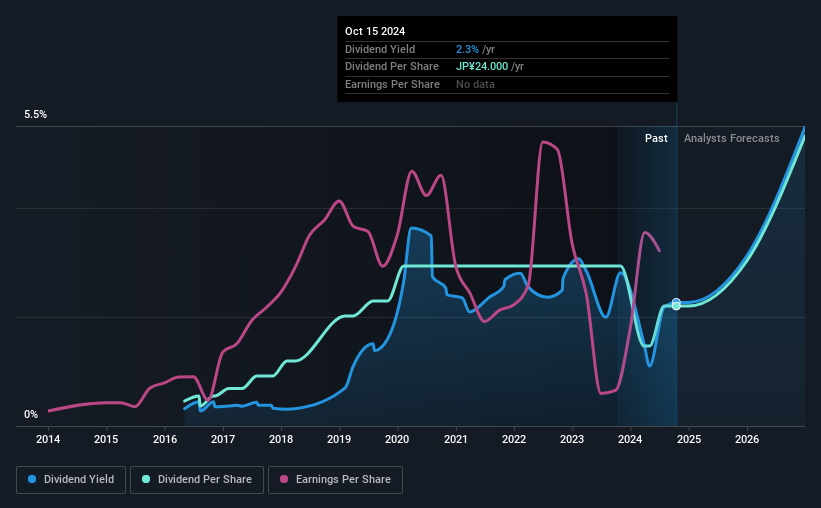

The board of Japan Investment Adviser Co., Ltd. (TSE:7172) has announced that it will pay a dividend of ¥12.00 per share on the 27th of March. This means that the annual payment is 2.3% of the current stock price, which is lower than what the rest of the industry is paying.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. Japan Investment Adviser's stock price has reduced by 38% in the last 3 months, which is not ideal for investors and can explain a sharp increase in the dividend yield.

Check out our latest analysis for Japan Investment Adviser

Japan Investment Adviser's Projected Earnings Seem Likely To Cover Future Distributions

Even a low dividend yield can be attractive if it is sustained for years on end. Japan Investment Adviser is quite easily earning enough to cover the dividend, however it is being let down by weak cash flows. With the company not bringing in any cash, paying out to shareholders is bound to become difficult at some point.

Looking forward, earnings per share is forecast to rise by 31.7% over the next year. If the dividend continues along recent trends, we estimate the payout ratio will be 21%, which is in the range that makes us comfortable with the sustainability of the dividend.

Japan Investment Adviser's Dividend Has Lacked Consistency

Even in its relatively short history, the company has reduced the dividend at least once. If the company cuts once, it definitely isn't argument against the possibility of it cutting in the future. The dividend has gone from an annual total of ¥5.00 in 2016 to the most recent total annual payment of ¥24.00. This implies that the company grew its distributions at a yearly rate of about 22% over that duration. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

Dividend Growth Is Doubtful

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. In the last five years, Japan Investment Adviser's earnings per share has shrunk at approximately 7.5% per annum. If earnings continue declining, the company may have to make the difficult choice of reducing the dividend or even stopping it completely - the opposite of dividend growth. However, the next year is actually looking up, with earnings set to rise. We would just wait until it becomes a pattern before getting too excited.

An additional note is that the company has been raising capital by issuing stock equal to 100% of shares outstanding in the last 12 months. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

The Dividend Could Prove To Be Unreliable

Overall, it's not great to see that the dividend has been cut, but this might be explained by the payments being a bit high previously. While Japan Investment Adviser is earning enough to cover the payments, the cash flows are lacking. We would be a touch cautious of relying on this stock primarily for the dividend income.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. At the same time, there are other factors our readers should be conscious of before pouring capital into a stock. To that end, Japan Investment Adviser has 4 warning signs (and 3 which shouldn't be ignored) we think you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.