Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalMarket Might Still Lack Some Conviction On Legimi S.A. (WSE:LEG) Even After 32% Share Price Boost

Despite an already strong run, Legimi S.A. (WSE:LEG) shares have been powering on, with a gain of 32% in the last thirty days. This latest share price bounce rounds out a remarkable 337% gain over the last twelve months.

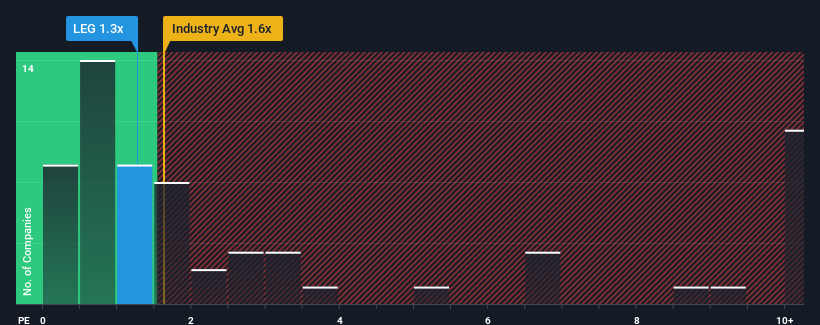

In spite of the firm bounce in price, you could still be forgiven for feeling indifferent about Legimi's P/S ratio of 1.3x, since the median price-to-sales (or "P/S") ratio for the Interactive Media and Services industry in Poland is also close to 1.6x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

See our latest analysis for Legimi

How Has Legimi Performed Recently?

Legimi certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. It might be that many expect the strong revenue performance to wane, which has kept the share price, and thus the P/S ratio, from rising. Those who are bullish on Legimi will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

Although there are no analyst estimates available for Legimi, take a look at this free data-rich visualisation to see how the company stacks up on earnings, revenue and cash flow.Is There Some Revenue Growth Forecasted For Legimi?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Legimi's to be considered reasonable.

If we review the last year of revenue growth, the company posted a terrific increase of 45%. The strong recent performance means it was also able to grow revenue by 155% in total over the last three years. So we can start by confirming that the company has done a great job of growing revenue over that time.

Comparing that to the industry, which is only predicted to deliver 11% growth in the next 12 months, the company's momentum is stronger based on recent medium-term annualised revenue results.

In light of this, it's curious that Legimi's P/S sits in line with the majority of other companies. Apparently some shareholders believe the recent performance is at its limits and have been accepting lower selling prices.

The Bottom Line On Legimi's P/S

Its shares have lifted substantially and now Legimi's P/S is back within range of the industry median. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

To our surprise, Legimi revealed its three-year revenue trends aren't contributing to its P/S as much as we would have predicted, given they look better than current industry expectations. There could be some unobserved threats to revenue preventing the P/S ratio from matching this positive performance. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to see the likelihood of revenue fluctuations in the future.

It is also worth noting that we have found 3 warning signs for Legimi that you need to take into consideration.

If these risks are making you reconsider your opinion on Legimi, explore our interactive list of high quality stocks to get an idea of what else is out there.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.