Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street Journal3 Chinese Stocks Estimated To Be Trading At Up To 49.3% Below Intrinsic Value

As Chinese equities have recently experienced a decline amid waning optimism about Beijing's stimulus measures, investors are increasingly focused on identifying undervalued opportunities within the market. In this context, a good stock is often characterized by strong fundamentals and potential for growth despite broader economic challenges, making it an appealing option for those seeking value in turbulent times.

Top 10 Undervalued Stocks Based On Cash Flows In China

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| HangzhouS MedTech (SHSE:688581) | CN¥57.63 | CN¥109.10 | 47.2% |

| Zhejiang Huahai Pharmaceutical (SHSE:600521) | CN¥18.80 | CN¥37.02 | 49.2% |

| Wuhan Keqian BiologyLtd (SHSE:688526) | CN¥13.38 | CN¥25.45 | 47.4% |

| Range Intelligent Computing Technology Group (SZSE:300442) | CN¥30.79 | CN¥58.56 | 47.4% |

| Beijing Konruns PharmaceuticalLtd (SHSE:603590) | CN¥23.52 | CN¥46.03 | 48.9% |

| Neusoft (SHSE:600718) | CN¥10.04 | CN¥19.29 | 47.9% |

| Crystal Growth & Energy EquipmentLtd (SHSE:688478) | CN¥29.09 | CN¥56.10 | 48.1% |

| GemPharmatech (SHSE:688046) | CN¥12.95 | CN¥25.26 | 48.7% |

| Brilliance Technology (SZSE:300542) | CN¥20.61 | CN¥40.65 | 49.3% |

| Ningbo Jifeng Auto Parts (SHSE:603997) | CN¥13.45 | CN¥26.09 | 48.4% |

Here's a peek at a few of the choices from the screener.

Shenzhen Megmeet Electrical (SZSE:002851)

Overview: Shenzhen Megmeet Electrical Co., LTD focuses on the R&D, production, sales, and services of hardware, software, and system solutions for electrical automation in China with a market cap of CN¥14.37 billion.

Operations: The company's revenue segments include Smart Equipment (CN¥390.08 million), Precision Connection (CN¥357.48 million), Industrial Automation (CN¥605.29 million), Industrial Power Products (CN¥2.25 billion), New Energy and Rail Transit (CN¥597.02 million), and Smart Home Appliances Electronic Control Products (CN¥3.23 billion).

Estimated Discount To Fair Value: 31.5%

Shenzhen Megmeet Electrical is trading at CN¥28.7, significantly below its estimated fair value of CN¥41.92, indicating potential undervaluation based on cash flows. The company's earnings and revenue are forecast to grow faster than the Chinese market, at 26.9% and 21.7% per year respectively. However, its dividend yield of 0.76% is not well covered by free cash flows, and return on equity is projected to remain low at 16.4%. Recent share buybacks totaling CNY 20 million suggest confidence in future prospects despite current challenges with one-off items impacting results.

- The analysis detailed in our Shenzhen Megmeet Electrical growth report hints at robust future financial performance.

- Take a closer look at Shenzhen Megmeet Electrical's balance sheet health here in our report.

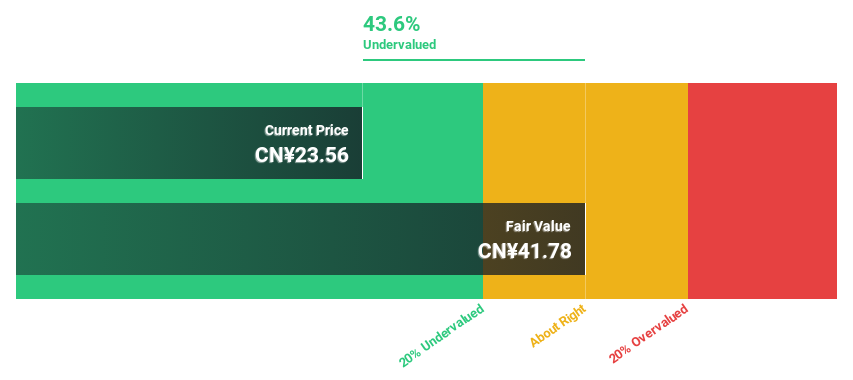

Brilliance Technology (SZSE:300542)

Overview: Brilliance Technology Co., Ltd., along with its subsidiaries, offers information solutions and services in China and has a market capitalization of CN¥6.15 billion.

Operations: Brilliance Technology Co., Ltd. generates revenue by providing information solutions and services in China.

Estimated Discount To Fair Value: 49.3%

Brilliance Technology is trading at CN¥20.61, well below its estimated fair value of CN¥40.65, highlighting potential undervaluation based on cash flows. Despite a recent net loss and declining revenue, the company's earnings are projected to grow significantly at 73.4% annually, outpacing the Chinese market's growth rate of 23.3%. However, profit margins have decreased from last year, and share price volatility remains high over the past three months.

