Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalHigh Growth Tech Stocks in South Korea for October 2024

The South Korean market has been experiencing dynamic shifts, with particular attention on the technology sector as it navigates broader economic trends and investor sentiment. In this context, identifying high-growth tech stocks involves evaluating companies that demonstrate resilience and innovation in response to both local and global market conditions.

Top 10 High Growth Tech Companies In South Korea

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| IMLtd | 21.80% | 111.43% | ★★★★★★ |

| Seojin SystemLtd | 33.39% | 49.13% | ★★★★★★ |

| Bioneer | 23.53% | 97.58% | ★★★★★★ |

| NEXON Games | 29.64% | 66.98% | ★★★★★★ |

| FLITTO | 32.60% | 106.82% | ★★★★★★ |

| ALTEOGEN | 64.22% | 99.46% | ★★★★★★ |

| Park Systems | 23.21% | 34.63% | ★★★★★★ |

| Devsisters | 29.08% | 63.02% | ★★★★★★ |

| AmosenseLtd | 24.04% | 71.97% | ★★★★★★ |

| UTI | 114.97% | 134.60% | ★★★★★★ |

Click here to see the full list of 48 stocks from our KRX High Growth Tech and AI Stocks screener.

We're going to check out a few of the best picks from our screener tool.

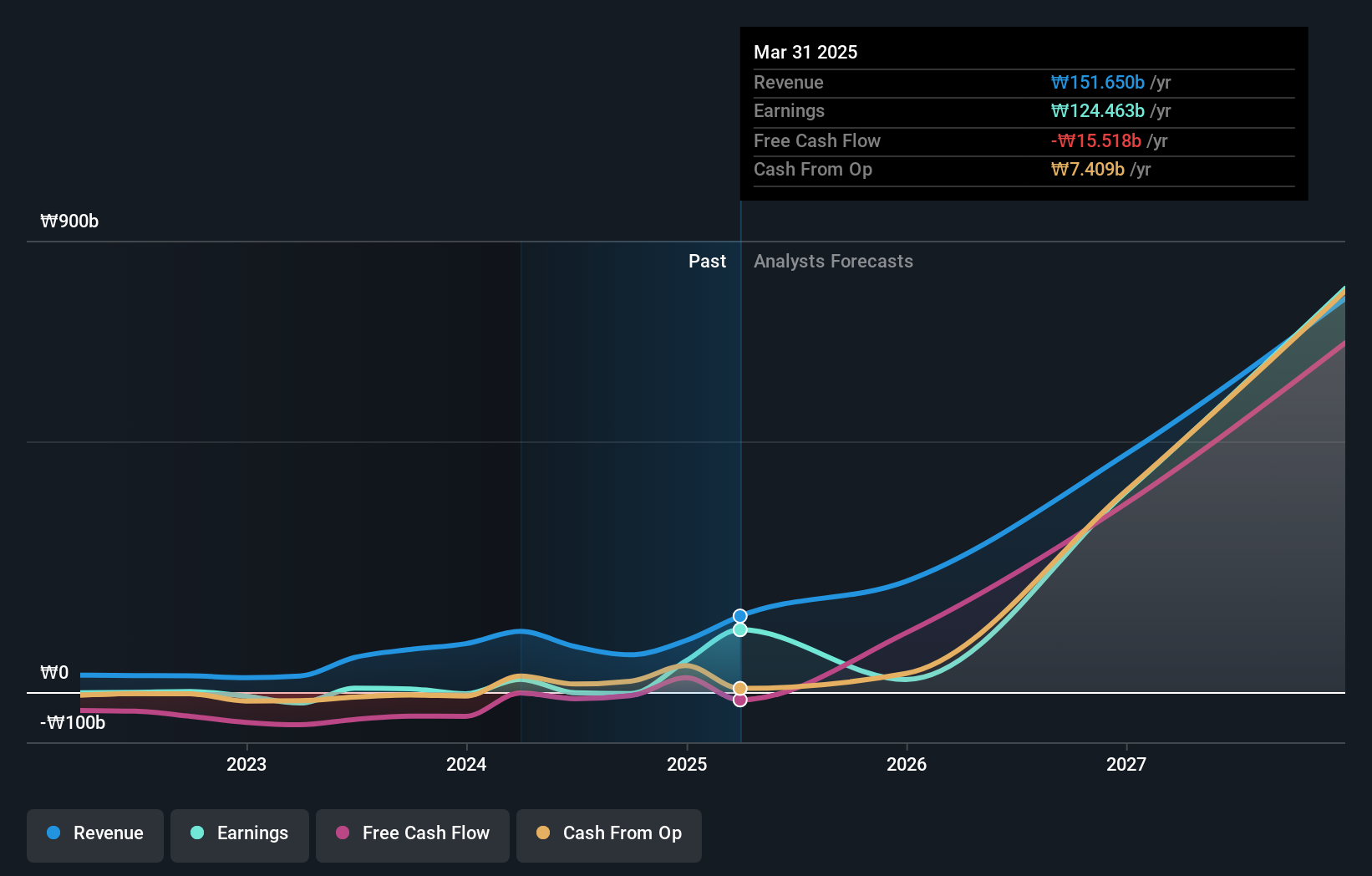

ALTEOGEN (KOSDAQ:A196170)

Simply Wall St Growth Rating: ★★★★★★

Overview: ALTEOGEN Inc. is a biotechnology company that specializes in the development of long-acting biobetters, proprietary antibody-drug conjugates, and antibody biosimilars, with a market cap of ₩20.11 trillion.

Operations: The company generates revenue primarily from its biotechnology segment, amounting to ₩90.79 million. It focuses on the development of innovative biopharmaceutical products.

ALTEOGEN is setting a brisk pace in South Korea's tech sector, with projections showing revenue growth at an impressive 64.2% annually, surpassing the broader market's 10.4%. This surge is backed by a significant commitment to R&D, crucial for maintaining technological edge and innovation; last year alone, R&D expenses were robustly maintained. Furthermore, earnings are expected to skyrocket by 99.5% per year, positioning ALTEOGEN well above its biotech peers who show more modest gains. Despite current unprofitability and shareholder dilution over the past year, the forecast for return on equity stands at a promising 66.3% in three years’ time, highlighting potential for substantial financial health improvements and market position strengthening within this high-stakes industry landscape.

- Unlock comprehensive insights into our analysis of ALTEOGEN stock in this health report.

Gain insights into ALTEOGEN's historical performance by reviewing our past performance report.

