Index Options

Index Options CME Group

CME Group Nasdaq

Nasdaq Cboe

Cboe TradingView

TradingView Wall Street Journal

Wall Street JournalThree Undiscovered Gems To Enhance Your Portfolio

As global markets experience fluctuations, with U.S. stocks reaching new highs amid a mix of economic signals, investors are increasingly looking toward small-cap stocks for potential growth opportunities. In this dynamic environment, identifying undiscovered gems—stocks that may not yet have captured widespread attention but exhibit strong fundamentals and potential for growth—can be a strategic way to enhance your portfolio.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Kanda HoldingsLtd | 30.47% | 4.35% | 18.02% | ★★★★★★ |

| Impellam Group | 31.12% | -5.43% | -6.86% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Standard Bank | 0.13% | 27.78% | 30.36% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| iMarketKorea | 28.53% | 5.35% | 1.30% | ★★★★★☆ |

| National Petroleum | 0.09% | 3.54% | 0.72% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Wilson | 64.79% | 30.09% | 68.29% | ★★★★☆☆ |

| Bhakti Multi Artha | 45.07% | 32.89% | -17.68% | ★★★★☆☆ |

We'll examine a selection from our screener results.

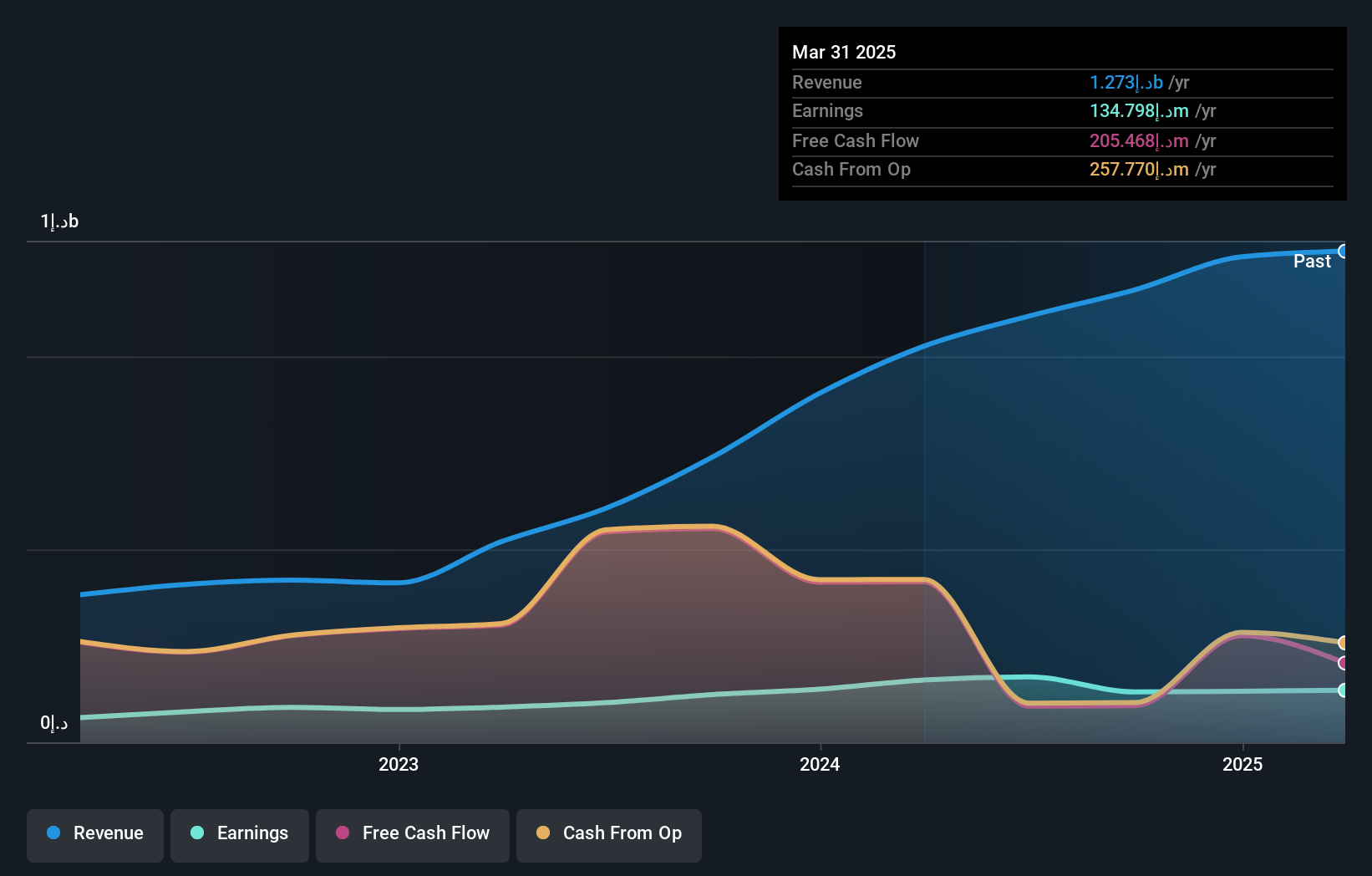

Dubai Insurance Company (P.S.C.) (DFM:DIN)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Dubai Insurance Company (P.S.C.), along with its subsidiaries, offers a range of insurance products for individuals and businesses in the United Arab Emirates, with a market capitalization of AED 1.27 billion.

Operations: Dubai Insurance generates revenue primarily from its Life and Medical segment, contributing AED 505.39 million, and its Motor and General segment, contributing AED 596.31 million.

Dubai Insurance Company, a nimble player in the insurance sector, reported impressive earnings growth of 65.1% over the past year, outpacing the industry average of 12.9%. The company posted a net income of AED 50.73 million for Q2 2024, up from AED 42.83 million in the previous year. With a price-to-earnings ratio of 7.5x below the AE market's average and high-quality earnings, it seems well-positioned despite its illiquid shares and increased debt-to-equity ratio from 1.2% to 6.4%.