- Upon reviewing our latest growth report, Brilliance Technology's projected financial performance appears quite optimistic.

- Click here to discover the nuances of Brilliance Technology with our detailed financial health report.

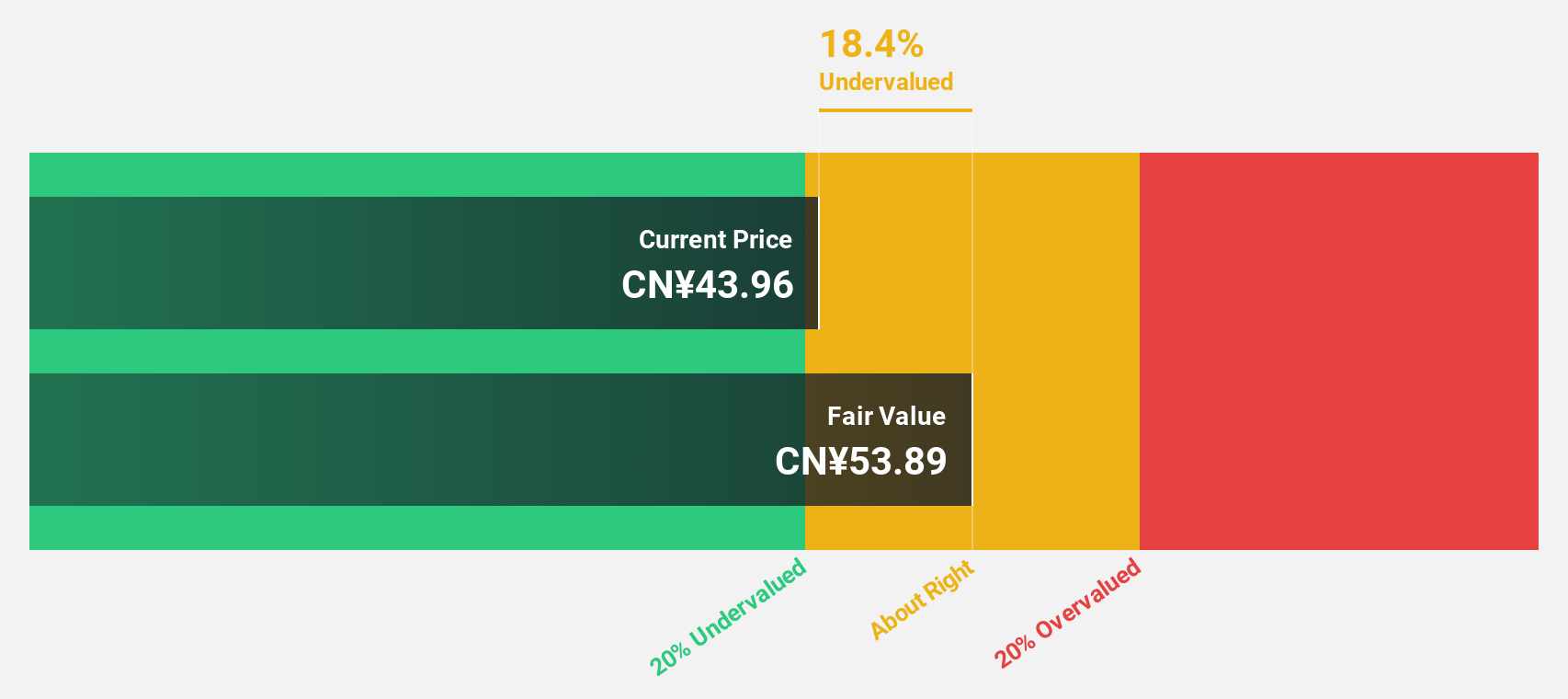

Electric Connector Technology (SZSE:300679)

Overview: Electric Connector Technology Co., Ltd. specializes in the research, design, development, manufacture, sale, and marketing of electronic connectors and interconnection systems globally with a market cap of CN¥19.11 billion.

Operations: The company's revenue from the connector industry segment is CN¥3.55 billion.

Estimated Discount To Fair Value: 15.9%

Electric Connector Technology, trading at CN¥45.48, is undervalued relative to its estimated fair value of CN¥54.07 and offers good relative value compared to peers. Despite a low forecasted return on equity (16.5%), the company expects significant earnings growth of 28.4% annually, surpassing market averages. Recent buybacks totaling CN¥100.28 million underscore management's confidence in its valuation, while robust revenue growth of 26.4% suggests strong future cash flows despite a modest dividend yield of 0.79%.

- Insights from our recent growth report point to a promising forecast for Electric Connector Technology's business outlook.

- Dive into the specifics of Electric Connector Technology here with our thorough financial health report.

Summing It All Up

- Gain an insight into the universe of 108 Undervalued Chinese Stocks Based On Cash Flows by clicking here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com