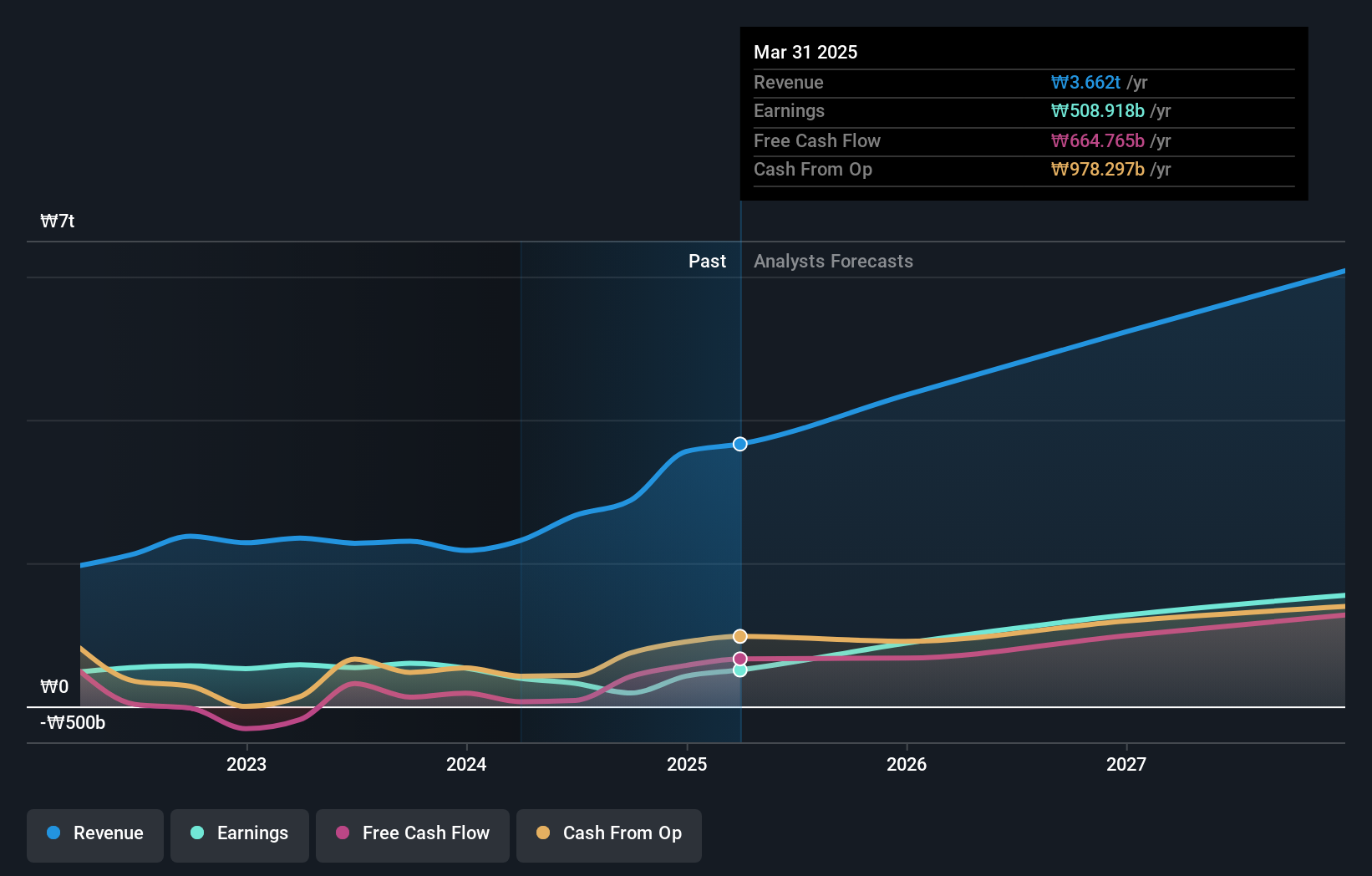

Celltrion (KOSE:A068270)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Celltrion, Inc., along with its subsidiaries, focuses on developing and producing protein-based drugs for oncology treatment in South Korea, with a market capitalization of ₩40.40 trillion.

Operations: The company generates revenue primarily from its Bio Medical Supply segment, contributing ₩3.54 trillion, and Chemical Drugs segment, adding ₩507 billion. The focus on protein-based oncology drugs underpins its business operations.

Celltrion's trajectory in South Korea's high-tech landscape is marked by a robust 25.6% annual revenue growth, outpacing the local market average of 10.4%. This growth is underpinned by a strategic focus on R&D, with expenses constituting a significant portion of revenue, reflecting its commitment to innovation particularly in biologics and biosimilars. Recent agreements with major U.S. health insurers for ZYMFENTRA® enhance its market penetration and are expected to bolster future revenues significantly. Additionally, the company's recent share repurchase program underscores confidence in its financial strategy and prospects, investing approximately KRW 75.89 billion back into the firm.

- Click to explore a detailed breakdown of our findings in Celltrion's health report.

Explore historical data to track Celltrion's performance over time in our Past section.