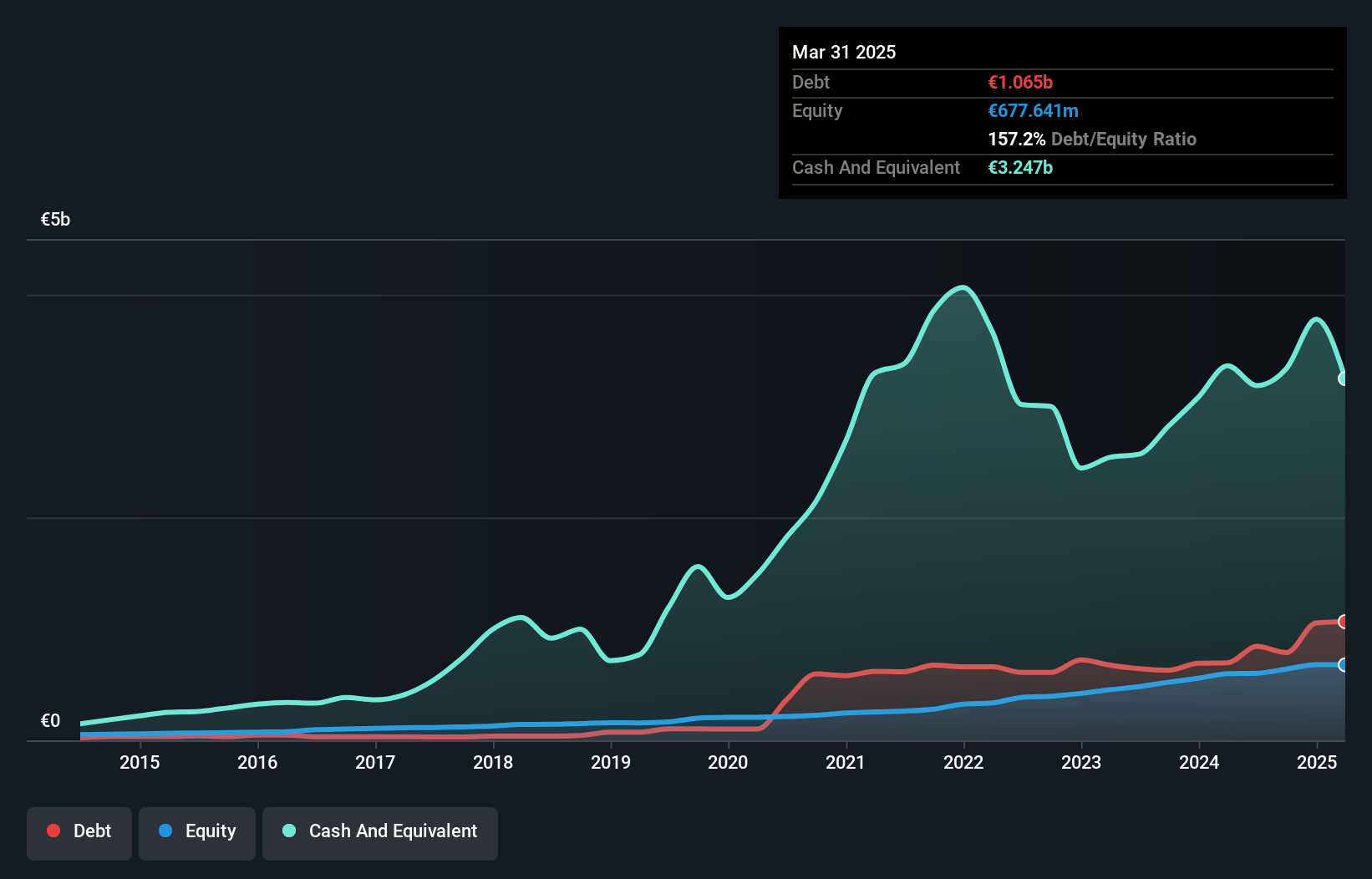

AS LHV Group (TLSE:LHV1T)

Simply Wall St Value Rating: ★★★★★★

Overview: AS LHV Group operates through its subsidiaries to offer a range of banking products and services to private and business customers in Estonia and the United Kingdom, with a market capitalization of approximately €1.13 billion.

Operations: LHV Group's primary revenue streams include Retail Banking, generating €137.37 million, and Corporate Banking, contributing €84.17 million. The company also earns from its LHV Bank LTD segment with €46.88 million in revenue and Asset Management at €9.44 million. Notably, the net profit margin is a key metric to consider when evaluating financial performance trends over time.

LHV Group, with assets of €7.3B and equity of €602.3M, seems to be a solid player in the banking sector. It boasts a net interest margin of 3.9% and has total deposits at €5.8B against loans of €3.9B, highlighting its robust financial position. The bank's allowance for bad loans is sufficient at 113%, while non-performing loans are just 0.8%. Recent guidance revisions show an upbeat outlook with expected net profit growth driven by an expanding loan portfolio and higher interest rates.

- Click here to discover the nuances of AS LHV Group with our detailed analytical health report.

Assess AS LHV Group's past performance with our detailed historical performance reports.

