Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalWe Ran A Stock Scan For Earnings Growth And Giriraj Civil Developers (NSE:GIRIRAJ) Passed With Ease

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Giriraj Civil Developers (NSE:GIRIRAJ). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

View our latest analysis for Giriraj Civil Developers

How Fast Is Giriraj Civil Developers Growing?

If you believe that markets are even vaguely efficient, then over the long term you'd expect a company's share price to follow its earnings per share (EPS) outcomes. That makes EPS growth an attractive quality for any company. It certainly is nice to see that Giriraj Civil Developers has managed to grow EPS by 37% per year over three years. This has no doubt fuelled the optimism that sees the stock trading on a high multiple of earnings.

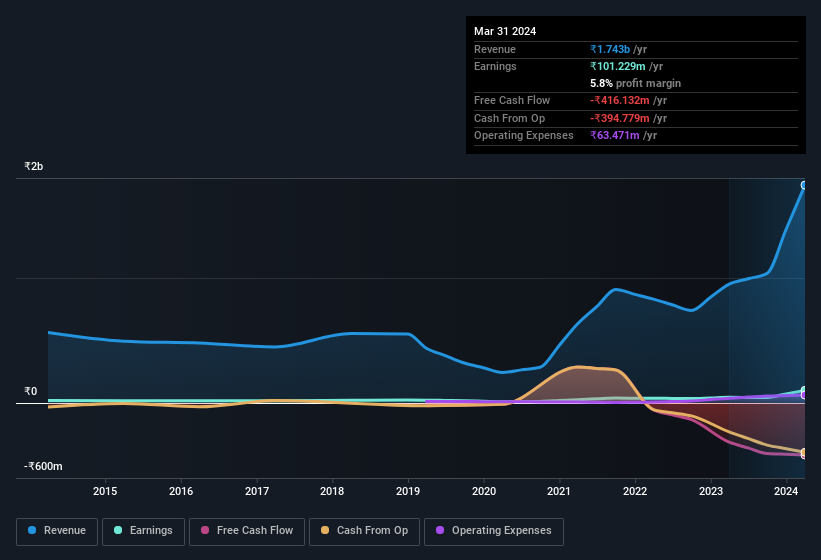

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. Giriraj Civil Developers maintained stable EBIT margins over the last year, all while growing revenue 83% to ₹1.7b. That's progress.

In the chart below, you can see how the company has grown earnings and revenue, over time. Click on the chart to see the exact numbers.

Giriraj Civil Developers isn't a huge company, given its market capitalisation of ₹9.8b. That makes it extra important to check on its balance sheet strength.

Are Giriraj Civil Developers Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

The good news is that Giriraj Civil Developers insiders spent a whopping ₹241m on stock in just one year, without so much as a single sale. The shareholders within the general public should find themselves expectant and certainly hopeful, that this large outlay signals prescient optimism for the business. We also note that it was the MD & Chairman, Krushang Shah, who made the biggest single acquisition, paying ₹116m for shares at about ₹116 each.

And the insider buying isn't the only sign of alignment between shareholders and the board, since Giriraj Civil Developers insiders own more than a third of the company. Indeed, with a collective holding of 68%, company insiders are in control and have plenty of capital behind the venture. This makes it apparent they will be incentivised to plan for the long term - a positive for shareholders with a sit and hold strategy. To give you an idea, the value of insiders' holdings in the business are valued at ₹6.7b at the current share price. So there's plenty there to keep them focused!

Does Giriraj Civil Developers Deserve A Spot On Your Watchlist?

For growth investors, Giriraj Civil Developers' raw rate of earnings growth is a beacon in the night. On top of that, insiders own a significant stake in the company and have been buying more shares. So it's fair to say that this stock may well deserve a spot on your watchlist. What about risks? Every company has them, and we've spotted 3 warning signs for Giriraj Civil Developers (of which 1 is a bit concerning!) you should know about.

The good news is that Giriraj Civil Developers is not the only stock with insider buying. Here's a list of small cap, undervalued companies in IN with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.