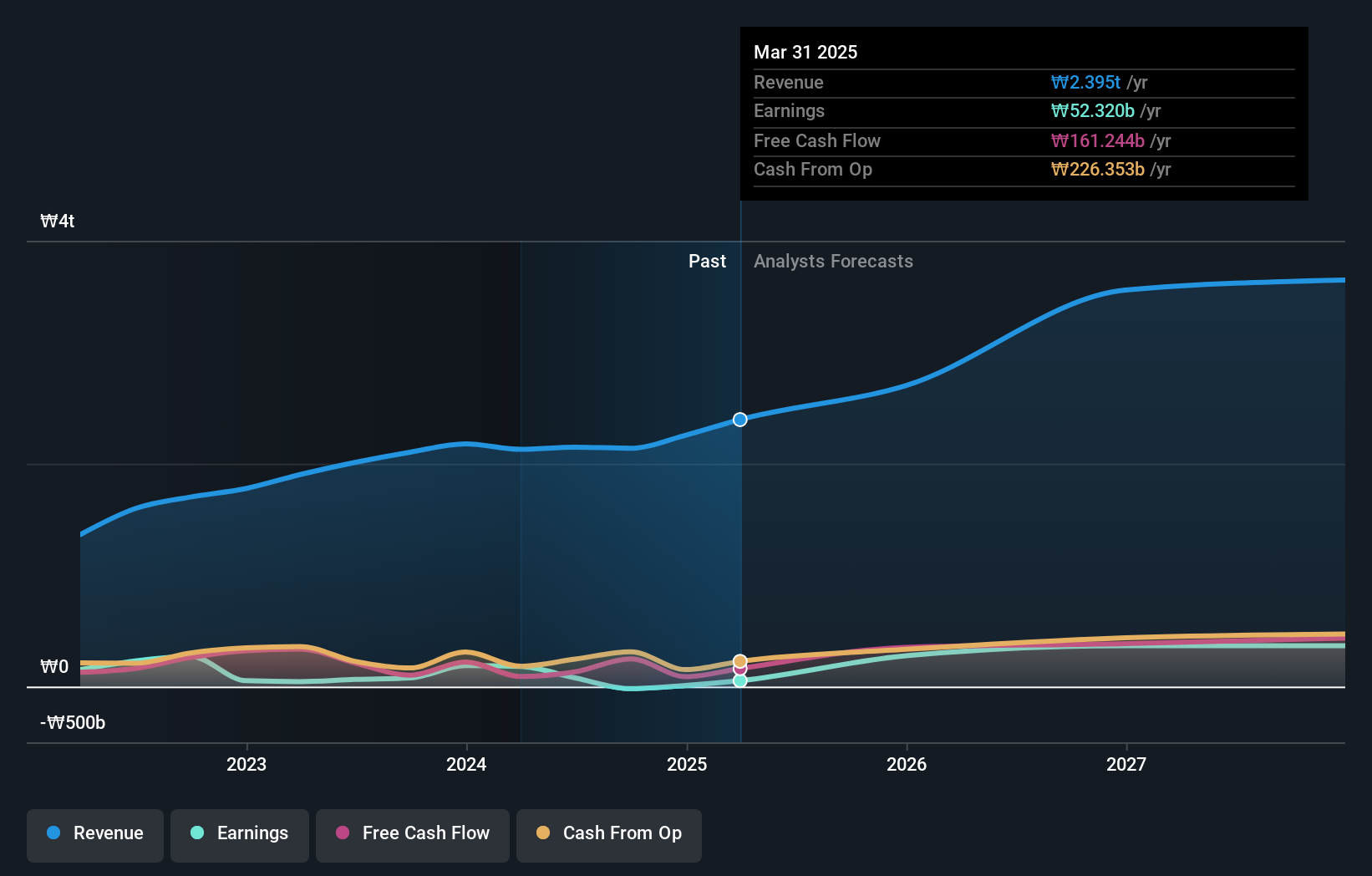

HYBE (KOSE:A352820)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: HYBE Co., Ltd. operates in music production, publishing, and artist development and management, with a market capitalization of ₩7.68 trillion.

Operations: HYBE Co., Ltd. generates revenue primarily from its Label and Solution segments, contributing ₩1.28 trillion and ₩1.24 trillion, respectively. The Platform segment adds ₩361 billion to its revenue streams.

HYBE's recent financial activities underscore its strategic maneuvers within South Korea's tech arena, marked by a 14% annual revenue growth and an aggressive R&D investment strategy. The company allocated a substantial 42.6% of its earnings to R&D, reflecting a deep commitment to innovation despite the broader industry's average growth. This focus on development is further highlighted by their recent share repurchase program where HYBE invested KRW 26.09 billion in buying back shares, signaling confidence in their ongoing projects and market position. These moves could be pivotal as HYBE continues to navigate the competitive entertainment technology landscape, aiming for sustained growth amidst fluctuating market conditions.

- Get an in-depth perspective on HYBE's performance by reading our health report here.

Understand HYBE's track record by examining our Past report.

Next Steps

- Gain an insight into the universe of 48 KRX High Growth Tech and AI Stocks by clicking here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com