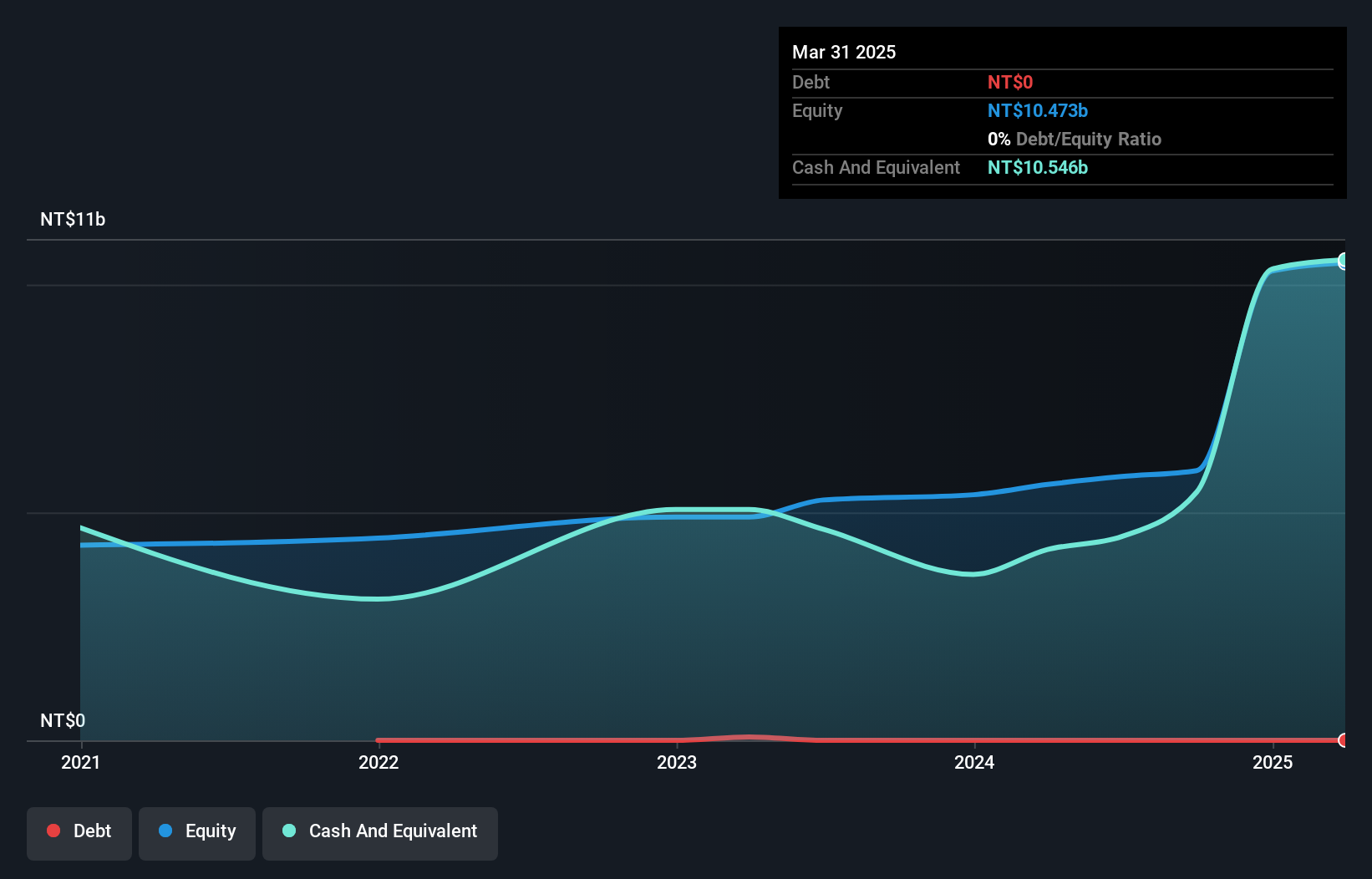

LINE Pay Taiwan (TPEX:7722)

Simply Wall St Value Rating: ★★★★★★

Overview: LINE Pay Taiwan Limited operates in the third-party payment sector within Taiwan, with a market capitalization of NT$35.52 billion.

Operations: The primary revenue stream for LINE Pay Taiwan Limited is from data processing, amounting to NT$5.52 billion.

LINE Pay Taiwan, a nimble player in the financial sector, has recently been added to the S&P Global BMI Index. The company reported impressive earnings growth of 39.5% over the past year, outpacing its industry peers. With sales reaching TWD 1.48 billion in Q2 2024 and net income climbing to TWD 159 million from TWD 105 million a year ago, it showcases strong performance metrics. Notably debt-free for five years, LINE Pay Taiwan boasts high-quality non-cash earnings and remains profitable despite negative free cash flow figures like -TWD 106 million as of October 2024.

- Click to explore a detailed breakdown of our findings in LINE Pay Taiwan's health report.

Gain insights into LINE Pay Taiwan's past trends and performance with our Past report.

Key Takeaways

- Click here to access our complete index of 4786 Undiscovered Gems With Strong Fundamentals.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com